This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

RT2: Renewed real-time gross settlement marks transformation for UK payment providers 9 June 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? RT2, the UK’s new Real Time Gross Settlement service, and its transformative impact on the payments ecosystem. Why is it important?

Tokenisation is now a core enabler of secure, interoperable digital paymentspowering embedded finance, asset tokenisation, and evolving identity flows. Once a system for masking sensitive data, tokenisation has evolved into a foundational technology for enabling secure, interoperable, and scalable digital payments.

Swift drives global interoperability and innovation, aligning with the UK’s National Payments Vision to enhance seamless, secure payments. The UKs payments landscape is at an inflexion point.

As the global demand for faster, more affordable, and increasingly transparent cross-border payments intensifies, Project Nexus is emerging as a foundational initiative to meet the G20’s ambitious roadmap. Eli Shoshani Eli Shoshani is Head of APAC at Bottomline , a leader in global business payments with extensive expertise in the region.

Legacy systems are increasingly unreliable, expensive to maintain, and resistant to modern payment innovations. Integration headaches: Open Banking, APIs, and AI-driven automation often require costly, unreliable workarounds. But as the financial landscape evolves, that mindset is in danger of proving very costly.

Our goal was clear: overcome the fragmentation that plagued international merchants, who had to maintain different payment solutions for each country, leading to operational complexity and significant costs.

As the industry evolves, adopting robust standards like ISO 20022 becomes crucial for driving these benefits. B2B payments service provider Bottomline ‘s on-demand webinar, “Championing Swift Connectivity for Private Banks and Asset Managers in APAC,” explores these critical developments in depth.

The significance of cross-border payments has never been greater. Yet, despite the rise of instant domestic payments, cross-border transactions remain slow, costly, and inefficient. Domestic instant payment systems (IPS), such as Malaysias DuitNow and Singapores PayNow, have revolutionised payments within their respective countries.

The platform risk paradox: Managing digital commerce fraud at scale 12 June 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? A shift toward AI-driven, integrated fraud management systems aligned with tightening UK regulations. Why is it important? What’s next?

New technology and innovations are pushing the payments industry forward, making transactions speedier and safer than they were before. Inside the new Smarter Payments Tracker , PYMNTS explores the latest interoperability developments that are helping banks and FinTechs open up new lines of communication and speak a common language.

Automated Clearing House (ACH) payments are a type of electronic bank-to-bank payment system in the US. Unlike payments facilitated by card networks like Visa or Mastercard, ACH payments are managed by a body called the National Automated Clearing House Association (NACHA). Let’s get started.

Payments messaging company SWIFT said it will test gpi Link, “a gateway to interlink eCommerce and trading platforms with the SWIFT gpi payment service.”. The proof of concept is designed to “bring the benefits of gpi payments’ speed, ubiquity and certainty to distributed ledger technology (DLT)-enabled trade.”

In the intricate landscape of payment processing, merchants encounter a myriad of options, each playing a pivotal role in the facilitation of financial transactions. The Definition of a Payment Processor A payment processor is a financial service provider that facilitates transactions between a seller (merchant) and a customer.

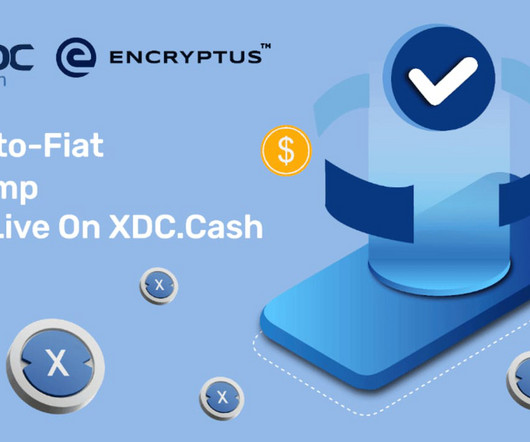

Dubai, UAE, April 10th, 2025, FinanceWire XDC Network continues to strengthen its ecosystem with the launch of XDC.Cash, a Next-Generation Crypto Payment Solution powered by Encryptus. This integration ensures competitive, near-interbank ratesespecially in frontier markets where traditional financial services often fall short.

The payment messaging entity SWIFT this past week began implementing its SWIFTNet Instant service that is tied to the Eurosystem’s TARGET Instant Payment Settlement service. The service, as has been reported, lets customers make instant payments from inside the Single Euro Payments Area (also known as SEPA ).

Merchant-facing regulation: What merchants need to know in 2025 15 May 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? The regulatory framework governing payments continues to expand in scope, with increasing implications for merchants operating in the UK and EU. Why is it important? for credit.

Payments messaging company SWIFT said it will test gpi Link, “a gateway to interlink ecommerce and trading platforms with the SWIFT gpi payment service.”. The proof of concept is designed to “bring the benefits of gpi payments’ speed, ubiquity and certainty to distributed ledger technology (DLT)-enabled trade.”

Examples of popular SaaS apps include Shopify, an eCommerce platform, Dropbox, a cloud storage service, and Stax Bill, an automated payment processing system. These could include platform providers, hardware manufacturers, technology partners, channel partners, and system integrators. Consider Stax’s partner program.

Expanding operations to reach customers like these requires that businesses not only offer appealing products and services, but also provide payment experiences that are both convenient for consumers and easy for the companies to manage. Selling to overseas subscribers means businesses must handle payments in multiple currencies.

And B2B payments , too. In a months-long series of interviews and fireside chats conducted and hosted by PYMNTS, payments executives, investors, bankers and economists weighed in on where we’ve been — and where we must go. Buyers and suppliers don’t really care about the network, but they want to have the payment.

Payments regulation roadmap: Q2 2025 14 April 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is the roadmap about? It provides a structured view of the regulatory developments set to shape the payments sector from Q2 2025 onwardsacross the UK, EU, and international markets. Why is it important? What’s next?

It also extends across industries, enabling seamless integration of financial tools into everyday activities. Open banking also fosters innovation, as fintechs and third-party providers can develop new products and services through secure APIintegrations. Such hyper-connectivity is not limited to financial services.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content