This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Deutsche Bank has joined the extended Series B funding round for blockchain-based fintech firm Partior , bringing the total raised to US$80 million and marking the close of the round. Established in 2021 and backed by DBS Bank, J.P. Morgan, Jump Trading Group, Standard Chartered, Temasek, and Valor Capital Group.

Fewer correspondentbanks to move that money. For instance, the number of active correspondentbanks fell about 23 percent in advanced economies, but as much as 41 percent in developing nations. And earlier this year, Harbour & Hills CEO Rahul Tripathi took note of the vagaries of correspondentbanking. “I

Global asset manager and Swiss bank UBS has developed and successfully piloted a blockchain-based payment solution, aiming to increase efficiency and transparency, as well as enable the programmability of money movements for corporate and institutional clients.

For foreign payment service providers looking to facilitate cross-border B2B payments into China, the correspondentbanking model often remains the only route to facilitate clearing and settlement. “Getting correspondentbank accounts is the biggest challenge every payment service provider is facing.

There has been, seemingly, a parade of announcements geared toward bringing B2B payments into the digital age, bringing about the end of paper, speeding the time for settlement of transactions and making payments across borders cheaper and more transparent. The settlement timeframe of a single day means, too, that there is no chargeback risk.

Partior, a fintech known for its global unified ledger based interbank rails for real-time clearing and settlement, has announced the first close of an over US$60 million Series B funding round led by Peak XV Partners, with participation from Valor Capital Group and Jump Trading Group as new investors. Existing shareholders J.P.

This collaboration with Circle marks a step towards compliantly leveraging stablecoins and blockchain infrastructure to boost the Onafriq payment network. Currently, over 80 per cent of intra-African payments route through correspondentbanks outside the continent and settle in foreign currencies such as the US dollar or the Euro.

The Bank for International Settlements (BIS) has launched Project Rialto to test the potential for improving instant cross-border payments through a combination of a modular foreign exchange (FX) component and wholesale central bank digital currencies (wCBDC).

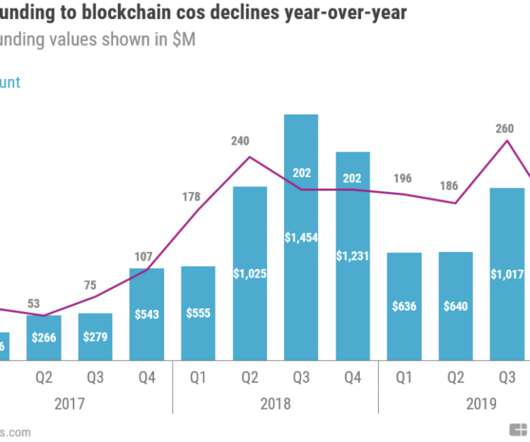

Blockchain companies have lost a step in the private markets. GET the 47-page blockchain TRENDS report. Download the free report to learn about the biggest emerging trends in blockchain and strategies to watch for 2019. Still, investor activity shows there are pockets of potential in the blockchain sector worth tracking.

The First Deputy Governor of the central bank of France, Denis Beau, spoke in support of a blockchain-based settlement system that would allow for faster transfers of euros, as well as be more cost-efficient, according to a report by Yahoo!

The blockchain has a bit of an identity crisis. And while it might be tempting to poke fun at those confident, if somewhat confused, CFOs, Adam Ludwin, co-founder & CEO at Chain , told Karen Webster that, actually, they are pretty much in the same boat as everyone else when it comes to the blockchain. “No Here’s a little proof.

Enterprise software provider R3 is teaming up with Mastercard to establish a blockchain solution for cross-border payments, the companies said in a press release on Wednesday (Sept. The new blockchain-enabled solution aims to bridge international payments infrastructures, schemes and banks via a Mastercard clearing and settlement network.

Visa, of course, announced its B2B Connect network, which will streamline 30 global trade corridors (to start) via fiat-based transactions settled over blockchain. The strategic move also has a financial component, as Ripple took a $50 million stake in the money transfer company. The Roadmap. “I

Blockchain and AI to the Rescue. Some payments providers are also leveraging blockchain and distributed ledger technology (DLT) to meet these needs, expediting the cross-border payment process. Canadian payments network Interac is also investing in blockchain and DLT solutions.

Increasingly, the financial services industry is targeting sluggishness in corporates’ cross-border payments, too, through technologies like blockchain and the development of faster payment rails around the globe. Some solution providers like Ripple are introducing new ways to bypass the correspondentbanking system entirely.

Beyond cryptocurrencies, blockchain is making wakes as a conduit for transactions. And there are a number of initiatives from banks in that country to use blockchain to exchange assets. The digital asset facilitates the trade and supplies important settlement instructions.”

. “Swift’s own strategy for instant and frictionless transactions is closely aligned with the G20 targets, and 89 per cent of transactions on our network now reach the recipient bank within an hour – ahead of the G20’s 2027 goal of settlement within an hour for 75 per cent of international payments.

Accenture Backs Blockchain. Professional services firm Accenture is backing blockchain in a big way, announcing this week that it will collaborate with TradeIX to support corporate onboarding to the blockchain-powered trade finance platform of the Marco Polo Network. Credit Unions Mix Blockchain With Existing Rails.

Aleks Stefanovski, VP for strategy and business operations at Visa “Another barrier is de-risking by correspondentbanks. Most cross-border payments are processed on infrastructure provided by correspondentbanks. “Over the past decade, the risk appetite at correspondentbanks has declined.

In addition, innovators the world over are exploring how technologies like blockchain could address payments speeds and efficiency on an international level. Payments experiences are far from ubiquitous from market to market, however, and a global payments settlement agency is now pressing for faster cross-border payments at a global scale.

Blockchain — or rather, blockchain-focused projects — has been in the spotlight as China has been trialing financial services (FinServ) and security measures across those rails. However, blockchain is also gaining ground, and currency is offering a boost to the payments infrastructure. Africa As Greenfield Payments Opportunity.

This is particularly true as improving the payment experience, in terms of velocity of settlement, transparency and traceability, is a positive impact on commerce by [making it easier to do] business in places like China.”. It could be key to the broader Chinese economy too.

The company also announced this week that it was shortening its name to “Ripple,” representing the technology’s emergence as an enterprise-grade solution and the debut of two new products for banks: Cross-Currency Settlement and FX Market Making. International transaction banking service.

Yet at the same time, according to a survey by The International Securities Association, 55% of companies polled are monitoring, researching, or developing solutions on top of blockchain. But this very loud and public backlash against cryptocurrencies from banks begs the question: What do banks have to be afraid of?

This week, SWIFT picks the latter, while JPMorgan Chase grows its initiative using blockchain to make cross-border transactions, and Form3 announces a new international payment services that connects banks with global small business payments capabilities via application programming interface (API).

With growing demand for faster, cheaper alternatives, fintech firms and blockchain solutions are emerging as real challengers. How Cross-Border Payments Work International payments rely on a network of correspondentbanks. When sending money abroad, banks often do not have direct relationships with every foreign institution.

Despite this immense potential, cross-border payments in LAC remain hampered by inefficiencies in the traditional SWIFT-based correspondentbanking system, marked by multiple intermediaries, settlement delays, and fees exceeding 6% for remittances for some corridors. billion, exceeding the $4.3 trillion by 2030.

The correspondentbanking model together with SWIFT was built 50 or 60 years ago to facilitate a small number of large payments. He believes this kind of hybrid model is essential to meet institutional needs, particularly as blockchain-based infrastructure becomes more viable for regulated financial services.

News came this week from Ripple, which has a presence in both the cryptocurrency and blockchain realms, that 13 more financial institutions have signed on RippleNet. Among the new additions to the roster: Euro Exim Bank, Ahli Bank of Kuwait, Pontual/USEND and others. Of Cryptos And Blockchain.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content