This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It accelerates the adoption of A2A payments across all transaction types: P2P, B2C, C2B, B2B WHAT ABOUT THE DIGITAL EURO? The agreement lays the groundwork for true operational convergence between well-established solutions and a next-generation infrastructure.

As a result, he predicted that the entrenchment of faster payments will be a linear progression that moves from consumer-to-consumer (C2C) to consumer-to-business (C2B), then to business-to-consumer (B2C) to business-to-business (B2B). Yet, Kresse pointed out that, ultimately, individual consumer behavior drives changes in business behavior.

In Vietnam, SmartPay started with C2B payments as transfers within its mobile wallet ecosystem, and later introduced QR code payments for both old and new merchants. Integrating these solutions on the same platform alongside existing channels and methods gives acquirers an additional competitive advantage — a lower TCO.

It’s just one example Sinha provided of how treasurers have the opportunity to streamline and standardize the experience by guiding their firms in developing the payments experience for shoppers, while simultaneously mitigating financial risk for their organizations.

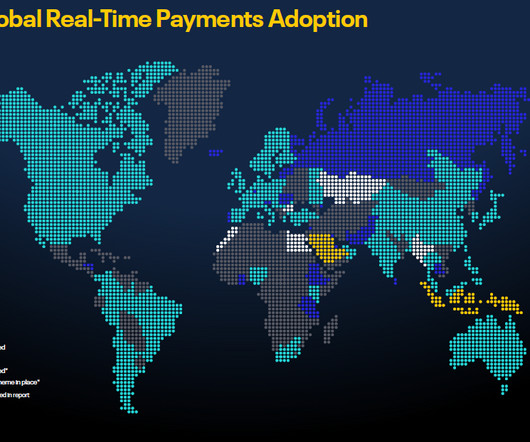

RTP technology facilitates payments across all payment categories, including business-to-business (B2B), business-to-consumer (B2C), consumer-to-business (C2B), peer-to-peer (P2P), government-to-citizen (G2C), and account-to-account (A2A) transactions. Current status of RTP adoptions around the world How RTP is used?

Regardless of whether payments are B2B or C2B, he said the trend has been clear: “You want to be able to choose between which payment instruments you are going to be using at the time of your choosing. The rising tide of card-not-present transactions and digital commerce also brings security Issues to top of mind, noted Cole.

And in looking toward the evolution of real-time payments, he said it’s likely the movement will be from P2P to consumer-to-business (C2B) — especially in paying small businesses such as lawn care companies or car repair shops. He said, too, that Fiserv has been collaborating with banks on real-time decisioning and data analysis.

Fiserv comes to the conversation with 30 years of insider industry knowledge, and on the heels of a year in which it moved more than $75 trillion across 30 billion digital payments in peer-to-peer (P2P), consumer-to-business (C2B) and business-to-consumer (B2C) transactions. In other words, it’s seen some stuff. Alphabet Soup.

90 percent | Percentage of banks that say they have major concerns about data management, per a report released last week by Wolters Kluwer’s Finance, Risk & Reporting, developed in conjunction with Risk.net.

They’re just a few of the latest developments covered in the Faster Payments Tracker, and there are clear implications for peer-to-peer (P2P) and consumer-to-business (C2B) transactions. But a clear indication of how these developments could impact the B2B payments space remains elusive.

Consumer-to-Business (C2B) C2B eCommerce reverses the traditional buyer-seller relationship. C2B platforms allow businesses to tap into a pool of talented individuals, freelancers, and influencers who can contribute their skills and expertise. It occurs when consumers offer products or services to businesses.

Use cases for Mastercard Send and Visa Direct range from P2P to C2B in the gig economy world – and B2C for disbursements supporting a diversity of use cases, including tax refunds, insurance claims and on-demand payroll for W-2 workers. But it actually puts them at great risk. Take the Fed. Watch that space, carefully. RTP and Faster.

And consumers are at risk of abandoning their purchases if they can’t pay quickly and with minimal hassle. RTGS was designed to support high-value, interbank transactions, but P2P and C2B payments typically took a day or two to clear, were processed only during work hours and cost up to HK $200 (US $25.5) per transaction.

Whether payments are moving between individuals (peer to peer, or P2P) or between consumers and businesses (C2B), they flow most easily from like to like — for instance, if the sender wants to use PayPal, the recipient must also have an account. They were lower risk and invited less fraud. That’s why ubiquity is so desirable.

Eco-Mail’s exchange-based technology eliminates physical mail delivery for mailers, consumers and large enterprises by using its proprietary platform to eliminate paper-based B2B, C2B and B2C mail. ID Analytics brings patented analytics and real-time behavioral insight to consumer risk management.

The next-highest category, consumer-to-business (C2B) cross-border payments, paled in comparison at just $54 billion. ” In large-value corporate global payments, squeezed foreign exchange margins, cyber risks and compliance burdens have bared their weight on revenues and, as a result, on the ability to innovate.

Limitations and Risks of Zelle While Zelle is fast and easy to use, it does have a few limitations and risks: No Payment Reversals: Once you send money via Zelle, you can’t cancel the transaction. Secure Network: Zelle operates through established banks, making it a secure way to transfer money.

Early Warning, which bought clearXchange , is expanding its banking network to enable real-time solutions between banks for B2B, B2C, C2B and C2C solutions. It’s exciting and exhilarating at the same time it is terrifying and filled with risk. But knowing what questions to ask, and when, is part of the journey.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content