This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The collaboration empowers local licensed institutions and merchants to conduct a wide range of transactions, including B2B, P2P, B2C, and C2B payments. These services will support diverse cross-border usecases, including foreign education payments, e-commerce transactions, and local acceptance of gig economy payments.

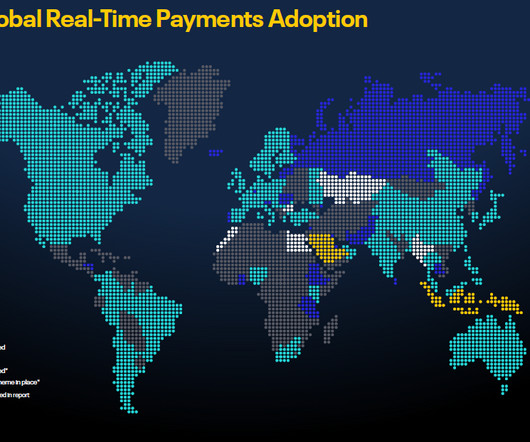

Current status of RTP adoptions around the world How RTP is used? RTP technology facilitates payments across all payment categories, including business-to-business (B2B), business-to-consumer (B2C), consumer-to-business (C2B), peer-to-peer (P2P), government-to-citizen (G2C), and account-to-account (A2A) transactions.

As a result, he predicted that the entrenchment of faster payments will be a linear progression that moves from consumer-to-consumer (C2C) to consumer-to-business (C2B), then to business-to-consumer (B2C) to business-to-business (B2B). Yet, Kresse pointed out that, ultimately, individual consumer behavior drives changes in business behavior.

Speakers: Elizabeth McQuerry, Glenbrook Partners; Mike Sklow, Goldman Sachs; Samson Rajan; JP Morgan; Miriam Sheril, Form3 1:30pm-2:10pmCT: Panel Session – Business End-Users Mega UseCases (City Beautiful Ballroom AB) As more capabilities become available for faster payments, business end users are finding creative ways to use the services.

Think about the fact that the usecase for a restaurant to accept provisions is unchanged,” McCarthy said — even with the pandemic. Such online platforms, he added, can eventually revolutionize B2B payments, and even B2C and C2B transactions. What Happens In A Recession. On The Path To Digitization.

Fiserv comes to the conversation with 30 years of insider industry knowledge, and on the heels of a year in which it moved more than $75 trillion across 30 billion digital payments in peer-to-peer (P2P), consumer-to-business (C2B) and business-to-consumer (B2C) transactions. The usecases for digital payments are also evolving.

RTP adoption has since spread across myriad industries and usescases, ranging from companies paying suppliers, each other and their consumers to government entities making payouts to firms or individuals. Customer-to-business (C2B) bill payments aren’t the only transfers made simpler by RTP.

Card rails are using push payments to close those gaps and support many new usecases for instant money. Both card networks are pushing money over their debit rails and instantly into the bank accounts of consumers and SMBs using their debit card aliases. See First Data and Fiserv. See Visa and Earthport.

Financial institutions need to be actively exploring usecases for real-time payments within their own organizations for meeting the requirement of their customers. This, FIS noted, can be particularly beneficial in B2B usecases. B2B’s Role In Faster Payments.

They’re just a few of the latest developments covered in the Faster Payments Tracker, and there are clear implications for peer-to-peer (P2P) and consumer-to-business (C2B) transactions. The API is a clear vote of confidence on Mastercard’s part that corporates want, and will use, faster payments services.

And when it comes to 24/7 real-time payments, adoption by businesses, and by consumers, will be pushed ahead usecase by usecase and transferring funds between accounts in minutes or seconds will gain traction. It may make sense that the first usecase for Pay on Delivery focuses on alcohol distribution.

Whether payments are moving between individuals (peer to peer, or P2P) or between consumers and businesses (C2B), they flow most easily from like to like — for instance, if the sender wants to use PayPal, the recipient must also have an account. That’s why ubiquity is so desirable. But in an ecosystem like the one in the U.S.,

The payments landscape has evolved over the past few years to embrace other flows across consumer-to-business (C2B), healthcare and business-to-business (B2B) usecases — and open up investment opportunities for those with great tech, but no way to scale it.

Businesses now see the value and competitive opportunities in many C2B, C2C and B2C real-time payments usecases. They are investing in ways to make them happen right now, using the rails available to them. Clearly, those usecases are game-changing – and the ROI is direct and compelling.

The next-highest category, consumer-to-business (C2B) cross-border payments, paled in comparison at just $54 billion. At the same time, though payment solutions are unifying, corporates are expressing demand for solutions that can meet their individual needs based on particular usecases, including corporate trade and investments.

Predictions suggest that Zelle may explore new usecases, such as business-to-business (B2B) and consumer-to-business (C2B) payments, providing a valuable tool for small businesses and contractors who benefit from real-time transactions.

Early Warning, which bought clearXchange , is expanding its banking network to enable real-time solutions between banks for B2B, B2C, C2B and C2C solutions. P2P is the usecase that everyone uses to rationalize the need, yet is the one where the business case is that consumers won’t pay.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content