This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Entities and Types of Scams Covered Under the Shared Responsibility Framework The SRF applies to all full banks, major payment service providers (PSPs), and telcos with major roles in safeguarding consumers’ financial and communication activities. Telcos’ Duties Telcos play a key role in securing SMS channels used in digital banking.

An independent review of the policy’s effectiveness is scheduled for October 2025, which will critically assess its impact, including the liability cap, success in reducing fraud, impact on competition, and operational shortcomings. This disparity created a postcode lottery for victims, depending largely on where they banked.

The horse in front Just like the vast natural grassland of the Kazakh Steppe, which lies in contrast to the modern cities of Astana and Almaty, so is the traditional banking landscape (dominated by three large banking groups) contrasted by a fast-moving digital leader – Kaspi.kz (Kaspi). However, this was not the case for Kaspi.

The Reserve Bank of India (RBI) has released the Draft Directi ves 2025 on Lending Against Gold Collateral, bringing a much-needed regulatory reset to a sector thats long operated in silos. Additionally, the enforcement of the 75% Loan-to-Value (LTV) cap was uneven, and risk weights were incorrectly applied.

and can cover the costs associated with transferring funds between banks, fraud prevention, and compensating card networks, payment processors, and issuing banks. Heres how each pricing structure works: Tiered pricing classifies transactions into predefined categories (qualified, mid-qualified, and non-qualified) with varying rates.

A Bank of England experiment proving that offline payments with a digital pound are technically feasible, but complex. The Bank of England (BoE) has demonstrated that it is technically feasible to carry out offline payments with a digital pound. Why is it important? Kristaps Zips UK CEO, payabl.

Company Background and Evolution Shift4’s journey began in 1999, when 16-year-old Jared Isaacman started a tiny payment processing business (then called United Bank Card ) out of his parents’ basement. Shift4 also set its sights on new industry verticals – notably non-profits, gaming, and even space technology.

These aren’t just suggestions, they’re critical guardrails that protect your business from non-compliance and ensure transparency with your customers. Notify Networks and Understand Their Requirements Your next move is notifying the card brands and your acquiring bank. Here are three important rules to be aware of: 1.

Roles of survey respondents Survey respondent company area Non-bank financial institutions dominated the survey respondents, accounting for nearly one in five participants (20%). Notably, emerging sectors such as digital assets and crypto, open banking, and cross-border payments each captured 2.5%

The regulations surrounding surcharging can be a bit confusing, and non-compliance has consequences. Usually, there’s a cap: you can’t charge more than 4% of the transaction amount. It limits how much banks can charge businesses to process debit card transactions, especially when the bank has more than $10 billion in assets.

Credit card networks and issuing banks don’t waive their cut; instead, these costs are shifted from the merchant to the customer. It’s important to distinguish this from deceptive offers that promise free processing but hide costs in monthly fees, equipment leases, or inflated rates on non-credit card transactions.

Authorization An authorization is a request to the cardholders bank to approve a charge. Acquirer (Acquiring Bank) The bank or processor that works with the merchant. Issuer (Issuing Bank) The issuing bank is the bank that gave the customer their credit or debit card.

Geale is responsible for helping to deliver the National Payments Vision and driving the FCAs work on open banking and digital finance. Fintilect, the AI-powered hyper-personalised digital banking provider for financial providers across the globe, has appointed Lindsay Soergel as CEO.

Globally, preparations for central bank digital currencies and evolving open finance frameworks signal longer-term structural change. Some of this activity creates new opportunities for firms, such as the Data (Use and Access) Act 2025 for open banking and open finance. Jaspreet Kaur Senior consultant. to 1.15% (debit) and 0.3%

Most providers require that you set up a merchant account, which acts as a secure intermediary to transfer funds from customer payments to your business bank account. Is there a cap on how many transactions can be processed through your Salesforce gateway?

Credit card processing fees are comprised of several fees, such as: Interchange fees: Interchange fees are paid to the card-issuing bank and typically consist of a percentage of the total transaction amount plus a small, fixed charge. Non-compliance can result in legal implications fines, and damage reputation. Request a demo or trial.

This constantly updated article tracks the biggest and most important new products released worldwide by financial technology companies, along with banks, credit unions, investment advisors, insurance companies, credit card issuers and payment providers. Weve been obsessed with new fintech products since before the term was invented.

The bank, listed in Ho Chi Minh City, intends to offer the shares at 34,500-36,000 dong (US$1.36-US$1.40) This move values the bank at approximately 53.5 The sale faces significant hurdles due to regulatory limits on foreign ownership in Vietnamese banks, capped at 30%. trillion dong (US$2.1

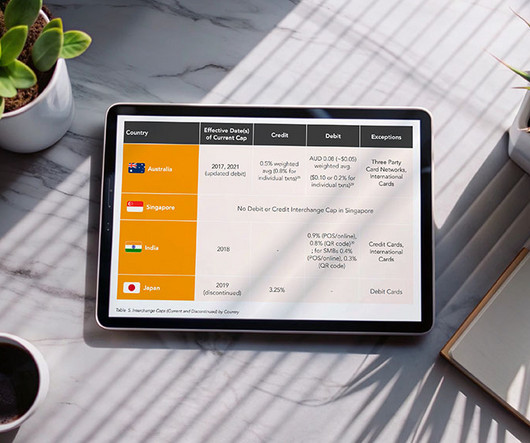

The report highlights the role of regulatory , such as interchange fee caps and the promotion of pay-by-bank alternatives, in reducing merchant costs and interventions enhancing competition within the payment market. Australia, for example, introduced caps on interchange fees in 2003 for both credit and debit transactions.

5) hearing before the House Financial Services Committee , representatives from several consumer groups said “rent-a-bank” schemes harm consumers through predatory lending. The hearing was titled “Rent-a-Bank Schemes and New Debt Traps: Assessing Efforts to Evade State Consumer Protections and Interest Rate Caps.”.

The central bank of Russia is seeking to place a yearly cap on the amount of cryptocurrency that retail investors can purchase, CoinDesk reported. Non-qualified investors wouldn’t be able to purchase over 600,000 rubles (approximately $7,740) per a proposal that the Bank of Russia released.

A mix of Thai and regional business groups, including SeaMoney Thailand, SCB X, CP Group, Gulf Energy, and VGI, are preparing to apply for virtual bank licences from the Bank of Thailand, according to the Bangkok Post. Speculation points to Bangkok Bank (BBL), the country’s largest lender, and Jaymart as potential collaborators.

Set rate processing Subscription rate processing TL;DR Interchange fees are not collected by your payment processor or bank; they go directly to the card-issuing banks. Interchange fees vary significantly depending on the card issuer, the issuing bank, type of transaction and/or merchant type.

In Malaysia, Bank Negara Malaysia has spearheaded efforts to introduce the Consumer Credit Act (CCA), which aims to increase consumer protection by regulating non-bank credit providers like BNPL companies.

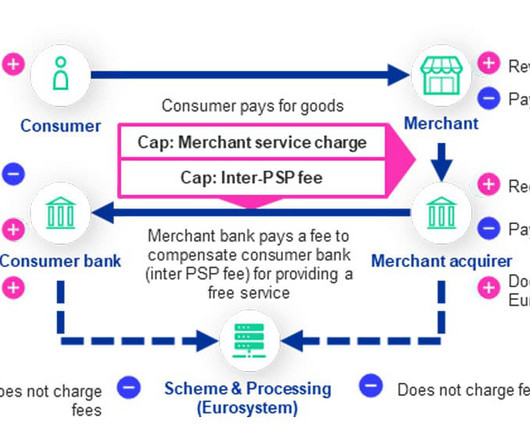

TRANSACTION FEE: A step-by-step overview of the digital euro compensation model Payment service providers will be able to charge merchants a fee for enabling them to accept digital euro transactions, the European Central Bank (ECB) has revealed, but a cap will be placed on the amount that it will be possible for them to charge.

Wells Fargo To Cap SMB Bailout Loans at $10 Billion. The country’s fourth-largest bank said it anticipates that its loan capacity will be maxed out under the program since it is operating with the current asset cap limitations. Plus, the European Union began investigating Facebook’s marketplace as part of its antitrust probe.

Banks need the technology of FinTech companies, and tech upstarts need the conduit to customers and installed trust that comes with decades of relationships that span generations. As Bloomberg reported, national banks are exempt from state-level dictates on usury limits. However, looking elsewhere beyond U.S.

For example, the now shuttered ABLV bank in Latvia, along with the Estonian branches of Danske Bank and Swedbank, have all been implicated with Russian money that could have dubious origins. The lessening of deposits came around the same time that prosecutors started an investigation in July in the Danske Bank Estonia branch.

According to the report, the European Commission said that Mastercard has long stopped retailers from looking for lower bank fees that are available outside of their country. percent fee on non-EU debit card payments done in shops, and a 0.3 credit card companies charge. The two payment companies have proposed a 0.2

It requires stringent adherence to regulatory guidelines and card network rules, from surcharge caps to disclosure requirements. Some states cap the surcharge rate to a set rate or dollar amount. Merchants pay interchange fees to compensate the cardholder’s bank (issuer) for the risk of managing credit card accounts.

14), Wells Fargo called out strong mortgage banking fees, higher equity markets and declining sequential charge-offs as positives for the period. “As The bank said that was predominantly due to increased consumer spending. The bank reported almost $1 billion of expenses linked to customers refunds tied to previous scandals.

Interestingly, even at that top of the new range, should pricing remain there, at the close of the day, the market cap of $1.8 Blue Apron is another firm that is likely to come public, as the on-demand delivery meal kit firm is rumored to be in talks with banks to lead an IPO. billion since its founding in 2010.

The company was accused of setting rules that blocked banks in one EU country from offering lower interchange fees to a retailer in another EU country. Mastercard actually stopped the practice in December of 2015 after the European Commission (EC) adopted charge-capping rules. The EC has long fought with the companies over fees.

After the financial crash in 2008, banks saved up billions in reserves to make sure that they would be able to handle times of market stress and be able to keep lending. The Fed is basically telling banks to dip into those reserves if they have to. Comcast said it would raise speeds, and AT&T said it would waive data caps.

India’s alternative finance community is calling on the Reserve Bank of India (RBI) to relax regulations on the market, particularly as they pertain to lending caps. “SME lending is an area which we are looking to grow,” said alternative lender RupeeCircle Co-Founder Abhishek Gandhi.

Digital lending marketplace BitX Funding , which matches business owners and non-bank lenders, is aiming to help Amazon third-party (3P) sellers grow. ” Rowe continued, “ Amazon sellers start off with an Amazon Working Capital Loan, but over time they hit a wall as their growth is capped at $1 million in financing.

For banks interested in transforming their brick-and-mortar branches, maybe, according to Diebold Nixdorf Senior Director of Advisory Services Chris Gill. One of the all too common mistakes banks make is letting the technology take the lead.”. Is there a right way and wrong way to innovate? It’s easy to let that happen, he said.

Wells Fargo To Cap SMB Bailout Loans at $10 Billion. Banks were supposed to start taking in PPP applications on April 3, but only JPMorgan Chase and Bank of America (BoA) had the ability to roll out per a report on April 5. COVID-19 Stimulus Money Could Show Up In Consumer Bank Accounts Today.

It makes it easier for merchants to make the switch to accepting non-cash payment methods like credit cards or contactless payments, which are often seen as more convenient for customers, but can come at a steep price. However, debit card processing fees are capped, and the interchange rates are less than credit card processing rates.

Traditionally, consumers stuck with familiar banks, but there’s now a growing trend of current account switching. The service was introduced as part of a government initiative to increase competition in the banking sector, aiming to reduce the inertia that had kept 75% of account holders with the same bank for years.

25) that China’s largest insurer (as measured by market cap) aims to take its OneConnect financial management unit public. OneConnect offers services to small to mid-sized financial firms, having partnered with hundreds of banks and more than 1,800 non-bank financial companies. 24) and Monday (Feb.

The American Fintech Council (AFC), the industry association representing responsible fintech companies and innovative banks, offered testimony before the Washington State House Committee on Consumer Protection and Business recommending key amendments to legislation recently introduced.

Small businesses (SMBs) in China are struggling to access bank loans with large, state-owned corporations, according to recent analysis from French trade credit insurer Coface , reported CNBC. That, combined with ballooning debt and ongoing trade disputes with the U.S.,

.” The Fed is said to be charging higher interest than the PPP initiative, and the debts are non-forgivable. Companies also have four years to pay the debts, but Bank of Southern California CEO Nathan Rogge said, per the report, that the window doesn’t provide sufficient time for a number of his customers.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content