This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

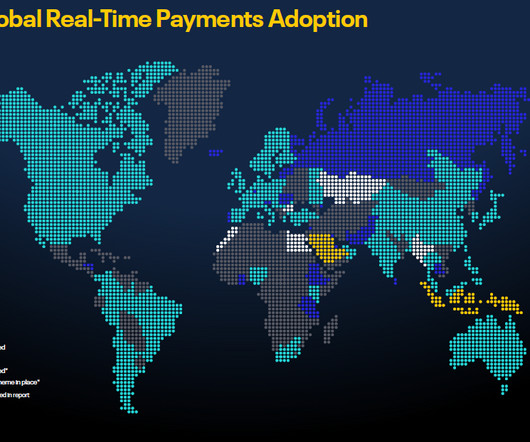

RTP technology facilitates payments across all payment categories, including business-to-business (B2B), business-to-consumer (B2C), consumer-to-business (C2B), peer-to-peer (P2P), government-to-citizen (G2C), and account-to-account (A2A) transactions. Current status of RTP adoptions around the world How RTP is used?

As a result, he predicted that the entrenchment of faster payments will be a linear progression that moves from consumer-to-consumer (C2C) to consumer-to-business (C2B), then to business-to-consumer (B2C) to business-to-business (B2B). So, from the beginning, start with the individual consumer. Particularly in the U.S,

Demand is also heating up for real-time gross settlement (RTGS) systems. Such was the case in Hong Kong, where the existing RTGS system was only serving high-value interbank transactions, leaving peer-to-peer (P2P) and consumer-to-business (C2B) payments to languish. USD) per transaction.

It is a bit of a curiosity – particularly since this new settlement window is not exactly new news. A third settlement window was part of NACHA’s original announcement in May of 2015 , of the unanimous adoption of SDA by all of the FIs in the U.S. In fact, it’s more like four years old.

Originally, faster payment systems were primarily focused on the retail market [person-to-person (P2P) and person-to-business (P2B)], but increasingly business payments [business-to-person (B2P) and business-to-business (B2B)] are taking advantage of the benefits that faster payments offer,” FIS wrote in its report. Switzerland.

In the always-on, 24/7/365 economy, payments that circle the globe should conceivably be as simple as those made in a peer-to-peer (P2P) transaction. The transaction wends its way across borders, in the middle of the night, settling instantly. The reality? API Advantages.

After two decades of tweaking and updating its existing Real-Time Gross Settlement (RTGS) system, Hong Kong determined it needed a new rail. RTGS was designed to support high-value, interbank transactions, but P2P and C2B payments typically took a day or two to clear, were processed only during work hours and cost up to HK $200 (US $25.5)

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content