This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Will this be the year that real-time payments — and, especially, peer-to-peer (P2P) — reach critical mass in the United States? He noted that P2P is the first application of real-time payments to gain traction, and said the arrival of that payments functionality is “long overdue.”. Streamlining the Onboarding Process. Building Trust .

The collaboration empowers local licensed institutions and merchants to conduct a wide range of transactions, including B2B, P2P, B2C, and C2B payments. Through this alliance, Thunes and MBANK will facilitate seamless money movement to and from the country.

Circle’s Allaire said in a September PYMNTS interview that electronic currencies are poised to become widely used to conduct business in P2P, C2B and B2B commerce. Cuy Sheffield , head of the crypto at Visa, said this is the first business card that will make the balance of USDC available for spending.

As a result, he predicted that the entrenchment of faster payments will be a linear progression that moves from consumer-to-consumer (C2C) to consumer-to-business (C2B), then to business-to-consumer (B2C) to business-to-business (B2B). So, from the beginning, start with the individual consumer. Particularly in the U.S,

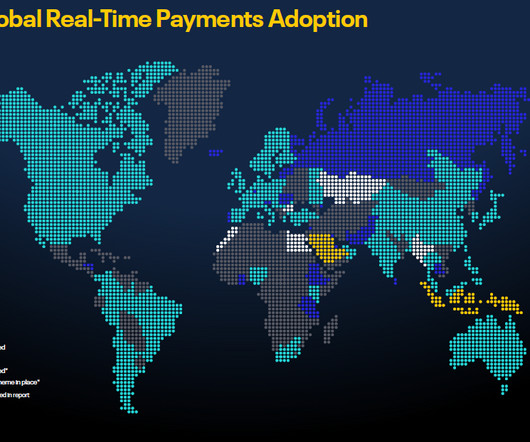

RTP technology facilitates payments across all payment categories, including business-to-business (B2B), business-to-consumer (B2C), consumer-to-business (C2B), peer-to-peer (P2P), government-to-citizen (G2C), and account-to-account (A2A) transactions. Current status of RTP adoptions around the world How RTP is used?

Regardless of whether payments are B2B or C2B, he said the trend has been clear: “You want to be able to choose between which payment instruments you are going to be using at the time of your choosing. These payment apps, said Cole, become “part of the social fabric of how these consumers interact with their friends and their communities.”

In a press release , Avidia said it will soon onboard to real-time payments via The Clearing House, adding to its existing faster payment support that enables P2P and C2B push payments via payment cards. Another institution , Avidia Bank, is also embracing real-time payments in collaboration with FinTechs.

Chipper Cash, a FinTech startup in Africa that facilitates cross-border peer-to-peer (P2P) payment services in Kenya, Rwanda, Tanzania, Nigeria, Uganda and Ghana, has raised $6 million in a seed round led by Deciens Capital, according to a report.

Fiserv comes to the conversation with 30 years of insider industry knowledge, and on the heels of a year in which it moved more than $75 trillion across 30 billion digital payments in peer-to-peer (P2P), consumer-to-business (C2B) and business-to-consumer (B2C) transactions. In other words, it’s seen some stuff. Alphabet Soup.

The company went live in October of 2018, and it’s a no-fee, P2P cross-border startup. The company is also launching a merchant-facing C2B mobile payments app called Chipper Checkout, which will be a paid app. African FinTech payment startup Chipper Cash has attracted some high-profile investors and raised $2.4

In a press release , Avidia said it will soon on-board to real-time payments via The Clearing House , adding to its existing faster payment support that enables P2P and C2B push payments via payment cards.

The reason faster payments is so important, Proto said, is because the four major quadrants of the payments industry — P2P, B2B, B2C and C2B — are all beneficially impacted when it comes to the expedited movement of money and data. When it comes to P2P payments, Proto pointed to a shifting consumer mindset and, in turn, adoption.

Today in PYMNTS’ data, financial services firms are moving electronic money and data, banks have major concerns about data management, multiple zettabytes of information are now produced on a global scale, consumers are more satisfied with features offered by large-format stores than small-format ones and ransomware is crippling small businesses.

Originally, faster payment systems were primarily focused on the retail market [person-to-person (P2P) and person-to-business (P2B)], but increasingly business payments [business-to-person (B2P) and business-to-business (B2B)] are taking advantage of the benefits that faster payments offer,” FIS wrote in its report. Switzerland.

Such was the case in Hong Kong, where the existing RTGS system was only serving high-value interbank transactions, leaving peer-to-peer (P2P) and consumer-to-business (C2B) payments to languish. These payments were typically only processed during work hours, could take days to clear and came with a price tag of up to HK $200 ($25.50

Whether payments are moving between individuals (peer to peer, or P2P) or between consumers and businesses (C2B), they flow most easily from like to like — for instance, if the sender wants to use PayPal, the recipient must also have an account. Interac started out in the P2P space back in 2002.

They’re just a few of the latest developments covered in the Faster Payments Tracker, and there are clear implications for peer-to-peer (P2P) and consumer-to-business (C2B) transactions. But a clear indication of how these developments could impact the B2B payments space remains elusive.

percent), as businesses swap checks for ACH transactions and P2P transactions (up 47 percent) between bank accounts. NACHA reported that in Q4 2018, SDA volume hit 51.3 million transactions, up 46 percent year over year. They also reported notable increases in B2B transactions (up 11.5

These payments offer instant round the clock transfers for B2B (Business-to-Business), B2C (Business-to-Consumer), C2B (Consumer-to-Business), and P2P(Peer-to-Peer). Real-time payments offer a solution to delayed payment options like ACH transactions, credit cards, debit cards, checks, etc. RTP makes it simple to move money.

In the always-on, 24/7/365 economy, payments that circle the globe should conceivably be as simple as those made in a peer-to-peer (P2P) transaction. The transaction wends its way across borders, in the middle of the night, settling instantly. The reality?

RTGS was designed to support high-value, interbank transactions, but P2P and C2B payments typically took a day or two to clear, were processed only during work hours and cost up to HK $200 (US $25.5) per transaction. Hong Kong required a new solution.

According to SWIFT and McKinsey & Company research , B2B cross-border payments accounted for $125 trillion in revenues last year alone, significantly higher than the $54 billion initiated by consumer-to-business (C2B) cross-border payments. percent (compared to 6 percent for peer-to-peer [P2P] payments).

The next-highest category, consumer-to-business (C2B) cross-border payments, paled in comparison at just $54 billion. percent, compared to 6 percent for peer-to-peer (P2P) global transactions. However, B2B global payments revenue margins are the smallest of any category at just 0.1

Both systems provide a simple, convenient way to send money person-to-person (P2P) , allowing users to transfer funds quickly and securely by entering just the recipient’s email address or phone number. Primarily, both services are designed for P2P use, allowing friends, family, and even small businesses to send and receive payments easily.

Early Warning, which bought clearXchange , is expanding its banking network to enable real-time solutions between banks for B2B, B2C, C2B and C2C solutions. P2P is the use case that everyone uses to rationalize the need, yet is the one where the business case is that consumers won’t pay.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content