This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Community Your feed Latest expert opinions Groups Join the Community 23,479 Expert opinions 41,848 Total members 350 New members (last 30 days) 190 New opinions (last 30 days) 29,133 Total comments Join Sign in Stablecoin – CrossBorderPayment Driver?! To cover modern payments needs this has not helped.

UK’s regulator FCA working with the Bank of England has published proposals for issuing stablecoins, crypto custody and financial resilience of crypto-asset firms, to provide a safe, competitive sector. Market Size Value of cross-borderpayments is estimated to reach a minimum $ 250 trillion by 2027.

The launch comes as stablecoins emerge as key tools in global finance, offering real-time settlement, reduced costs, and increased accessibility for cross-borderpayments, especially in hard-to-reach markets that still face challenges with correspondentbank networks and financial inclusion.

Cryptocurrencies introduce new money laundering risks (e.g. The result is that crypto companies now face compliance burdens very similar to banks, often without the decades of infrastructure banks have built.

Today, Ripple , the leader in enterprise blockchain and crypto solutions, announced a new partnership with Clear Junction , the global leader in cross-borderpayments solutions for regulated institutions. The post Ripple Partners With Clear Junction to Enhance UK and EU Cross-BorderPayments appeared first on Fintech Finance.

So, why do cross-borderpayments present so many challenges? Despite rapid market growth, international payments have been hampered by country-specific regulations, while transactions being channeled through intermediary banks can take days to complete and often come with fees. Currently, there are 0.7

There has been, seemingly, a parade of announcements geared toward bringing B2B payments into the digital age, bringing about the end of paper, speeding the time for settlement of transactions and making payments across borders cheaper and more transparent. The Volatility. dollars), less the 1 percent fee.

How MSBs are leveraging the power of USDC and Circle for cross-borderpayments to their counterparties. As cross-borderpayments continue to gain popularity, businesses are constantly looking for faster, more secure, and cost-effective methods to conduct transactions.

Individual jurisdictions around the globe are pressing for both faster and more efficient cross-borderpayments. China’s central bank, for instance, took steps last month to boost the efficiency of cross-border transactions involving Chinese parties by lengthening its clearing window time span.

June was a busy month for cross-borderpayments — done across currencies and time zones, between consumers and corporates. No doubt by now most payments watchers are familiar with Libra , the Facebook plan to bring a new global cryptocurrency to market that seemingly seeks to do nothing less than upend global banking.

Corporate payments are still not a guaranteed use case for cryptocurrencies. Wirex , which providers consumers with an account to store both fiat and cryptocurrency, recently stepped into the corporate finance space with the launch of its business account. Cross-BorderPayments Friction.

He said that “disorderly approaches and heterogeneous adaptations” could happen if the bank didn’t take decisive action. DLT would also help in terms of cross-borderpayments, he said.

The volatility of cryptocurrencies and their existence in what’s often a grey area of regulatory compliance make businesses operating in this sector an unattractive target for traditional financial institutions. ius offered insight into exactly why crypto businesses are so difficult to bank. As Karalevi?ius

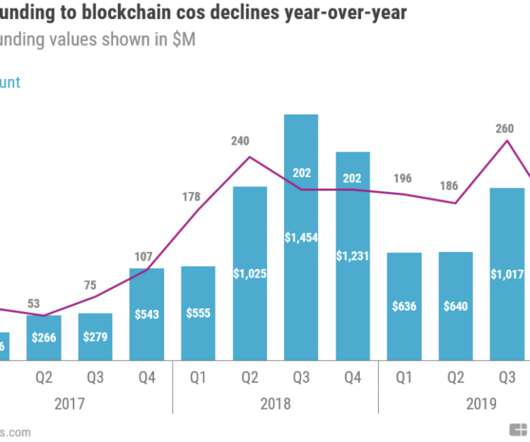

Entrepreneurs have pitched applications for blockchain technology ranging from supply chain tracking to financial asset settlement, but the only one that has found adoption at any significant scale so far is cryptocurrency creation and trading. The companies raised $400M and $321M, respectively, both contributing to 2018’s spike.

B2B cross-borderpayments company Ripple offers an alternative to transferring money via the correspondentbanking system, which has long faced criticism for being slow, opaque, and costly.

FinTech innovators are finally paying attention to the B2B sphere, and much of that focus has landed on the cross-borderpayments space — a notoriously clunky, expensive and opaque burden for many business payers. Traditional banks are often at the center of that global B2B payments friction. Regulatory Burdens.

Because it leverages stablecoins, the company does not rely on outdated SWIFT and correspondentbanking rails and is able to deliver faster, more reliable, and cost-effective cross-borderpayments between developed and emerging markets.

Beyond cryptocurrencies, blockchain is making wakes as a conduit for transactions. And there are a number of initiatives from banks in that country to use blockchain to exchange assets. In other payments infrastructure-related offerings, some marquee names have made some strides.

One of the more loaded revelations from the report: Banks really only have to worry about disruption from blockchain technology in some aspects of the financial system, like trade finance, and less so in other aspects, like cross-borderpayments.

“We offer a single API across all banks,” Kirsch told Webster. He emphasized that the company’s aim is to help move digital currency — that is, digital forms of fiat currency — across bank rails, and that it has nothing to do with cryptocurrency, which is still an unwelcome concept to many financial institutions (FIs) and payments players.

Cryptocurrency Acceptance: Not Just Rumors Cryptocurrencies like Bitcoin and Ethereum have been making headlines for years , and in 2024, they are expected to become more widely accepted as a legitimate form of payment.

Absent the traditional banking role of money creation, he said, individual consumers would not be able to obtain mortgages or finance car loans because there would not be enough money to go around. The digital cryptocurrencies can’t function with the same flexibility and economic impact as fiat , then, and blockchain doesn’t scale.

Cross-borderpayments are rarely quick and transparent, and moving money across borders through the traditional channels is becoming more difficult. percent drop in correspondentbanking last year. percent drop in correspondentbanking last year.

But this very loud and public backlash against cryptocurrencies from banks begs the question: What do banks have to be afraid of? We’ll provide the definitions and analogies you need to know for bitcoin, blockchain, cryptocurrencies, and more. The short answer is “a lot.”. What is blockchain technology?

Regulatory shifts are paving the way for banks to engage with stablecoins. These are rapidly evolving from a niche vertical in the cryptocurrency ecosystem into a foundational element of the global financial system. This record high is driven by a wave of adoption from major global banks. How stablecoins work?

McDonald’s crossed the threshold from millions of burgers to billions served. News came this week from Ripple, which has a presence in both the cryptocurrency and blockchain realms, that 13 more financial institutions have signed on RippleNet. Social media firms count subscribers in much the same way. The firm stated Tuesday (Jan.

Another 2024 survey by ConsenSys and YouGov found 57% of 901 adults familiar with cryptocurrencies reported too many scams as their main concern with the technology. One of the greatest challenges to further adoption of digital assets is concern over scams.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content