This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Thats why 92% of consumers and 82% of companies reportedly made the switch to electronic payments, like Electronic Funds Transfers (EFT) and Automated Clearing House (ACH). Checks can bounce, and cash can get lost. EFT and ACH payments are fast, secure, and hassle-free. Thats Electronic Funds Transfer (EFT) in action.

When did you last use cash or check to pay for something? And on that note, two of the most common modes of electronic funds transfer are ACH and wiretransfers. In this post, we’re going to review ACH and wiretransfers, look at their similarities, and then see how they compare against each other.

But cash and checks are rapidly declining as preferred modes of payment. If you’ve been accepting and using electronic payments in your business, you’ve probably come across two of the most popular terms in the digital payments scene— automated clearing house (ACH) and wiretransfer. No fees on the receiving side.

ACH credit payments are best for sending one-time payments whereas ACH debit payments are more suited for making regular payments, such as for monthly utility bills. All ACH payments are secure and reliable, available 24 hours a day, 7 days a week, and 365 days a year. Learn More What are ACH Credit Payments?

TL;DR You get to choose from traditional payment methods like cash and checks, online payment methods like digital wallets and ACHtransfers, and emerging payment methods like BNPL services and cryptocurrencies. ACH payments are also reversible, while wiretransfers cant be reversed once completed.

Wiretransfers and electronic funds transfers have been staples of financial transactions for decades, but various electronic transfer methods have emerged with the innovation in banking technology. ACHtransfers are common for low- or mid-value payments that don’t require immediate settlement.

First, let's delve into the mechanics of ACH and Wiretransfers, followed by an exploration of their distinctions, guidance tailored for small businesses, and concluding with instructions on establishing ACH and Wire processes. What is ACH? It's a massive upgrade to the traditional paper checks.

According to the firm, B2B transactions were a key driver of ACH transaction growth in the third quarter of the year, leading NACHA Chief Operating Officer Jane Larimer to describe the ACHNetwork as “thriving.”. More people than ever are benefitting from Same Day ACH. today, but it’s not the only one.

ACH payments are a convenient way for business owners, individuals, and employers to use intuitive automated banking throughout their daily lives. Most small business owners and employers are turning to ACH payments instead paper check payments because of the ease and instant access the ACHnetwork provides.

An EFT payment isn’t just one type of payment – several different types of EFT payments come under the Electronic Fund’s Transfer umbrella. These can include using a credit or debit card, an electronic check, or an ACH (Automated Clearing House) transfer. Electronic Checks. WireTransfer.

“If you want to originate on a card network, but pay out through an ACHnetwork, let’s do it. If you want to originate an ACH and pay directly to an account, we can do that as well. And Eliminating The Check Is A Good Start. SMBs Need Help.

Introduction If you’re still paying your vendors with paper checks, you’re likely facing several issues for your business - like tons of manual effort, difficulty tracking payments, high fees on checks, and so on. Checks are a slow process with many steps on both ends.

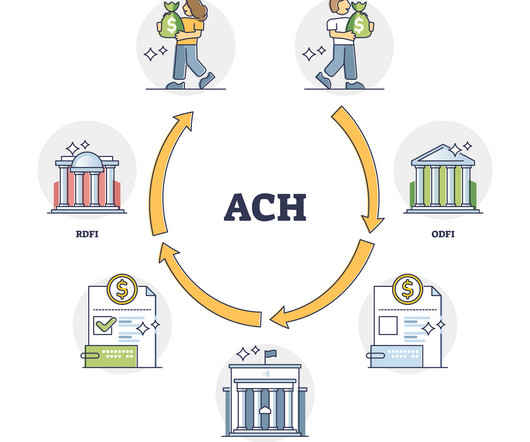

ACH stands for Automated Clearing House, a network that handles electronic payments and transfers. So, what is an ACH deposit? It’s a way to move money directly from one bank account to another without using paper checks, credit cards, or cash. ACH direct deposits are common. What Is an ACH Deposit?

Types of ACHTransfers Direct Deposit Direct deposits are electronic transfers of funds from governments or businesses directly into a recipient’s bank account. By using direct deposits, recipients can access their funds quicker and more securely compared to traditional paper checks.

Read on and learn everything you need to know about ACHtransfers , including their types, benefits, potential downsides, and their alternatives. What Is ACH Bank Transfer?: ACHtransfers are electronic, bank-to-bank money transfers processed through the ACHnetwork.

It is a system of transferring money from one bank account to another without the use of paper checks, or cash. One of the advantages of EFT is that it's relatively quick - payments can be processed and transferred within a few days. Checking accounts allow you to write checks and use a debit card to make purchases.

It is a system of transferring money from one bank account to another without the use of paper checks, or cash. One of the advantages of EFT is that it's relatively quick - payments can be processed and transferred within a few days. Checking accounts allow you to write checks and use a debit card to make purchases.

What are ACH payments? ACH payments refer to electronic funds transfers (EFTs) between financial institutions using the ACHnetwork. ACH payments offer a secure, reliable, and cost-effective way to transfer funds for payroll, recurring bill payments, direct deposits, and other routine transactions.

With the introduction of electronic funds transfers (EFTs), gone are the days of paper checks and manual money handling. For businesses , EFTs simplify the payment process by allowing direct payments, reducing the administrative workload associated with handling paper checks and enhancing the speed at which transactions can be settled.

What Exactly is an ACH? Depending on your end goal, there are a few different types of ACH. They pretty much break down into ACH payments and ACHtransfers, both encompassed within the ACHnetwork. ACH payments are strictly transferred between banking institutions. Platforms Used.

TL;DR An Electronic Funds Transfer is an umbrella term for payments that are conducted electronically—essentially, any payment method except for cash and paper checks. An Electronic Funds Transfer is an umbrella term for payments that are conducted electronically—essentially, any payment method except for cash and paper checks.

ACH (Automated Clearing House) payments are basically EFTs ( electronic fund transfers ) that use the ACHnetwork to move funds between bank accounts in the United States. ACH is most commonly used for direct deposit of payroll, payment of bills, and business-to-business payments.

Take, for instance, the finding that the majority of cross-border payments are conducted via wiretransfer, according to Tipalti’s report. According to Israch, wire’s popularity largely stems from its familiarity among finance departments. “I The biggest problem with wire is that it’s very expensive,” he added.

While there has been some innovation in wage payment mechanisms as more employers shift away from the paper check toward direct deposit and payroll cards, little has changed about the timing of those payments. It’s also opened up conversations about how professionals get paid. Balancing Employer-Employee Needs.

Also keen on the Fed’s involvement were the community banks and credit unions that worry (as they should) about having TCH as the only operator of an RTP network in the U.S. and one of two operators of the ACHnetwork in the U.S., TCH is the association of the 25 largest banks in the U.S., the other being the Fed.

Before diving deeper into SEC codes, let’s take a minute to better understand ACH transactions – if you’ve already worked with ACH transactions and have an idea about what is involved in them, you can skip this section and go straight to SEC codes. There is a number of situations in which ACH payments are used.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content