This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The next major shift After November 2025, banks will need to prepare for yet another major shift: structured addresses. Starting November 2026, unstructured postal addresses will no longer be supported in CBPR+ messages. Banks need to adopt either a fully structured or hybrid address format to become compliant.

Despite this immense potential, cross-border payments in LAC remain hampered by inefficiencies in the traditional SWIFT-based correspondent banking system, marked by multiple intermediaries, settlement delays, and fees exceeding 6% for remittances for some corridors. trillion by 2030.

Almond’s blockchain-driven Settlement Optimization Engine (SOE) addresses critical speed, transparency, and cost challenges in cross-border payments. What specific challenges in the cross-border payments industry does Almond FinTech aim to address, and how? Today, moving funds across borders is still incredibly inefficient.

Its expertise is built on experience supporting leading banks and integrating with major payment networks, including Swift and Visa, with Thunes expected to follow soon. What is Project Nexus, and how does it address today’s cross-border payment challenges? Nexus aims to address each of these areas directly.

Fraud prevention features – Look for additional fraud prevention features like fraud detection, address verification, chargeback protection, and IP geolocation to enhance protection from fraud. Even if the data is intercepted, it doesnt offer any value and wouldnt be used to extract the original data.

Fewer correspondent banks to move that money. The Bank for International Settlements (BIS) said in a recent report that the number of correspondent banks — where banks and financial institutions (and domestic payment systems) are linked together — slipped 3 percent in 2019 vs. 2018 and declined a significant 22 percent from 2011 to 2019.

To address this issue effectively, having a reliable source of truth for payment data is indispensable. ” For FIs, the consequences are equally daunting, as they face expenses associated with the correspondent banking network. This necessitates using technology and data solutions to identify and address payment issues promptly.”

SWIFT’s year has been filled with controversy, the apex of which occurred when reports surfaced that cyberthieves infiltrated Bangladesh Bank via the SWIFT messaging system in February, resulting in $81 million stolen from the bank’s account at the New York Federal Reserve.

Mastercard Move Commercial Payments aims to address existing challenges and capitalize on opportunities in commercial cross-border payments in an innovative way. Fully compatible with existing correspondent banking arrangements between respondents and correspondents.

The fraudsters who hacked their way into the Bangladesh central bank two years ago got there by getting into software tied to the SWIFT financial platform. It added later, in description of methodology, Park and peers used North Korean IP addresses to ply their trade. The way they got there? The Background. The Bangladesh Bank Hack.

Mastercard says Move Commercial Payments aims to address existing challenges and capitalise on opportunities in commercial cross-border payments in an innovative way. Tackling serious pain points Mastercard Move Commercial Payments is fully compatible with existing correspondent banking arrangements between respondents and correspondents.

Practical improvements await Rachel Levi, global head of innovation engineering, SWIFT Rachel Levi , global head of innovation engineering, Swift , the cross-border payments provider, notes how the company and ecosystem are working to make practical improvements to international payment speed.

To that end, SWIFT debuted its global payments innovation initiative (gpi) earlier this year, a solution which looks to boost the infrastructure underpinning the movement of money on a global scale. Banks also will be able to immediately stop or recall payments no matter where those payments are in the correspondent banking chain.

Bank Of America Wields SWIFT gpi. Bank of America has built a new solution using SWIFT's gpi rail, which integrates with domestic rails, to enable cross-border payment tracking for its corporate customers. The solution is made possible through the adoption of the funds transfer service Interac eTransfer for Business.

Criticism of the world’s correspondent banking network continues to mount — and at the same time, the number of correspondent banking relationships is on the decline. The Financial Stability Board released analysis last year that found SWIFT interbank payment messages reflected a 4.1

Most international money wires have been possible with the infamous SWIFT code. SWIFT is widely used in almost every country, with just a few exceptions, as it’s one of the most secure methods of sending international payments all over the world. This article discusses the definition and purposes of the SWIFT network system.

Inadequate risk management and due diligence : Institutions faced challenges in ensuring effective customer risk profiling and due diligence, particularly for high-risk clients and correspondent banking relationships. Regular enhancements informed by emerging risks and internal feedback are critical to address systemic vulnerabilities.

It explores the challenges faced by financial institutions in correspondent banking relationships, shedding light on regulatory compliance, security concerns, foreign exchange rate risks, and the impact of fintech players entering the field. The post U.S.

Conduit’s cross-border payment network seamlessly integrates stablecoins, USD and local currencies, providing businesses with a faster, cheaper, and more reliable alternative to the legacy SWIFT system. “What impressed us most was not just their innovative technology, but their remarkable traction and clear product-market fit.

The challenges of global payments are well known, particularly as analysts warn of the impact of a decline in correspondent banking relationships around the world. Analysts pointed to a rise in regulatory pressure as one of the factors pushing banks to reduce exposure to and participation in the correspondent banking space.

Speed, for instance, is an essential component of crypto transactions, making it difficult for many of these businesses to find a banking provider that can address that need. “Crypto is just another payment channel, like SEPA, SWIFT or payment cards,” noted Karalevi? ”

These assessments come in various forms, each designed to address different aspects of business vulnerability. Calculate Overall Risk Level With both the likelihood of each threat and the corresponding vulnerabilities in hand, you can now determine the overall risk level.

These assessments come in various forms, each designed to address different aspects of business vulnerability. Calculate Overall Risk Level With both the likelihood of each threat and the corresponding vulnerabilities in hand, you can now determine the overall risk level.

This is done by ensuring a swift and fair resolution of any issues related to Visa card transactions. Explaining the Allocation & Collaboration Workflows Visa Resolve Online has two workflows for addressing disputes: allocation and collaboration. Collaboration generally addresses mistakes in processing and customer complaints.

In addition to speed, the search engine delivers full visibility into a company’s transactions, providing details such as a payment status, incoming and outgoing messages, Swift GPI tracking details and images. “Within seconds, the tool searches across multiple accounts and applications to find a business transaction.”

The new commercial payments tool leverages a multi-rail system that includes SWIFT, Visa Direct, and Mastercard’s proprietary networks. Move Commercial Payments offers features like liquidity management, integration with existing SWIFT systems, and helps to reduce counterparty risk. with Lloyds Banking Group and UBS.

This resulted in a surge of QR payment-accepting merchants under ACLEDA’s network, from 230,000 in 2022 to over 420,000 in 2024, and the corresponding number of transactions skyrocketed from 16 million to 160 million per year. Partnering with BPC and implementing SmartVista delivered all of these and more.

With correspondent banking relationships on the decline, financial institutions are looking for new — and faster — ways of moving money around the world, too. Some solution providers like Ripple are introducing new ways to bypass the correspondent banking system entirely. This, of course, means faster global payments.

It seems that’s the journey for cross-border payments, which are in the midst of a digital disruption as innovators focus on addressing a range of friction points, from sluggish speeds to high costs. Only a few years ago, small businesses lagged in global payments technology uptake.

China’s renminbi (RMB) is one global currency that is pushing its international standing, but new data from SWIFT released earlier this month found 2017 was a mixed year for the currency. Earlier data from SWIFT released last year found the RMB slipped from fifth place to sixth in a ranking of global currencies. “In

Though common, this strategy fails to present an opportunity to optimize transaction routing throughout the growing number of infrastructures available, whether it be through ACH, SWIFT, Ripple, the correspondent banking network or otherwise.

The reforms aim to address weaknesses in safeguarding practices, reduce consumer fund risks, and enhance regulatory compliance, particularly in preventing fund shortfalls. The FCA has stressed that these reforms are critical to addressing widespread weaknesses in safeguarding practices, which have led to significant consumer harm.

In addition, innovators the world over are exploring how technologies like blockchain could address payments speeds and efficiency on an international level. Financial literacy is also key, while regulatory initiatives to address a decline in correspondent banking relationships — critical to cross-border payments — may also help.

Use an online routing number verification tool: There are several websites that allow you to look up routing numbers to verify their validity and the corresponding financial institution. How do routing numbers differ between SWIFT and IBAN methods? SWIFT codes and IBANS are essential for international payments.

The sender's bank transmits a message through a secure messaging service like SWIFT or Fedwire. NACHA for ACH and government-run rails like FedWire & Swift for Wire. In contrast, wire transfers provide a narrower window for addressing issues related to settlement discrepancies.

Global messaging firm SWIFT is easing some cross-border payment pains by enabling the approximately 11,000 FIs that use its network to send standardized payments information to each other, although much work is needed. Limited connections between FIs can cause delays and higher costs as well.

According to the company, rather than force businesses to rely on expensive third-party payment processors, service providers can help corporates become their own processors for greater cost savings, efficiencies and data integration into their back-office platforms, allowing firms to address ACH’s largest pain points that prevent adoption.

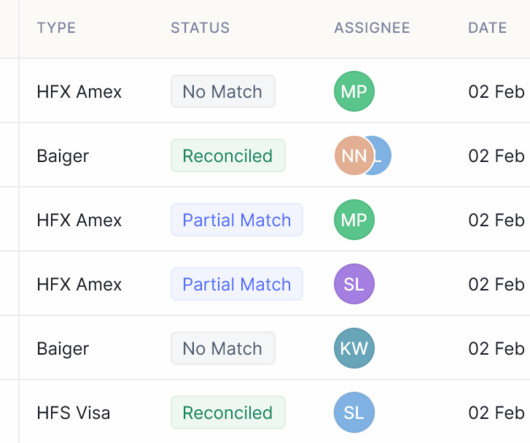

Bank reconciliation typically involves gathering bank statements and transaction records, comparing them with the corresponding entries in the company's accounting records, and investigating any discrepancies. This process ensures the integrity of financial data and confirms that the reported financial position is accurate.

Reconciling payments involves verifying whether the payments received in the company's bank account match the corresponding invoices or payment records in the company's financial system. It ensures that all customer payments are correctly recorded and matched with the corresponding invoices or sales transactions.

Another one, against Banco de Chile in May, cost about $10 million via fraudulent SWIFT wire transfers. Evidence of that comes from Swift’s Latin America Regional Conference , held earlier this month in Miami. She commented that these weak links in the system need to be addressed in order to protect the ecosystem.”.

Real-time Visibility and Tracking: IDP enables swift extraction of relevant information for real-time tracking and monitoring of shipments. The incorporation of address verification mechanisms further fortifies accuracy by eliminating errors stemming from incomplete or inaccurate recipient addresses.

Stripe Reconciliation refers to the use of Stripe for the systematic process of matching and verifying transactions processed through the Stripe payment gateway with corresponding entries in your accounting records. What is Stripe Reconciliation? Division of duties : Errors and fraud can be mitigated by dividing responsibilities.

Fortunately, there are solutions to address these issues – solutions that many people are unaware of. Let’s get to it, addressing the common question, “Why is my Venmo not working” with answers, solutions, and tips to help you troubleshoot and resolve any issues you may be facing. This can lead to swift payment declines.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content