This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many small businesses choose ACHoperators because they are more convenient than most direct deposits. ACH transfers don’t come with high fees and transactions and they’re easily edited if an employer wants to adjust payroll, extend bonuses, or reimburse an employee.

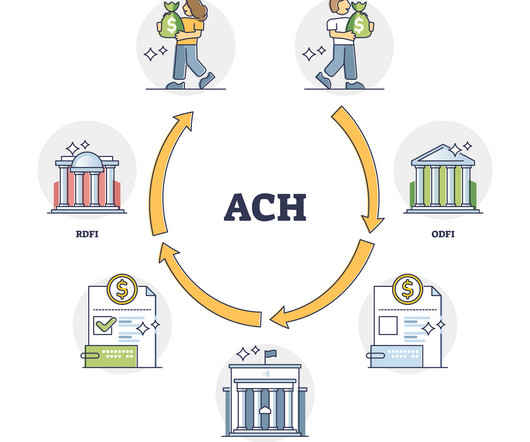

They give their bank a request to send funds through the ACH network. The bank then packages this request into a digital file, which gets sent to an ACHoperator. This operator acts like a middleman, making sure everything is in order and routing the payment to the right place. ACH Deposit Timing: How Long Does It Take?

The payment process using ACH transfers involves the payee creating a payment order which is received by the originator bank. The originator bank compiles all the POs and sends them to an ACH for processing. The ACHoperator then approves and releases the PO amount to the recipient bank.

Last week, NACHA issued an ACHoperations bulletin announcing the delay of the rollout of a third Same Day ACH (SDA) processing window by six months, to March 19, 2021. The regulator notified NACHA that they need more time to evaluate required changes to their system before giving it the green light.

ACH vs EFT ACH is a form of EFT, but EFT is a broad category encompassing different electronic payment types, including ACH. All ACH transactions are forms of EFTs, but not all EFTs are ACH transactions. Update protocols and systems as needed to accommodate changes in business or regulations.

The ACH network (Automated Clearing House network) allows banks to work with each other without the need to have their own network. Instead, they are under the jurisdiction of NACHA (The National Automated Clearing House Association), which establishes the rules and regulations that all the institutions that are part of the network follow.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content