This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Through this collaboration, Sepagon integrates Genome’s secure incoming payment APIs and real-time webhook notifications to offer faster, more transparent C2Bpayments for businesses and their customers.

The company has enhanced its Banking-as-a-service (BaaS) products by allowing third parties to have access to payment rails. Another institution , Avidia Bank, is also embracing real-timepayments in collaboration with FinTechs.

Avidia Bank is embracing real-timepayments as part of its push to promote collaboration with FinTechs, the financial institution announced Friday (July 12). The APIs in particular enable FinTechs to customize financial services offerings to their corporate partners, the bank said. “We

When The Clearing House (TCH) unveiled the Real-TimePayments (RTP) system in 2017, it propelled swifter payments and brought about the next generation of fund transfers. It wasn’t the first to roll out such a system, but it was the first “major payments upgrade” in the U.S. in approximately four decades. .

Will this be the year that real-timepayments — and, especially, peer-to-peer (P2P) — reach critical mass in the United States? The data points to a confluence of events, as Wilcox told PYMNTS: a readiness on the part of consumers to embrace real-timepayments, and an increasing readiness of FIs to serve them. “I

As a result, he predicted that the entrenchment of faster payments will be a linear progression that moves from consumer-to-consumer (C2C) to consumer-to-business (C2B), then to business-to-consumer (B2C) to business-to-business (B2B). So, from the beginning, start with the individual consumer. Particularly in the U.S,

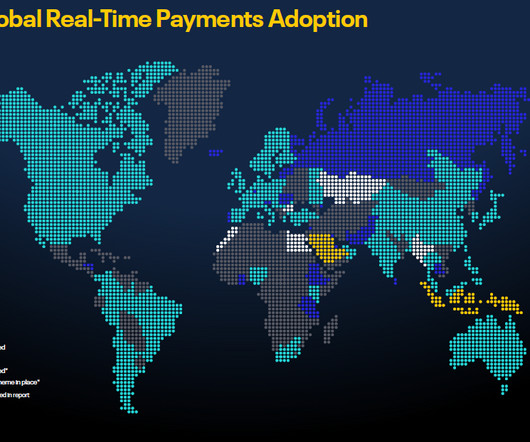

Dozens of countries already have real-timepayments programs in operation, with several more under development, as identified by financial services technology provider FIS in its latest Flavors of Fast report. Those who wait may find themselves left behind as the faster payments revolution takes hold.”.

The collaboration empowers local licensed institutions and merchants to conduct a wide range of transactions, including B2B, P2P, B2C, and C2Bpayments. These services will support diverse cross-border use cases, including foreign education payments, e-commerce transactions, and local acceptance of gig economy payments.

While real-timepayments (RTP) was previously considered an infrastructure luxury, it has now become a common method of payment in many parts of the world. This adoption has changed the payments landscape. Introduction on RTP and its adoption around the world.

With the system joining the existing RTP system, both promising to modernize the way money moves and allow for greater use of instant payments, it seems the shift to real-timepayments is 'inevitable'. Join our panel discussion on the real-timepayments revolution. What are your options?

. Last year, only 25 real-timepayment systems were operational worldwide — that number is growing rapidly. Demand is also heating up for real-time gross settlement (RTGS) systems. SWIFT also recently rolled out a new initiative, one aimed at connecting real-timepayment systems.

Faster and real-timepayments are generally considered a benefit for the consumer payments world. finally making inroads in its faster payments initiatives, it’s now time to see whether faster payments will make their way into the B2B sphere too. But with the U.S. Meanwhile, the U.S.

The March edition of the PYMNTS Faster Payments Tracker TM , powered by NACHA, covers the latest news and developments in the Faster Payments world, including the most recent notable player forays with the blockchain, like IBM ’s recent announcement of Blockchain-as-a-Service. The Power Of Payments.

Realtime, ready for prime time? Adoption of any new payments service does not happen overnight. And when it comes to 24/7 real-timepayments, adoption by businesses, and by consumers, will be pushed ahead use case by use case and transferring funds between accounts in minutes or seconds will gain traction.

Businesses are now digitalizing all aspects of their systems to offer seamless payments on a digital platform. Real-TimePayments. Faster payments benefit both consumers and businesses. Real-timepayments offer a solution to delayed payment options like ACH transactions, credit cards, debit cards, checks, etc.

That faster payments, whether via the Fed or via the TCH’s Real-TimePayments (RTP) network or both, is a big threat to how banks monetize the movement of money between senders and receivers and their depository accounts.

After two decades of tweaking and updating its existing Real-Time Gross Settlement (RTGS) system, Hong Kong determined it needed a new rail. The Hong Kong Monetary Authority (HKMA) designed its long-awaited Faster Payment System (FPS) to ease frictions that RTGS couldn’t. per transaction. Hong Kong required a new solution.

That is the crux of the dilemma playing out on the new real-timepayments rails arena as it relates to the B2B side of the payments ecosystem. That’s where the big payments flow – and where the big opportunities for innovation, change and disruption lie.

According to SWIFT and McKinsey & Company research , B2B cross-border payments accounted for $125 trillion in revenues last year alone, significantly higher than the $54 billion initiated by consumer-to-business (C2B) cross-border payments. percent (compared to 6 percent for peer-to-peer [P2P] payments).

Zelle is a fast, convenient way for people in the United States to send and receive money almost instantly, known as a real-timepayment service (a category of payment methods). Primarily, both services are designed for P2P use, allowing friends, family, and even small businesses to send and receive payments easily.

It’s a wave that was set in motion worldwide a few years ago when regulations in a few countries mandated that consumers and businesses have a right to access funds sent to them in real-time. In other words, it’s a teeny and tiny part of the payments mix in the countries where it was required to happen. Here in the U.S.,

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content