This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Understanding ACH credit payments means understanding the way in which different types of ACH payments are processed in the US banking system. ACH credit payments differ from ACH debit payments and both are distinct from credit and debit card payments. Learn More What are ACH Credit Payments?

Thats why 92% of consumers and 82% of companies reportedly made the switch to electronic payments, like Electronic Funds Transfers (EFT) and Automated Clearing House (ACH). EFT and ACH payments are fast, secure, and hassle-free. EFT and ACH offer more security and convenience than cash and checks, but they also come with limitations.

As a business owner, you must have a clear understanding of how online payments processing works to be able to create a hassle-free checkout process that will keep buyers coming back to your eCommerce store. Talk to sales How Online Payment Processing Works On the surface, online credit card processing happens in seconds.

Nonprofit Nacha , which enables Automated Clearing House ( ACH ) payments, has adopted eight new amendments to the Nacha Operating Rules that a press release said will help to modernize the payment style. The amendments concern Same Day ACH and new ways of making ACH payments easier to use, the release stated.

Transaction volume on the EPN ® system, the ACHnetwork operated by The Clearing House Payments Company L.L.C., in 2024, continuing the trend of yearly ACH volume and value growth. In 2024, the EPN system processed 20.7 ACH commercial volume last year. billion transactions worth $56.4

As companies transition to online payment platforms, the complexities of payment processing costs can often lead to unexpected expenses that eat into margins. Thankfully, this article will explore the various payment processing costs associated with Acumatica as well as actionable strategies for businesses to reduce these expenses.

As businesses navigate credit card processing fees, zero cost credit card processing has emerged as a valuable alternative. This option focuses on eliminating processing fees for the merchant by passing them onto customers, a practice thats steadily gaining traction. What are credit card processing fees?

An ACH API integration enables a business or SaaS platform to automate ACH payment processing and reconciliation. Any business that accepts recurring payments should leverage the ACHnetwork for 2 compelling reasons:

NACHA — The Electronic Payments Association — announced that its membership has approved three new rules that will expand Same-Day ACH for all financial institutions and their customers. The expansion of Same-Day ACH will be made possible through the creation of a new Same-Day ACHprocessing window by the two ACHNetwork operators.

New data shows that the ACHNetworkprocessed 21.5 It is the third year in a row in which the number of new ACH transactions increased by more than one billion. And the network’s growth rate for last year is the highest since 2008. And the network’s growth rate for last year is the highest since 2008.

ACH transfers, or payments made through the Automated Clearing House network, account for billions of dollars in payments annually. In fact, NACHA, the nonprofit that governs the ACH payments network reported 6.1% The average consumer commonly uses the ACHnetwork for automated bill payments and larger transactions.

ACH payments are a convenient way for business owners, individuals, and employers to use intuitive automated banking throughout their daily lives. Most small business owners and employers are turning to ACH payments instead paper check payments because of the ease and instant access the ACHnetwork provides.

The backbone of these developments is none other than America’s Automated Clearing House (ACH) which facilitates seamless electronic transactions between banks and financial institutions within its network. Instant ACH transfers have gained prominence as they cater to the increasing demand for expedited financial transactions.

ACHnetwork steward Nacha says Visa has been added to its list of partners for a payment information exchange it is creating to help credentialed service providers share and manage electronic payments information for faster and more secure processing.

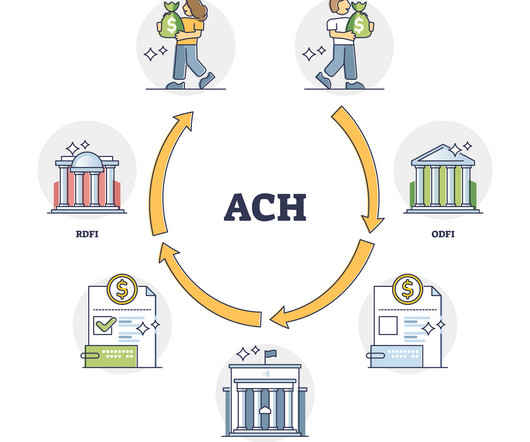

And on that note, two of the most common modes of electronic funds transfer are ACH and wire transfers. In this post, we’re going to review ACH and wire transfers, look at their similarities, and then see how they compare against each other. A typical ACH transaction is like a machine with multiple moving cogs.

Barely a couple of decades ago, there were just a few options available for transferring money from one account to another, but the rise of internet banking has given way to a bunch of different services with different names, processes, fees, and waiting times. Two of the more common methods are known as ACH and EFT transfers.

TL;DR You get to choose from traditional payment methods like cash and checks, online payment methods like digital wallets and ACH transfers, and emerging payment methods like BNPL services and cryptocurrencies. You will need POS terminals to accept and process in-person card payments.

NACHA’s launch of Same Day ACH ushered in three settlement windows, enabling ACH payments to be received same day. The Road To Process Improvement. As Throckmorton pointed out, it’s not about moving money but more about making processes better, more standard and more secure. via all banks and credit unions.

ACH fees may not seem like much, but they can make a big difference for even the most prominent businesses. While ACH transactions are everywhere these days, understanding these fees can still feel like navigating a maze. What is ACH? What are ACHprocessing fees?

Automated Clearing House (ACH) payments are a type of electronic bank-to-bank payment system in the US. Unlike payments facilitated by card networks like Visa or Mastercard, ACH payments are managed by a body called the National Automated Clearing House Association (NACHA). Let’s get started.

The Electronics Payment Association NACHA announced significant increases in the ACHNetwork transactions. billion | Amount of 2016 overall ACH monetary transactions. percent | Percentage increase of ACH transactions from 2015 to 2016. 52 percent | Percentage increase in number of ACH same-day direct deposits.

NACHA, national administrator of the ACHnetwork, said a third processing window for same-day transactions will be postponed for six months until the Federal Reserve Board of Governors (Fed Board) approves the initiative. In the latest example, PayPal Holdings Inc. and The Clearing House as partners.”.

If you’ve been accepting and using electronic payments in your business, you’ve probably come across two of the most popular terms in the digital payments scene— automated clearing house (ACH) and wire transfer. While they’re both electronic modes of payment, they have stark contrasts when it comes to their processes.

Automated Clearing House (ACH) transactions are revolutionizing how businesses and consumers transfer money, offering a variety of payment types to meet diverse needs. Recognizing the different types of ACH payments and their relevant codes is crucial for navigating this complex landscape. What are ACH payments?

What are ACH payments? ACH (Automated Clearing House) payments are electronic fund transfers that use the ACHnetwork to move funds between bank accounts in the United States. The ACHnetwork is managed by NACHA, which was earlier known as the National Automated Clearing House Association.

You’ve probably heard the term “ACH deposit,” but what does it really mean? ACH stands for Automated Clearing House, a network that handles electronic payments and transfers. So, what is an ACH deposit? ACH direct deposits are common. What Is an ACH Deposit? So, what does an ACH deposit mean?

Since its founding in the early 1970s, ACH payments have made payment processes between entities easier. They use direct bank account transfers instead of card networks, checks, or cash. ACH's value lies in its fast payment processing, lower fees, and security.

Payment Network Companies like Visa, Mastercard, Amex, and Discover that move the data between banks. ISO (Independent Sales Organization) A reseller of payment processing services. Assessment Fee A fee charged by the card networks (Visa, Mastercard, etc.). Bank Account Where funds are deposited after processing.

Every day, billions of dollars in transactions are processed around the world. While payment methods vary depending on location, merchant, and type of transaction, ACH payments are one of the most used electronic payment systems in the U.S. What is ACH? Outside of commercial applications, ACH is also heavily used by the U.S.

Data from the ACHNetwork shows growth in payment volumes and values across a number of classifications. More generally, the network reported that the total number of payments was up 5.8 In all of 2018, there were 27 billion ACH payments, with roughly $51 trillion in value that moved across the network.

If your business is using Automated Clearing House (ACH) transactions to pay more of its suppliers, you are not alone. billion B2B transactions were made via ACH in the third quarter of 2023, a 9.6 percent increase from a year earlier, per NACHA, which governs the ACHNetwork.

What is an ACH transfer? ACH (Automated Clearing House) payments are basically EFTs ( electronic fund transfers ) that use the ACHnetwork to move funds between bank accounts in the United States. ACH is most commonly used for direct deposit of payroll, payment of bills, and business-to-business payments.

The firm chose the latter, offering its clients — companies in the hospitality and food services sectors — the ability to pay their suppliers by supporting invoice management and payment processing. According to Moran, one way to approach the conflict is by choosing a strategic payment rail: ACH.

Automated Clearing House (ACH) payments have become increasingly popular among growing businesses, for their faster processing times, lower fees, and reduced risk of fraud. However, managing ACH payments can be a challenging task for AP teams, especially when dealing with multiple vendors and payment preferences.

Same Day ACH will create a new option for faster payments for all the banks and credit unions across the U.S. Two new same-day settlement windows will be added to the ACHNetwork, which will increase the actual movement of funds between all those financial institutions from once a day (at the beginning of the day) to three times a day.

An Automated Clearing House (ACH) transfer limit is the maximum amount of money that can be spent or received through the ACHnetwork in a single transaction or within a specified period. This article will shed light on what ACH transactions are, the nature of their limits, and the influencing factors.

Automated Clearing House ( ACH) transfers have revolutionized the way we handle our finances, offering a convenient and secure method to send and receive money electronically. Whether it’s receiving your paycheck through direct deposit or paying your bills online, ACH payment solutions have become an integral part of our daily lives.

ACH: Key Differences Overview of Nacha Operating Rules Formats for Nacha Payments Importance of Nacha Compliance How Paystand Enhances Nacha Payments The Future of Digital Payments with Nacha Key Takeaways Nacha payments, governed by Nacha Operating Rules, are efficient and secure. What Is an ACH Payment?

ACH: Key Differences Overview of Nacha Operating Rules Formats for Nacha Payments Importance of Nacha Compliance How Paystand Enhances Nacha Payments The Future of Digital Payments with Nacha Key Takeaways Nacha payments, governed by Nacha Operating Rules, are efficient and secure. What Is an ACH Payment?

23 billion: Number of payments the ACHnetworkprocessed in 2018. percent: The growth in payments volume via the ACHnetwork between 2017 and 2018. $40 percent: Projected CAGR of the real-time payments market from 2018 to 2023. 67 percent: Share of Australians slated to use real-time payments by 2023.

George Throckmorton, managing director at NACHA, said the aim was to assess whether standardization would be able to address some particular pain points for users of the ACHNetwork — and offered insight into what’s next. . To demonstrate this challenge, he pointed to the ACHNetwork itself.

Clearinghouses act as neutral third parties that verify, process, and often guarantee transactions to reduce participant risks. Transparency: Clearinghouses provide a clear record of all transactions, offering both parties confidence in the accuracy and fairness of the process.

These can include using a credit or debit card, an electronic check, or an ACH (Automated Clearing House) transfer. Every time you use your card to make a purchase, whether in a store or online, the transaction is processed electronically. But with direct deposits, the entire process can be carried out electronically.

With the current state of economic upheaval, the ongoing pandemic and the great digital shift, corporates and financial institutions are racing to digitize and modernize payment flows and back-end processes. Moving Beyond ACH . Real time and the ACHnetwork can actually work together to displace paper checks.”

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content