This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Deep Dive Opinion Library Events Press Releases Topics Sign up Search Sign up Search Retail Banking Restaurants Regulations & Policy Risk Technology B2B An article from Mastercard, Visa play down stablecoin threat The giant card networks are sifting through the opportunities and threats that stablecoins present for their businesses.

That’s because it is not only the first stablecoin legislation to gain real bipartisan traction, but it will also serve as a foundation for the US to begin a digital asset ecosystem. Stablecoins gain legitimacy and clarity As a decentralized finance tool, stablecoins have long been grouped together with their crypto cousin bitcoin.

Most of these centre on how firms handle digital assets, particularly stablecoins, as well as the operational and legal adjustment needed to navigate the changing landscape. Stablecoins, as a subset of digital assets, have been a focal point of both the Bill and the FCAs regulatory discussions.

The first two quarters were packed with change: from the stablecoin frenzy and cuts to the CFPB in the US, to new regulatory crackdowns across Europe and the reversal of Section 1033, reshaping the future of open banking. Regulatory clarity is also beginning to transpire.

The enforcement of MiCA provides clear guidelines for the issuance and management of stablecoins, reducing legal uncertainties and fostering confidence among market participants. In response to MiCA’s requirements, several crypto exchanges and service providers adjusted their offerings.

The UK government and the FCA will further develop and implement these regulations through consultations and legalframeworks, aiming for a comprehensive rollout by 2026. With new regulatory frameworks on the horizon, professionals in the sector will face a dynamic environment. What’s next?

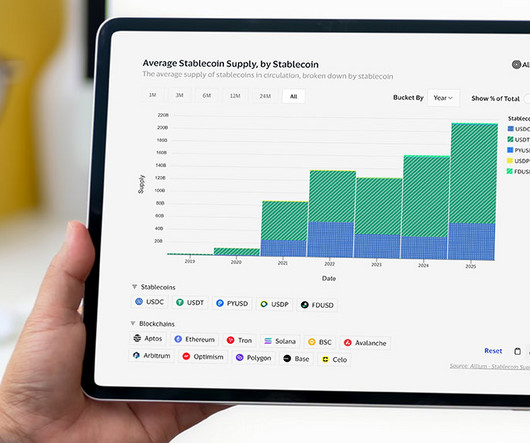

The reported move comes as a number of major companies, both within and outside the financial sector, consider entering the stablecoin space in the context of evolving regulatory conditions. Companies such as Circle and Tether currently dominate the USD 251 billion stablecoin market, but that landscape could shift.

Others on the panel discussed how regulatory and legalframeworks vary globally, posing challenges and risks of regulatory arbitrage. Mike Wilcox, global COO and UK CEO of Blockchain.com highlighted the maturity of digital assets and the growing use cases, including stablecoins and tokenisation.

Financial institutions hesitate to adopt blockchain without clear, consistent regulatory frameworks, especially when operating across multiple jurisdictions. We are starting to see that shift with the introduction of MiCA in Europe, which aims to create a unified legalframework across the EU for crypto-assets.

Under the new legalframework, a wide range of virtual asset-related activities, including cryptocurrency exchanges, token offerings, lending platforms, staking, non-fungible tokens, and decentralised finance services, will require authorisation from CRVAA.

This framework underpins real, verifiable trust. Provide a LegalFramework, Not Software Design The regulation should define the legal environment for trusted digital interactions, not prescribe technical implementations.

In many ways, this setup is akin to stablecoins (where a company holds USD in a bank and issues tokens like USDC or USDT). They offer the speed and openness of crypto markets but are still tethered to the legal and financial realities of traditional markets. As we move forward, keep an eye on trust and transparency.

Etherfuse has undertaken extensive regulatory efforts in Mexico and aims to use this unique legalframework to establish itself as a leading global platform for compliant tokenized assets. The company has launched five products so far, including short-term notes from Mexico and Brazil.

No matter how disruptive a fintech platform is, it must operate within legalframeworks that are evolving rapidly. Crypto and Digital Assets : Governments are rapidly building frameworks for digital asset custody, trading, and issuance. It is no longer enough to innovate.

The Consultation Paper comes shortly after the Financial Services and the Treasury Bureau and the HKMA issued a consultation paper in December 2023 outlining their legislative proposal for a regulatory regime governing stablecoin issuers in Hong Kong (see this Latham blog post ). reference assets). reference assets).

For stablecoins, concept is edging closer to reality, especially for digital dollars – with a dose of regulatory clarity. To that end, as Jeremy Allaire , CEO of Circle , told PYMNTS’ Karen Webster, a number of trends are converging to bring stablecoins into the mainstream of commercial and consumer payments.

De Meijer Owner and Economist MIFSA Location Maarrssen Followers 8 Opinions 157 Follow Unfollow Stablecoins are attracting considerable attention by traditional financial institutions. Regulatory shifts are paving the way for banks to engage with stablecoins. What are stablecoins? How stablecoins work?

In Asia, stablecoins are gaining significant attention, prompting governments to step in with efforts to regulate the sector. The report, released in April 2025, explores Asias rapidly evolving stablecoin landscape, noting that different countries are taking varied approaches to stablecoin integration.

While digital infrastructure is advancing, including cloud-native solutions and distributed ledger technologies (DLT), legalframeworks are still rooted in outdated assumptions, creating friction in what should be frictionless systems. But as Paul Palmer pointed out, safety in real-time payments isnt just a legal question.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content