This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

SameDayACH is ready for its debut at the end of the week, and for some, its launch signals the next step for the payments industry to become faster and more digital. But a new report finds that, even as SameDayACH is fast-approaching, businesses are actually increasing their use of paper checks.

Thats why 92% of consumers and 82% of companies reportedly made the switch to electronic payments, like Electronic Funds Transfers (EFT) and Automated Clearing House (ACH). Checks can bounce, and cash can get lost. EFT and ACH payments are fast, secure, and hassle-free. No cash or checks needed. In 2024, it processed 1.2

Eliminating checks from corporate payments will take many more years, but Nacha’s latest data suggests the B2B category is playing a key role in SameDayACH's growth.

And pay the very sameday. NACHA, the payments association behind the ACH Network, said Tuesday (Nov. million SameDayACH transactions occurred in October, the first full month after the initial Sept. The total value of those same-day payments came to $4.9 If you build it, they will come.

The backbone of these developments is none other than America’s Automated Clearing House (ACH) which facilitates seamless electronic transactions between banks and financial institutions within its network. Instant ACH transfers have gained prominence as they cater to the increasing demand for expedited financial transactions.

There’s much to look forward to as the September rollout of Phase 2 of SameDayACH (Debit Pull) looms, but David Barnhardt, executive vice president of full-service payment and verification solutions provider GIACT , thinks there’s just as much reason for caution. “I Check and Double-Check.

With Same-DayACH now a reality in the U.S., In its analysis of the Same-DayACH rollout, NACHA found no evidence that it led to an increase in fraud attempts or successful breaches. That doesn’t mean that fraud linked to ACH transactions is nonexistent, however.

—and realize that it’s too late; fraudsters will have figured out how to hijack funds flowing out of checking accounts. Today could be that day. Are banks truly ready for same-dayACH? ACH is a different animal. This exposes banks to fraudsters, who will quickly find and exploit the weakest link.

With the SameDayACH rollout coming in just two weeks and other faster payments initiatives taking off, financial institutions are taking significant steps to ensure the transition to a faster processing environment, including improving their payment security platforms to keep fraudsters at bay. Impact On SameDayACH Rollout.

2 million | Number of SameDayACH transactions made in the first 11 days of SameDayACH’s availability, according to NACHA’s statistics. Those statistics also stated more than 178,000 SameDayACH transactions were made per day, accounting for a total of approximately $1.5

Phase One of the SameDayACH rollout that made credit transfers a reality was completed last year. Phase Two, which will allow debit transactions on the sameday, is planned for September 2017. The third phase, which will usher in faster ACH credit funds availability, is on track to occur in March 2018.

SameDayACH payments are gaining traction right out of the gate, with nearly $5 billion and 3.8 This sets the stage for increased adoption of same-day payments across consumers and the merchants who serve them. The ACH news “definitely has an impact for our business,” said Youakim of the same-day rollout.

There’s another catch, though: While Bill.com facilitates ACH payments, it also announced news that it would support paper check payments made by SMEs by producing and mailing out checks to payees on behalf of SME users. Kriplani said that checks are even more popular among small companies. “If

ACH payments are a convenient way for business owners, individuals, and employers to use intuitive automated banking throughout their daily lives. Most small business owners and employers are turning to ACH payments instead paper check payments because of the ease and instant access the ACH network provides.

While there has been some innovation in wage payment mechanisms as more employers shift away from the paper check toward direct deposit and payroll cards, little has changed about the timing of those payments. ACH Innovation Breaks The Mold. It’s also opened up conversations about how professionals get paid.

NACHA released new statistics late last week on growth of ACH transaction volume in the U.S. According to the firm, B2B transactions were a key driver of ACH transaction growth in the third quarter of the year, leading NACHA Chief Operating Officer Jane Larimer to describe the ACH Network as “thriving.”. In all, more than 3.3

But cash and checks are rapidly declining as preferred modes of payment. If you’ve been accepting and using electronic payments in your business, you’ve probably come across two of the most popular terms in the digital payments scene— automated clearing house (ACH) and wire transfer.

23) marks the launch of SameDayACH, with three settlement windows enabling consumers and businesses to receive credit, sameday, for payments made to them. is now capable of receiving and enabling this same-day capability. But in many ways, today’s milestone is all about what’s next for ACH.

The latest data from Nacha found a new record-high growth rate for adoption of ACH payments , with B2B payments showcasing a surge in adoption of the legacy payment rail that has recently turned to technologies that can augment the service, from the movement of transaction data with an ACH payment to the deployment of SameDayACH.

Checks, despite their near extinction in consumer payments, remain alive and well when it comes to businesses paying each other. The check – for its many, many flaws – does address all three of those aspects. That is why checks have been so resistant to replacement. And that’s pretty well why it persists.

Transaction volume on the EPN ® system, the ACH network operated by The Clearing House Payments Company L.L.C., in 2024, continuing the trend of yearly ACH volume and value growth. ACH commercial volume last year. ACH volume has been growing across all user types and use cases. In 2024, the EPN system processed 20.7

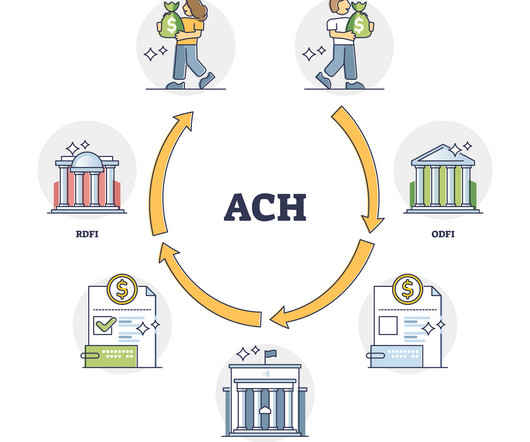

What are ACH payments? ACH (Automated Clearing House) payments are electronic fund transfers that use the ACH network to move funds between bank accounts in the United States. The ACH network is managed by NACHA, which was earlier known as the National Automated Clearing House Association.

An Automated Clearing House (ACH) transfer limit is the maximum amount of money that can be spent or received through the ACH network in a single transaction or within a specified period. This article will shed light on what ACH transactions are, the nature of their limits, and the influencing factors. What is an ACH transfer?

Using FIS-run PayNetExchange to process ACH, checks and virtual cards and using Comdata to issue Mastercard commercial cards, Corcentric pulls in payment capabilities across a range of rails to support the last mile of the B2B transaction. The data makes that glaringly clear. “It’s key when it comes to the payment process.”

The Automated Clearing House (ACH) payment system facilitates the movement of billions of dollars every day, operating behind the scenes in the U.S. In this article, we'll explore the ACH network and ACH payments, how ACH payments function, and the ways in which it impacts our daily financial transactions.

Consumers and microbusinesses have access to many disbursement options, yet they receive a significant share through legacy methods such as paper checks or digital methods that are non-instant.

Data from the ACH Network shows growth in payment volumes and values across a number of classifications. In all of 2018, there were 27 billion ACH payments, with roughly $51 trillion in value that moved across the network. In February 2019, there was a daily record set, when the volume was past 100 million ACH payments per day.

Automated Clearing House (ACH) transactions are revolutionizing how businesses and consumers transfer money, offering a variety of payment types to meet diverse needs. Recognizing the different types of ACH payments and their relevant codes is crucial for navigating this complex landscape. What are ACH payments?

You’ve probably heard the term “ACH deposit,” but what does it really mean? ACH stands for Automated Clearing House, a network that handles electronic payments and transfers. So, what is an ACH deposit? ACH direct deposits are common. What Is an ACH Deposit? So, what does an ACH deposit mean?

Today’s consumers increasingly expect payments to be processed quicker than ever before, and insurance companies are turning to newly introduced faster payment initiatives, such as SameDayACH, to accommodate the demand. Maximizing SameDayACH opportunities.

has reached a real-time tipping point Community Your feed Latest expert opinions Groups Join the Community 23,263 Expert opinions 43,814 Total members 393 New members (last 30 days) 186 New opinions (last 30 days) 29,062 Total comments Join Sign in Why the U.S. Sameday Automated Clearing House (ACH) payments rose 19.1%

To address the supplier acceptance challenge, CardUp automatically shifts bank transfer or check payments to cards, while ensuring that suppliers receive those funds via the original payment method. Nacha Drives Corporate ACH Adoption. Nacha is rolling out a new resource center designed to help corporates embrace the ACH Network.

Automated Clearing House ( ACH) transfers have revolutionized the way we handle our finances, offering a convenient and secure method to send and receive money electronically. Whether it’s receiving your paycheck through direct deposit or paying your bills online, ACH payment solutions have become an integral part of our daily lives.

This week’s examination of the latest in payments rails innovation finds financial service providers innovating on top of existing rails to address the friction of ACH, checks and other bank transfer infrastructure. ACH Gets A Boost In The Public Sector. Invoiced Tackles The Friction of Check.

In the path of FinTech innovation, many expect the inevitable demise of the paper check. But the data doesn’t lie: Paper checks are alive and well, despite efforts to kill it. The latest in PYMNTS’ Kill the Check series , a collaboration with Ingo Money, highlighted the persistence of paper checks.

And pay the very sameday. NACHA, the payments association behind the ACH network, said Tuesday that 3.8 million same-day transactions occurred in October, the first full month after the initial Sept. The total value of those sameday payments came to $4.9 If you build it, they will come.

The payments ecosystem now prizes quickness above all things in a time of cash flow shortages, where each paper check takes an eternity — assuming it arrives at all. Clearly, paper checks aren’t cutting it anymore. To paraphrase the movie “Top Gun” … “We feel the need … the need for speed.” We’ve evolved.

The discussion took place as NACHA unveiled Phase Two of its SameDayACH initiative, debuting same-day debits with an eye on settling bill payments with speed and security. Firms in those industires can look to faster ACH payment options as a cost-effective and customer satisfying alternative to card payments.

Gu said the company typically makes its payouts with ACH transfers instead of relying on checks. Same-dayACH deposits money straight into a customer's account, and funds usually appear the next business day. Around 67 percent of Upstart loans, in addition, are fully automated on the platform.

But while the underlying accounting infrastructure may be embracing technology, the payment itself remains slow, with paper checks still posing a major challenge both to AR professionals’ needs for faster payments and AP professionals’ needs for digitization.

Ach and Wire are two of the most popular ways of money transfer in the United States. First, let's delve into the mechanics of ACH and Wire transfers, followed by an exploration of their distinctions, guidance tailored for small businesses, and concluding with instructions on establishing ACH and Wire processes.

Introduction If you’re still paying your vendors with paper checks, you’re likely facing several issues for your business - like tons of manual effort, difficulty tracking payments, high fees on checks, and so on. Checks are a slow process with many steps on both ends. What are ACH payments?

SameDayACH is now a reality and, with much fanfare, represents the first ubiquitous faster payments initiative in the United States without an attendant regulatory mandate. But as Karen Webster noted in the latest installment of Topic TBD, even as faster payments takes a step closer to reality in the U.S.,

First, there was the Fed’s decision to slow faster payments progress via SameDayACH because it wasn’t ready to approve another processing window during the day. and one of two operators of the ACH network in the U.S., Then came PayPal’s debut of Instant Transfer to Bank. A Couple of Important Dots. Take the Fed.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content