This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Merchants can end up paying high fees if they have many non-qualified transactions and payment processors may even abruptly change their classification criteria. The first key component is the transaction fee, which is the base cost merchants must pay for each credit card transaction.

EMV (Europay, Mastercard, and Visa) chipcard use has continued to expand in use since its tumultuous rollout in 2015. The EMV standard has now become a global standard for cards equipped with computer chips and the technology used to authenticate chip-card transactions.

The interchange fee usually includes a percentage of the card transaction value and an additional fixed charge. Payment processors usually tack on additional fees on top of interchange to compensate for their services (based on their pricing model ). Card networks typically use a combination of both when setting interchange fees.

This involves using a physical point-of-sale (POS) terminal to process card payments. How It Works The customer swipes, inserts, or taps their card on the POS device. The terminal communicates with the cardissuer to approve the payment. Accepts contactless and EMV chipcards , which are more secure than magnetic stripes.

Amex will also limit the number of counterfeit fraud chargebacks to a total of 10 per card account. Under these new policies, the cardissuer, instead of the merchant, will cover the liability for the additional counterfeit fraud transaction disputed from a card account after those 10 chargebacks.

For a merchant to accept credit cards, they need to pay both credit card processing fees to the banks involved and for the soft and hardware required to process cards. Typically, the merchant’s payment processing software will build the credit card processing rates into their fee. Card Network (e.g.,

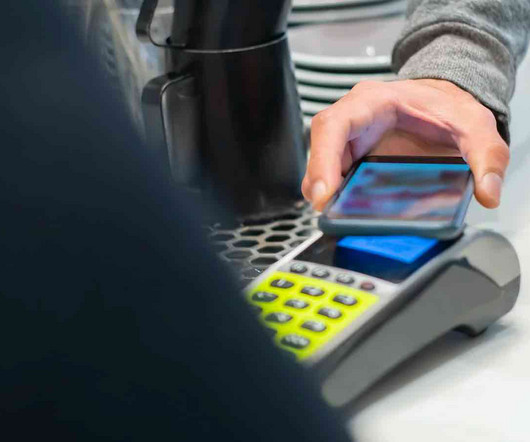

Major cardissuers such as Visa, MasterCard, and American Express each have hundreds of millions of NFC-enabled (near-field communication) debit and credit cards in circulation. Mobile card readers are now supported by major credit cardprocessors such as Visa, MasterCard, and American Express.

Breakdown of credit card processing fees Credit card processing fees are charged to merchants for each credit card transaction processed. Each cardissuer’s interchange rates are publicly available for reference. These fees vary depending on the payment processor and the merchant’s chosen service plan.

Traditional cardissuers and networks must adapt or risk obsolescence. Technological disruption and innovation The rapid pace of technological change is both a challenge and an opportunity for the card payment industry. Thus helping to reduce the overall expense of accepting payments for a merchant.

Since the first plastic credit card was issued by American Express in 1959 , payment tech progress has been growing exponentially. EMV chipcard technology had a good two decades or so, beginning in the mid-’90s. It’s universally compatible Unlike the chipcard and magnetic stripe, NFC technology is standardized.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content