Firms with revenues less than $25 million, mainstays of the Main Street economy, are particularly pressured. US Bank Chief Product Officer for Business Banking Shruti Patel provided an assessment of the sentiment among SMBs.

Results from a U.S. Bank survey show just where the worries lie, she said.

“Almost 60% to 80% of our respondents are feeling very overwhelmed with the macro environment stressors right now,” she said, adding that her unit’s focus is on enterprises with sales under the $25 million threshold. “The uncertainty around tariffs, the impact on cost of operations, whether they’re going to absorb the cost, pass it down, the rate environment, access to capital” are top of mind.

Many of these businesses are in a holding pattern, uncertain about what to do next.

“They’re in a pause mode right now,” she said.

Although there has been strong demand for capital through the bank’s Small Business Administration program, managing the obtainable capital has been a challenge, she said. Beyond financing, there’s a need for enhanced financial literacy and guidance on how to manage resources in a volatile market.

Launching Online Resources

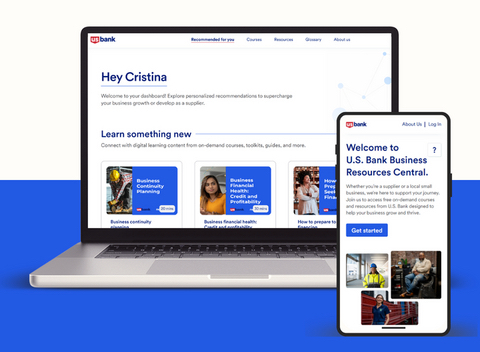

Last month, the bank launched U.S. Bank Business Resources Central (BRC). The free, online hub builds on the bank’s financial literacy and community access initiatives, said Patel, who added that the business access advisor program was set up in 2021.

The online offering, launched in collaboration with Next Street, a firm focused on training programs for small businesses, functions as a sort of Coursera for enterprises.

The overarching goal is to provide foundational business skills that remain relevant regardless of economic shifts. The collaboration uses Next Street’s experience to co-create content that addresses the broader needs of small businesses beyond banking and payments, Patel said.

The functionality of the BRC is centered on ease of access and comprehensive educational offerings. The hub is “open not just to U.S. Bank clients but is actually open to everyone,” Patel said.

The content (contained in 10 courses) covers essential topics such as how to secure financing, protect against cybercrime and improve digital literacy.

There’s also emphasis on artificial intelligence, given its growing adoption by small businesses.

“We made AI a very big portion of the business resource hub because we hear a lot from our customers … that they are deploying AI more and more in everyday operations,” Patel said. “Almost 80% of our small business survey respondents deploy AI. They’re trying to minimize the cost of their operations.”

The hub offers dedicated toolkits to help businesses learn about and use AI tools for efficiency and cost reduction. The content is also customizable, tailored to the specific industry and stage of development of each small business.

Beyond general business acumen, the BRC also helps SMBs navigate specific opportunities, such as becoming vendors for larger institutions, with the help of the business access advisors that act as procurement specialists and are located across more than a dozen markets around the United States.

The focus on active use and return visits will help fine-tune the platform’s value to SMBs, Patel said.

“The success of the platform is all about keeping up with the challenging times and continuing to iterate on the curated content to make sure that engagement metrics stay high,” she said.

Early results show that nearly 20% of users in the initial weeks are already defined as U.S. Bank customers, and many are reaching out for one-on-one coaching. U.S. Bank is promoting the BRC through various marketing channels, including publications and social media, and through direct outreach by its business access advisors in communities across its footprint markets.

“If we can help small businesses, whether they became a vendor, whether they get access to capital, whether they were able to understand how they can [undertake] sustaining and growing their business, that would be a big success story for us,” Patel said.