This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

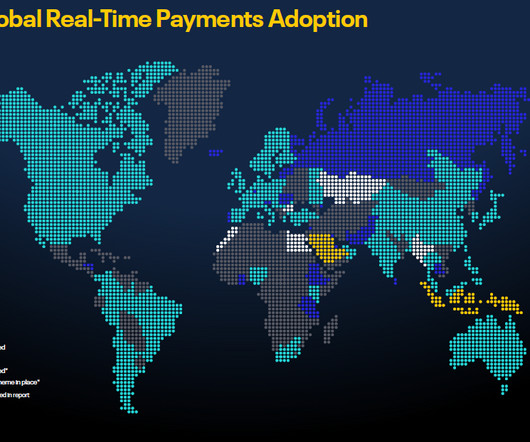

Introduction on RTP and its adoption around the world. While real-time payments (RTP) was previously considered an infrastructure luxury, it has now become a common method of payment in many parts of the world. Digital and RTP payments have dramatically accelerated the pre-existing, but slow-moving trend, away from cash and checks.

When The Clearing House (TCH) unveiled the Real-Time Payments (RTP) system in 2017, it propelled swifter payments and brought about the next generation of fund transfers. Payment solution providers are now also getting in on the real-time game and supporting a growing list of RTP use cases that use the network for rapid transaction speeds.

With the system joining the existing RTP system, both promising to modernize the way money moves and allow for greater use of instant payments, it seems the shift to real-time payments is 'inevitable'. FedNow may not interoperate with RTP, and it doesn't seem to be a priority for either. What are your options?

These payments offer instant round the clock transfers for B2B (Business-to-Business), B2C (Business-to-Consumer), C2B (Consumer-to-Business), and P2P(Peer-to-Peer). RTP makes it simple to move money. With RTP, businesses can manage their cash flow on a second-to-second basis that minimizes working capital.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content