This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Indigenous Banking (Shroffs and Mahajans): Long before modern banks, India had a thriving indigenous banking system. These banks introduced formal ledger-based accounting and cheque payments. This expanded the reach of formal banking to rural areas. This introduced standardization and divisibility.

After the June 2007 announcement of Apple’s first-ever iPhone and the ensuing buzz around iOS apps, financial institutions (FIs) began developing offerings to ease digital banking. Twelve years later, however, mobilebanking has become ubiquitous across much of the global financial ecosystem.

It may have started in 2007 when the U.K. launched its Faster Payments scheme, after the regulator said the banks had to comply, but has amped up ever since, as regulators in a few other countries have followed in the U.K.’s Topic Two: Banks — sure, they’re boring as all get out, but they are innovating. s footsteps.

In fact, we’re seeing it happen in a variety of retail, banking and broader commerce pilots and prototypes today. It’s also why mobile order ahead has seen such speedy growth. Over the last five or so years, consumers have increasingly used their mobile devices and apps to discover and buy things. Here’s why.

household held five mobile devices. Likewise, the rate of online fraud attacks on retailers has doubled, up 137 percent year over year in the first quarter of 2016. This will tie banks up while examiners search for any indication of wrongdoing. From 1992 to 2007, it traded on the NYSE before being taken private by KKR.

The cost associated with check processing and the lose-lose business model for check clearing imposed on banks by the Fed is one of reasons that checks are such a drag on the financial system. In fact, my bank loses the use of those funds the minute that the check is presented, regardless of when Bryan uses the money.

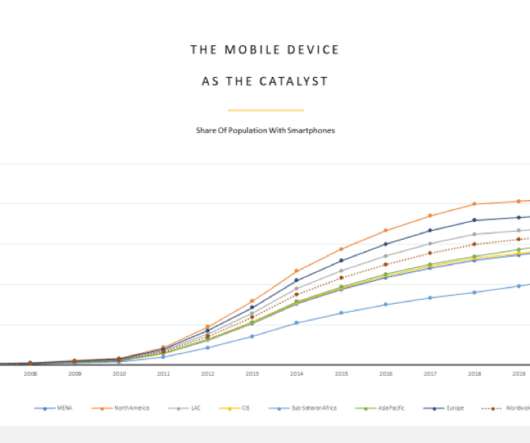

The introduction of the iPhone in 2007 – and the birth of the apps ecosystem a year later in 2008 –inspired an entirely new class of innovators, stating the 2010s with a brand-new toolkit. Armed with new tech, mobile devices, data and the cloud, they fast-tracked the shift from a largely analog world to the app-based economy of today.

The introduction of the iPhone in 2007 – and the birth of the apps ecosystem a year later in 2008 –inspired an entirely new class of innovators, starting the 2010s with a brand-new toolkit. Armed with new tech, mobile devices, data and the cloud, they fast-tracked the shift from a largely analog world to the app-based economy of today.

But he went on to hit a career 755, a feat that no one came close to matching until 2007, when Barry Bonds broke that record. Card Payouts is a card-based, front end user experience that integrates with treasury banks’ existing infrastructure. The cards will be usable for dipping, swiping and for entrance into a mobile wallet. “At

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content