This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Government agencies face mounting pressure to provide efficient, secure, and accessible payment options for their services, agencies, and constituents. Challenges in Government Payment Processing Government agencies manage a diverse range of payment types, including tax payments, permit fees, licensing, utility bills, and fines.

Episode Six (E6), a leading global provider of enterprise-grade payment processing and ledger infrastructure, today announces a partnership with payment solutions and services provider Secupay to provide asylum seekers with payment cards, enabling them access to financial support from the German Government.

Trustly , the global leader in Pay by Bank, and Point & Pay , a leading payment processing provider for government agencies, today announced an integrated product partnership. “This collaboration helps government agencies simplify their payment systems, reduce processing costs, and improve the overall customer experience. .

Consumers, businesses, and governments can use Visa Direct to deposit funds to bank accounts linked to eligible debit cards in real-time1. In addition to enhancing the cardholders experience, this update opens new avenues for businesses and governments to grow and thrive. Faster Payments Council (FPC).

SEAs young, tech-savvy population, a growing consumer base, reliance on informal financial systems, and supportive government initiatives aimed at financial inclusion serve as robust drivers for long-term growth. This demand is expected to fuel fintech innovations even in the face of current economic hurdles. Yet, optimism abounds.

Scalability Issues: AI systems demand thousands of transactions per second, far beyond current capacities. Key features include: Zero-Latency Transactions: Millisecond-level settlement speeds to meet real-time demands. Cost Barrier: High fees (2.9% + $0.30 per transaction) make microtransactions unviable.

On-Demand 440 registered Online Join this Webinar As VOP implementation across the SEPA region progresses, what are the practical next steps for financial institutions? Webinar The final countdown: What’s next for Verification of Payee? The Verification of Payee (VOP) deadline is just around the corner.

A growing young and middle-class The second driver Southeast Asia’s fintech boom is the regions growing tech-driven youth and middle class, two demographics that are fueling demand for digital-first financial services. Southeast Asia’s youth, aged 15 to 34, account for over a third of the population.

These restrictions were aimed at ensuring that the platform could manage the demand of Indias massive digital payment ecosystem while maintaining security and performance standards, the Financial Express reported. In India, WhatsApp Pay was initially introduced in 2020 with a 40 million user cap.

This comes as manual and in-house verification struggle to meet the crypto industry’s fast-paced demands. Instead, this method requires users to provide key details such as an identification number, which are then cross-checked against government databases. in 2023 to 2% in 2024. in verification times.

This demands a substantial investment of time and resources for the initial build, not to mention creating the significant ongoing burden of securing and maintaining compliance for the entire lifecycle of the system. Any service used for tokenization must scale to meet the demand of its clients.

Viewing these initiatives as a whole presents a clear regulatory trajectory: accelerated timelines, harmonised standards, and enhanced scrutiny across governance, conduct, and technology infrastructure. Strategic modernisation through modular, API-first architecture enables a phased, agile response to compliance demands.

On-Demand 230 registered Online Join this Webinar How is the macro-economic environment reshaping global trade and payment requirements? Currency diversification is accelerating; how are geo-political tensions and shifting trade flows reshaping global payment demands? But the geo-economic domain is not the only source of change.

Yet designing for offline-first use cases introduces technical complexity and requires careful consideration to balance user demand with practicality, though recent prototypes show that offline functionality can be achieved on standard smartphones without specialised hardware. Flexibility is also crucial when it comes to custody.

Primary Use Cases : CBDCs are designed to enhance financial inclusion, streamline payments, and provide a government-regulated alternative to cryptocurrencies and private digital payment providers. This demand has spurred initiatives like FedNow in the U.S. They remain a staple payment method globally.

Absorbing the PSR’s responsibilities into the FCA risks adding further complexity to an already demanding agenda, potentially disrupting the ongoing development and supervision of the UK payments ecosystem with a view to kickstart growth.

Singapore currently stands as the regional leader, or Champion, with exemplary ratings in market maturity and government initiatives. Regional integration is playing a key role, with governments accelerating their efforts to enhance cross-border commerce and digital economy participation.

This initiative aligns with the Qatari Government’s vision of digitalising payments, enhancing electronic banking services, and advancing the shift towards a cashless society. “These solutions aim to streamline payments for our corporate clients while augmenting security measures,” he stated.

This report provides a comprehensive analysis of the key trends defining the payments sector in 2024, highlighting the opportunities for strategic growth, as well as the challenges posed by regulatory pressures, financial crime, and evolving infrastructure demands.

These old-school platforms were never designed to meet the demands of todays always-on, customer-centric banking environment. BPCs SmartVista is a digital payments platform that enables banks, fintechs, and governments to manage a range of services including card issuing, digital banking, and real-time payments.

. “At LeapXpert, we’re seeing greater and greater demand for our platform, driven in part by the three-year crackdown by global regulators on off-channel communications,” LeapXpert Founder and CEO Dima Gutzeit said. “This is now expanding beyond regulated enterprises into non-regulated sectors, as the DOJ in the U.S.

In the survey report, ‘ Understanding Consumer Demand in the AI-Banking Era ‘, Personetics reveals that 84 per cent of respondents indicated that they would likely switch to a bank that provides timely, relevant advice to improve their financial health.

These insights are crucial for payment firms aiming to develop proactive strategies to stay ahead in this dynamic and demanding environment. The newly appointed Labour Government will be expected to unveil clear plans about how the regulatory framework will be shaped going forward. Why is it important?

While still central to security, modern tokenisation addresses broader demands: interoperability across platforms, reduced operational costs, and improved customer experience. The necessity of tokenisation in digital payments The traditional view of tokenisation as a fraud mitigation tool is outdated.

We are seeing strong adoption and demands for wallets like PayPal, Alipay, and WeChat Pay as they have evolved from basic payment tools to comprehensive financial ecosystems. Digital wallets are expanding faster than financial oversight can keep up, forcing governments to scramble for new safeguards without choking innovation.

Despite these advancements, many firms still rely on outdated payment systems and technologies that cant meet the market’s growing demands. As digital assets continue to gain traction, payment networks must evolve to accommodate rising transaction volumes, evolving regulatory frameworks, and the growing demand for real-time settlement.

As the global demand for faster, more affordable, and increasingly transparent cross-border payments intensifies, Project Nexus is emerging as a foundational initiative to meet the G20’s ambitious roadmap. By joining Nexus, banks can respond to that demand in a tangible way. All of this reflects what the G20 set out to achieve.

The move supports Vietnams growing demand for digital and contactless payments, particularly among younger, tech-savvy users. Most importantly, our partnership with NAPAS marks a significant milestone in our commitment to supporting the governments vision of realizing its non-cash payment goals in 2025.”

This model enables SMEs to receive funds quickly, improving their ability to respond to market demands or cover urgent expenses. Government support and favourable regulatory environments will play a crucial role. Quick, Digital Loan Approvals Unlike banks, fintech platforms offer a streamlined, digital loan application process.

MacKenzie highlighted this tension: Customers demand a zero-friction experience, especially in e-commerce and retail. Participants also touched on the potential for government-backed initiatives to facilitate data sharing. As McMurtrie summarised, Fraud is a collective problem, and it demands a collective solution.

Addressing these vulnerabilities demands collaboration across financial institutions, digital platforms, and regulators. Frequently used for high-value impersonation fraud, with scammers posing as trusted entities like banks or government officials. Why is it important? What’s next?

In Singapore, the government-backed API Exchange is promoting API standardisation. According to a study by Bain & Company, Google, and Temasek, 53% of industry experts believe that consumer tech platforms, rather than pure-play fintechs, are more likely to drive disruption in financial services. of all cashless transactions in Japan.

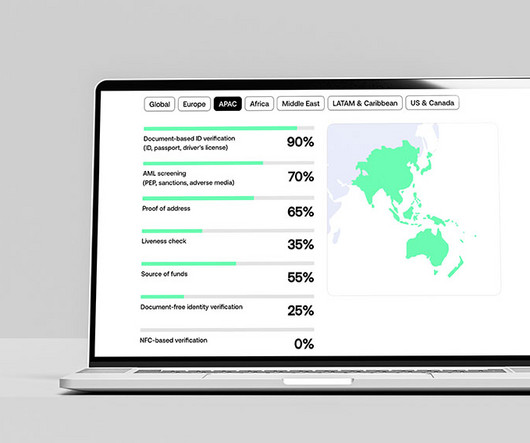

The way the ID verification works is that users upload a government-issued ID and take a selfie. iDenfy’s AML solution screens users continuously, not just at onboarding, to ensure QwikPay always stays ahead of evolving risk profiles and regulatory demands. The pricing model was another deciding factor.

This urgency often leads organisations to choose vendors who claim to deploy solutions swiftly to meet compliance demands. However, Armstrong warns that this desire for bespoke solutions can lead to miscalculation. “I I have quite strong views on why it might not be the best idea for some firms,” he claims.

Where profitability and mature governance take precedence over pure top-line expansion. It is also investing in machine learning -driven fraud prevention, real-time payouts, and open banking integrations to stay ahead of shifting market demands. Its core strength lies in controlling the entire payment stack.

They shine in markets where cash-in/cash-out, P2P transfers, airtime top-ups, and government disbursements are common. What is a digital wallet? A digital wallet, on the other hand, doesn’t hold money. It simply facilitates transactions by linking to your customers existing financial instruments, like bank accounts or credit/debit cards.

Businesses cite a broad mix of motivations, from lower transaction fees and faster settlements to a lack of consumer demand. Still, a sector-specific evolution is shaped by education, infrastructure, and market demand, with adoption predicted to increase gradually over the next three years.

This government is laser-focused on supporting business growth and expansion. Consumers demand payment choice, flexibility and transparency at checkout, and Affirm delivers all three. Affirm has been publicly traded on NASDAQ since 2021 and has processed more than $75 billion over the last five years.

This partnership with Fundiin is more than just a single undertaking – it is a strategic, long-term initiative designed to strengthen risk management, refine credit-scoring models, and introduce financial products that better meet market demands.”

government is laying the groundwork for regulations that will support the growing digital asset economy. Consumers want to use it, and with modern gateways eliminating risk and complexity, merchants can meet this demand safely and efficiently. Positioning for the Future The shift toward crypto payments isn’t slowing down.

The growing adoption of mobile and internet technology and rising consumer expectations for instant payment experiences will drive financial inclusion forward. In my view, organizations that prioritize the end-user experience will be the ones that lift the benchmark on what is possible and will continue to drive growth.

Standard Chartered Standard Chartered has a track record of working with stablecoin issuers globally, allowing the JV to fully utilise its bank-grade infrastructure and rigorous governance. “We are introducing solutions and instruments that service this market and meet the growing client demand.

The introduction of the Digital Assets Bill and the Financial Conduct Authority (FCA)s ongoing efforts to regulate cryptoassets demonstrates the regulator’s intentions to further define just how digital assets are governed and traded. Why is it important?

Stripes growth to date is evidence of the intense market demand for programmable financial services. We believe this ability will prove particularly important in the coming years, as stablecoins, AI, and other forces reshape the landscape. The associated transformation is still early. The post Stripes Total Payment Volume Reaches $1.4t

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content