This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

UDPN is a DLT-underpinned messaging backbone focused on providing interoperability between the fast-growing number of different regulated stablecoins, tokenized deposits, and CBDCs, and seamless connectivity between any business IT system and regulated digital currencies.

Central bank digital currencies (CBDCs) have largely existed in the virtual realm, with transactions initiated primarily through web and mobile interfaces. However, a significant shift has occurred with the launch of Eurasia’s first CBDC cards in Kazakhstan, providing 20 million consumers with a new, tangible way to manage CBDC funds.

It highlights major trade-offs in security, privacy, and policy that must be addressed before offline CBDC payments can scale. If implemented, offline CBDC capability could introduce new consumer behaviours, shift merchant requirements, and alter the economics of digital payment acceptance. Why is it important? What’s next?

This PoC involved executing real-time cross-border test transactions between various Central Bank Digital Currency (CBDC) systems. The project tested the feasibility of conducting multilateral cross-currency transfers through the UDPN, involving both Distributed Ledger Technology (DLT) and non-DLT-based CBDC technologies.

The agreement brings together OpenPayd’s API-based payment and banking services with Circle’s infrastructure for USDC, a dollar-denominated stablecoin issued by regulated affiliates of Circle. They indicated that the collaboration aims to further expand the use of stablecoins like USDC in practical financial applications.

The growing adoption of stablecoins across Asia marks a significant shift in the regions financial landscape. dollar-pegged stablecoins like USDT and USDC primarily dominate the cryptocurrency topography. Tether (CNHt) Tether CNHt is a stablecoin that is pegged to the offshore Chinese Yuan (CNY). Traditionally, U.S.

Treasury Department is researching usecases for a central bank digital currency (CBDC), as well as drafting regulatory proposals for private stablecoins, U.K. Meanwhile, Lebanon Governor Riad Salameh announced that the country will be introducing a CBDC next year, to “restore confidence,” reported Bloomberg.

The reported move comes as a number of major companies, both within and outside the financial sector, consider entering the stablecoin space in the context of evolving regulatory conditions. These tokens are typically pegged to the US dollar and backed by reserve assets, offering faster settlement and lower transaction fees.

The age of digital currencies might be fully upon us, but key questions swirl about how to issue and regulate cryptos – especially stablecoins. Bitcoin and other offerings have not yet evolved into real alternatives to sovereign monetary activities, but stablecoins present challenges. In a paper that debuted Tuesday (Nov.

The idea that digital assets are exclusively some form of currency has been slowly dispelled, as new usecases emerge and are rapidly adopted across the globe. The digital currency landscape in the MEA region is diverse, with a vast number of companies offering services to meet a variety of usecases and needs.

However, the idea that digital assets are exclusively some form of currency is slowly falling by the wayside as different usecases are emerging and being rapidly adopted. The potential usecases and benefits for users are hazy at best. This may mean that, initially, acceptance of the retail CBDC is gradual.

In addition, the regulator will have jurisdiction over stablecoin issuance, digital banking operations, and cross-border payment solutions. Crypto classified as commodity, not security The legislation classifies cryptocurrencies as commodities rather than securities, thereby excluding payment tokens from being considered investment contracts.

2023 marked a pivotal year in the Asia-Pacific (APAC) region’s approach to crypto regulation, influenced significantly by the preceding implosion of Sam Bankman-Fried’s FTX exchange and the collapse of of Terra, the algorithmic stablecoin created by Korean entrepreneur Do Kwon.

Interestingly, Singapore’s consumer cryptocurrency ownership is high among those surveyed in new findings, and staking has emerged as the most popular usecase, preceding others such as trading cryptocurrencies and holding cryptocurrencies for the long term.

Where you’ll see it: FinovateEurope is sure to be packed with fresh AI usecases and regulatory guidance. Assessing leading usecases, challenges, barriers to adoption and how to navigate the roadblocks.” This session titled, “What is the state of play for GenAI in financial services?

Efforts were also made to advance digital assets, tokenization and central bank digital currency (CBDC) experimentation with initiatives such as Project Guardian and Project Orchid expanding to include more usecases and moving towards “live” pilots.

Each cryptocurrency operates on its own underlying technology and has unique features that may cater to different usecases. What are Stablecoins? Unlike their more volatile counterparts, stablecoins aim to maintain a stable value by pegging their worth to established fiat currencies, commodities, or other assets.

As noted in this space last week, about 80 percent of 66 central banks queried by the Bank of International Settlements (BIS) are working on central bank digital currencies (CBDC). He pointed to the concept of synthetic central bank digital currencies ( CBDC ).

The digital currency and payments market encapsulates various facets, including cryptocurrencies like Bitcoin and Ethereum, central bank digital currencies (CBDCs), stablecoins pegged to real-world assets, digital wallets , and blockchain-based payment networks.

. “Combined, these benefits would substantially improve cross-border payments in particularly underserved corridors, and enable a multitude of sophisticated usecases more generally through native composability or bundling of conditional transactions enabled through tokenisation. BIS Aurum) and interoperability solutions (e.g,

Source: Monetary Authority of Singapore Several nations within the APAC region, including Singapore and Japan , are actively exploring Web3 digital assets and stablecoins. The central bank of Singapore has announced plans to pilot the issuance and use of wholesale central bank digital currencies (CBDCs) in the coming year.

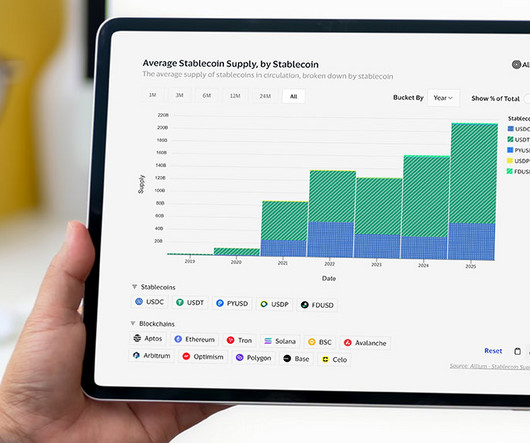

In Asia, stablecoins are gaining significant attention, prompting governments to step in with efforts to regulate the sector. The report, released in April 2025, explores Asias rapidly evolving stablecoin landscape, noting that different countries are taking varied approaches to stablecoin integration.

A survey conducted this year indicates that 85% of senior payment professionals identified fraud detection as the most significant usecase for AI , aligning with the banks’ focus on implementing generative AI for improved fraud detection and securing payment data.

As part of these efforts, Mastercard will join Paxos’ Global Dollar Network and has signalled its intent to integrate PayPal’s PYUSD and Fiserv’s proposed FIUSD stablecoin. The card network already supports Circle’s USDC, currently the second largest stablecoin by market capitalisation.

Immediate focus areas include fraud prevention, ISO 20022 readiness, and stablecoin regulationbut longer-term success depends on active engagement with consultations, operational resilience, and global alignment. Under the forthcoming framework, stablecoinsused for payments will fall squarely under the FCAs regulatory perimeter.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content