This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

EMV (Europay, Mastercard, and Visa) chipcard use has continued to expand in use since its tumultuous rollout in 2015. The EMV standard has now become a global standard for cards equipped with computer chips and the technology used to authenticate chip-card transactions.

To improve the payment experience for consumers, card networks must innovate and incorporate the latest technologies. Think AI-powered anti-fraud measures and contactlesspayments such advancements are funded by interchange fees. Card networks typically use a combination of both when setting interchange fees.

Finance shows that contactlesspayments in the country continue to grow. In fact, almost 50 percent of all debit cardpayments are contactless. billion transactions with their debit cards, which is a jump of 8.9 Contactless transactions totaled £7.2 don’t rely on swiping or chipcard readers.

The change happened quickly – numerous markets saw contactless usage go from single digits to more than 50 percent use within 18 to 24 months. It’s not as prevalent in the United States, however, as many cardissuers don’t give customers the contactless option. But there need to be cards in the market to drive adoption.”.

Finance shows that contactlesspayments in the country continue to grow. In fact, almost 50 percent of all debit cardpayments are contactless. billion transactions with their debit cards, which is a jump of 8.9 Contactless transactions totaled £7.2 don’t rely on swiping or chipcard readers.

has been slower to adopt contactlesspayments than other parts of the world, Europe in particular. According to payment gateway NMI, just 3 percent of payments in the U.S. don’t rely on swiping or chipcard readers. cards use chip-and-signature and chip-and-PIN methods. However, the U.S.

The terminal communicates with the cardissuer to approve the payment. Once approved, the funds are transferred to the business’s merchant account, typically within 1–3 business days (same day or next day with Clearly Payments ). Key Statistics Over 83% of in-store transactions are paid using credit or debit cards.

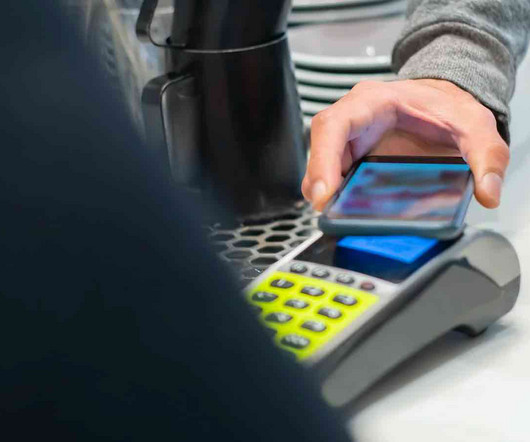

Magnetic stripe payments enjoyed a 30-year reign between the ’70s and ’90s. EMV chipcard technology had a good two decades or so, beginning in the mid-’90s. And the winner of the 2010s and beyond is the NFC-powered, contactless sensation that is tap-to-pay.

To that end, Chase , the largest cardissuer in the U.S., 14) that it’s rolling out tap-to-pay functionality across its Chase Visa card portfolio. A survey of 2,800 consumers found that many individuals have the desire to tap and pay, rather than swipe cards at the point of sale (POS). said Wednesday (Nov.

Traditional cardissuers and networks must adapt or risk obsolescence. Technological disruption and innovation The rapid pace of technological change is both a challenge and an opportunity for the cardpayment industry.

Modern POS systems often come with built-in card readers capable of accepting various payment methods, including EMV chipcards, magnetic stripe cards, and contactlesspayments (NFC). This software needs to be EMV compliant to handle chipcard transactions securely.

Instead, they can tap their mobile devices against supporting POS terminals to process their payments securely and efficiently by way of a digital wallet. Why Is Adding Mobile Payments Important to Businesses Today? What Can You Do to Adopt These Mobile Payments Solutions?

Breakdown of credit card processing fees Credit card processing fees are charged to merchants for each credit card transaction processed. These fees cover handling costs, fraud and bad debt costs, and the risk involved in approving the payment.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content