This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

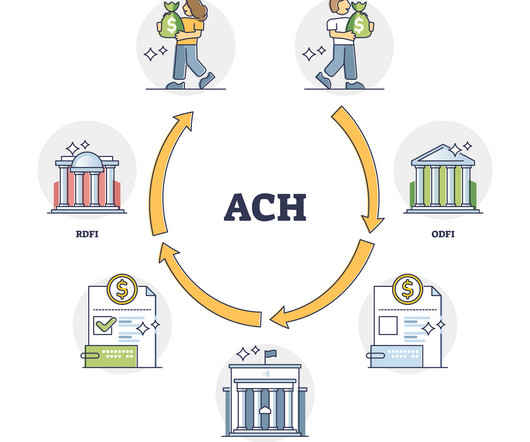

ACH (Automated Clearing House) transactions are electronic money transfers from one bank to another processed through the ACH network. The customer must give the originating bank or financial institution authorization to debit or credit their savings or checking account.

With ACH debit payments, the recipient is in control, so these payments are pulled, rather than pushed. A customer authorizes these electronic payments by indicating it’s their preferred payment method for recurring bill payments or other essential funds transfers such as an annual tax payment. Health insurance and premiums.

Many small businesses choose ACHoperators because they are more convenient than most direct deposits. ACH transfers don’t come with high fees and transactions and they’re easily edited if an employer wants to adjust payroll, extend bonuses, or reimburse an employee. Q: What’s the difference between a check and ACH?

They give their bank a request to send funds through the ACH network. The bank then packages this request into a digital file, which gets sent to an ACHoperator. This operator acts like a middleman, making sure everything is in order and routing the payment to the right place.

Payment automation systems are usually built into a comprehensive AP automation system that encompasses various processes, including invoice capture, coding, review, approval, payment authorization, and payment execution. The originator bank compiles all the POs and sends them to an ACH for processing.

Some of the most common ACH return codes are caused by incorrectly entered information or insufficient funds available, while others can be more complicated and include issues with authorization and more. What Are ACH returns? ACHOperator The ACHOperator links the two accounts by processing transactions (e.g.,

An SEC (Standard Entry Class) code is a code made up of three letters that explains how a specific ACH transaction was authorized by the business or a customer that received it. The codes are universal, and they are maintained and defined by NACHA, which has jurisdiction over the ACH network. SEC Codes – The List.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content