This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The cardissuers often side with the customer without consulting us, which is unfair and costly. Cardissuers often make judgment calls onservice disputes without consulting merchantsor understanding the nature of our transit business,leaving us to bear the financial and operational burden, he explained.

Interoperability across multiple domestic and international card schemes without cobadging constraints. Significant simplification of the technical architecture for merchants. no mandatory cobadging). It expresses the views and opinions of the author. 13 February nexo standards: simplifying payments one transaction at a time.

EMI Is Not a Monolith The EMI sector spans everything from simple gift cardissuers to sophisticated platforms delivering government disbursements. However, critics note that few of these inputs are publicly disclosed or provide quantitative justification for the rating shift.

The cardissuers often side with the customer without consulting us, which is unfair and costly. Katherine Bailey (Valor Hospitality Europe Limited) explained how customers manipulate chargeback systems to claim refunds for services theyve already consumed: The guests enjoy a stay or experience and then dispute the charges.

and $0.50), plus a percentage of each purchase (between 1% and 3%) on top of the interchange fees charged by the cardissuers. Tiered Pricing A tiered model puts credit card transactions into several categories—qualified, mid-qualified, and non-qualified. We offer you subscription-based credit card processing at a direct cost.

Prior to joining CA Technologies, James led the EMEA Security consulting practice at IBM Global Technology Services and the e-Crime Prevention consulting practice at Deloitte. James is a recognized security and fraud expert covering topics such as mobility, cryptography, e-commerce, and network and infrastructure security.

Guest post by Emily Rueth , Managing Director & Founder of Vicuse Payments Advisors For cardissuers, embracing and implementing even the most basic use cases for artificial intelligence (AI) can revolutionize your operations and enhance customer experiences.

SRM (Strategic Resource Management, Inc.) , an independent advisory firm serving financial institutions across North America and Europe, has announced that, through its subsidiary SRM Europe, it has acquired Accourt Payments Specialists , a provider of payments consulting and other strategic services based in the United Kingdom.

said PSCU had already worked on many things Primax clients could utilize, including “digital and mobile banking, security and fraud mitigation solutions, business intelligence and data analytics, and expert consulting services to help optimize operations and portfolios,” the release states. Primax president and CEO Ted Keith Jr.

AI is not a barrier for cross-border payments Serena Smith, chief client officer, at i2c Inc Serena Smith , chief client officer, at i2c Inc , the cardissuer and payment processor, explains that AI will not be the main hindrance for cross-border payments growth in 2024.

Transactions are also more secure, with Mastercard data revealing that the risk of fraud is 30 times lower when using virtual cards compared to traditional payment cards. A 2023 infographic produced by Up in the Air, a travel payment consultancy from the Netherlands, depicts a dynamic and diversified B2B travel payment landscape.

A new study has found that the number of payment cards issued globally reached 14 billion last year and is predicted to rise to 17 billion by 2022, boosted by an increase in overall debit card issuance. RBR , a strategic research and consulting firm, recently published its “Global Payment Cards Data and Forecasts to 2022” report.

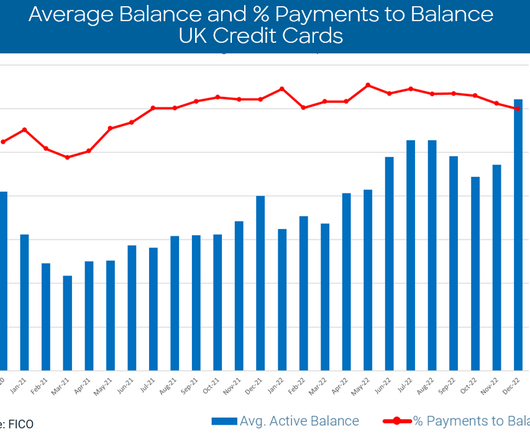

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service produced by FICO® Advisors , the business consulting arm of FICO®. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK cardissuers.

This week, Mastercard announced a partnership with Danish FinTech Cardlay in an initiative to expand Mastercard’s commercial card presence throughout Europe by connecting cardissuers with technology that augments their own corporate card offerings. Cards Tackle Event Planning Expenses.

The payment card business is among the most competitive areas of financial services. A growing number of fintechs have developed strategies and technologies to help cardissuers and acquirers access millions of dollars in cost savings and missed revenue by better controlling card network fees and enhancing transactional profitability.

Cardlay Payment Solutions Cardlay Payment Solutio ns’ white-label card and expense management product, Cardlay Expense, delivers an exceptional, real-time experience for card users. Features A fully bank-integrated, real-time product that helps banks provide corporate card clients a highly competitive user experience.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service produced by FICO® Advisors, the business consulting arm of FICO®. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK cardissuers.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service produced by FICO® Advisors, the business consulting arm of FICO. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK cardissuers.

Average card spending has increased month-on-month and year-on-year. These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK cardissuers.

“Never buy a couch without consulting your spouse.” But if the man called his cardissuer and pretended the order was never his and that his card had been misused fraudulently, he wouldn’t owe the fee. Gluck said that presented his friend with an interesting moral dilemma.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service produced by FICO® Advisors, the business consulting arm of FICO. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK cardissuers.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service produced by FICO® Advisors, the business consulting arm of FICO. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80%of UK cardissuers. .

TL;DR Surcharges are additional fees that a business adds to a customer’s bill when they choose to pay with a credit card. These fees help the business offset the cost of credit card processing fees, which the merchant typically has to pay to the cardissuer and payment processor.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service produced by FICO® Advisors, the business consulting arm of FICO®. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK cardissuers.

If the new FCA persistent debt rules come into effect, the way issuers communicate with customers will determine how successful they are and could affect customer risk and retention. Here are some options for issuers, based on our experience helping banks contact customers using FICO Customer Communication Services : 1.

Prior to joining Discover, Hochschild worked for consulting firm Booz Allen, and had also served in various leadership roles at MBNA America. The card company was originally launched in 1986 by Sears to compete against Visa, Mastercard and American Express.

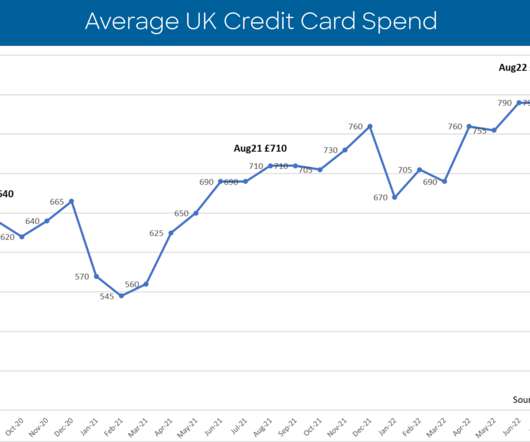

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK cardissuers.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client finance reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK cardissuers.

FICO’s latest market report of UK card trends suggests that consumers managed their credit card debt to keep lines of credit open for the festive season as spend increased month on month. These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service.

Despite the many benefits offered by virtual cards, AP professionals and vendors still have reservations about adopting them. Cardissuer U.S. Bank believes it has the perfect weapon to counter such reluctance: strong client and vendor input. In this month’s feature story, U.S.

The United Kingdom and the Nordic region continue to lead Europe in terms of digital transformation and fraud loss reduction - but non-card scams are rising fast. Senior Consultant, Fraud and Financial Crime. As such, the UK’s challenges and successes can be instructive for cardissuers in other countries across Europe.

However, rolling out virtual cards in AP departments does have some challenges. Bank — Jennifer Swenson, vice president of corporate payment systems, and Adam Kruis, senior vice president and manager of working capital consulting — addressed some of these concerns in a recent interview with PYMNTS. Two officials from U.S.

To combat that, our mission is to provide end-to-end solutions that address the entire payments ecosystem — from payment automation in accounts payable to an intuitive supplier portal for both AP and AR, to payment processing and credit card tokenization for merchants, to virtual cardissuer processing for financial institutions and so much more.

According to Grant Halverson, CEO of McLean Roche Consulting, interchange fees from commercial card payments account for more than $46 billion in revenue for cardissuers. It is unclear how much of that spend is made online, however.

Furthermore, Visa and Mastercard engage with regulatory authorities through advocacy efforts and industry consultations to influence regulatory policies and advocate for industry-friendly regulations conducive to innovation and competition. Regulatory changes necessitate adjustments to their compliance frameworks and operational practices.

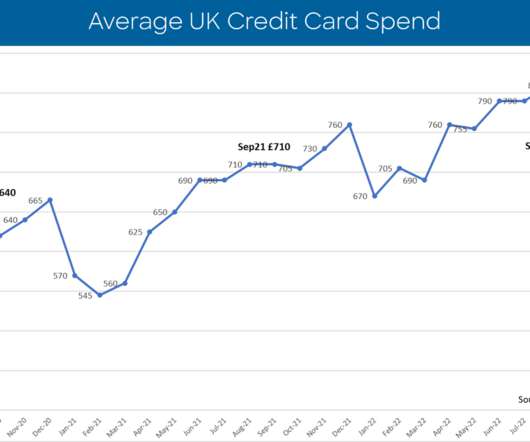

Our latest data on UK credit card trends shows financial volatility and higher levels of credit card spend, compared to 2022 – with monthly spend up by 6.7 The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK cardissuers. percent in April.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK cardissuers.

Amazon is rethinking returns, routers have been overrun by Russians and credit cardissuers may not yet be betting on sports gambling, regardless of what the Supreme Court says. Backers of the state’s gambling initiatives want the credit cardissuers to allow it. Amazon’s Returns Reset.

This partnership will also create opportunities for cardissuers in Southeast Asia to be part of a key strategic alliance in the travel and entertainment space, and bring the best benefits, experiences, and value to their customers. The partnership will also see SIA benefit from Mastercard’s suite of data and services capabilities.

This is an excellent time for banks, lenders and cardissuers to ensure they continually interact with customers to better understand their genuine financial position — especially if household incomes are likely to take a hit later in the year. Improving Customer Outcomes. by Bruce Curry.

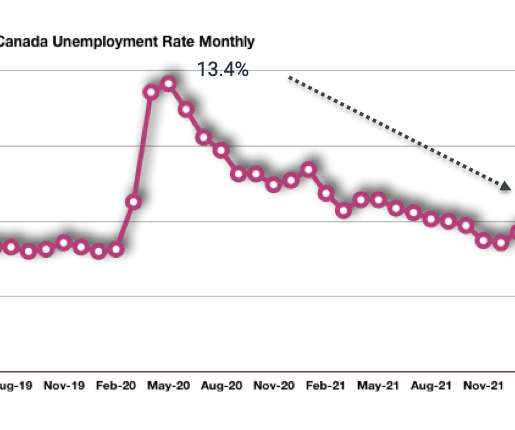

FICO® Advisors regularly monitor in-depth data reported by Canada’s leading credit cardissuers. These credit card performance figures represent a national sample of approximately 38 million consumer accounts from FICO client reports generated by the FICO® TRIAD® Customer Manager and Adaptive Control System solutions.

The gateway performs this function by connecting to debit card/credit card networks such as Visa, Mastercard, Discover, or American Express. It also reaches out to the credit cardissuer, which is the issuing bank or financial institution that provided the card to your customers.

For example, the interchange fees for online transactions may be higher due to the higher risk of credit card fraud. Interchange fees are set by credit cardissuers, such as Bank of America, Citi, or Chase, and are adjusted every year in April and October. Can merchants pass credit card processing fees to customers?

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service produced by FICO® Advisors, the business consulting arm of FICO. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK cardissuers.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content