This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

TL;DR An ACH API allows businesses to automate bank-to-bank payments—like ACH debits, credits, and recurring payments—by integrating directly with the ACHnetwork via software. What is an ACH API? Where ACH APIs come into play The role of ACH API is to automate your transactions through the ACHnetwork.

Automated Clearing House (ACH) is one type of EFT that processes payments in batches through the ACHNetwork. EFT and ACH offer more security and convenience than cash and checks, but they also come with limitations. Interconnecting 10,000 US banks and credit unions, this network continues to receive high demand.

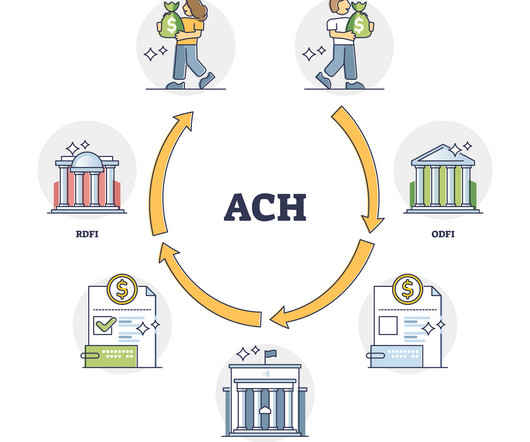

Verification and validation Clearinghouses confirm the authenticity of all parties involved in a transaction through verification and validation. Payment clearinghouses consist of: Automated clearinghouse (ACH): Handles electronic payments such as directdeposits, bill payments, and money transfers.

AVS (Address Verification System) Verifies the billing address matches the card. CVV (Card Verification Value) The 3-digit number on the back of a card. KYC (Know Your Customer) Verification required to open a merchant account. ACH Bank-to-bank transfers, like directdeposit or bill pay.

Prenotes are used for many financial transactions, including directdeposit and payroll, recurring payments, loan repayments, vendor payments, and insurance premiums. While some account verifications require a micro-deposit to verify funds can be transferred appropriately, ACH prenotes use $0 deposits.

ACH stands for Automated Clearing House, a network that handles electronic payments and transfers. So, what is an ACHdeposit? ACHdirectdeposits are common. Understanding the ACHdeposit meaning is important because it’s a fast, secure, and cost-effective way to transfer money.

ACH (Automated Clearing House) payments are electronic fund transfers that use the ACHnetwork to move funds between bank accounts in the United States. This payment method is widely used for directdeposit of payroll, payment of bills, and business-to-business payments.

It's a sophisticated system that many of us have benefited from, whether by using online bill pay or receiving directdeposit paychecks. In this article, we'll explore the ACHnetwork and ACH payments, how ACH payments function, and the ways in which it impacts our daily financial transactions.

ACH payments Another commonly used EFT payment type includes transactions conducted through the ACHnetwork. An ACH credit is commonly used for transactions like receipt of directdeposit payments. U tilize secure network protocols such to protect data during transmission over the internet.

Here are some of the most common: ACH (Automated Clearing House) Transfers Wire Transfers Credit Card/ Debit Card Transactions as EFT Mobile Payments Electronic Checks (eChecks) Point-of-Sale (POS) Payments DirectDeposits Recurring Payments EFT accounts can be checking or savings. Check with your bank for specifics.

Here are some of the most common: ACH (Automated Clearing House) Transfers Wire Transfers Credit Card/ Debit Card Transactions as EFT Mobile Payments Electronic Checks (eChecks) Point-of-Sale (POS) Payments DirectDeposits Recurring Payments EFT accounts can be checking or savings. Check with your bank for specifics.

Here’s a brief overview of the prominent types: Automated Clearing House (ACH): ACH transfers are a reliable and often-used form of EFT. ACH is designed to process batches of transactions, such as directdeposits of salaries or social security benefits and direct payments for bills.

Pay vendors with ACHACH (Automated Clearing House) payments are electronic fund transfers that use the ACHnetwork to move funds between bank accounts in the United States. This payment method is widely used for directdeposit of payroll, payment of bills, and business-to-business payments.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content