This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Navigating AML obligations in the age of virtual IBANs February 10 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? The compliance challenges of virtual IBANs, focusing on AML obligations and regulatory gaps. Why is it important? What’s next?

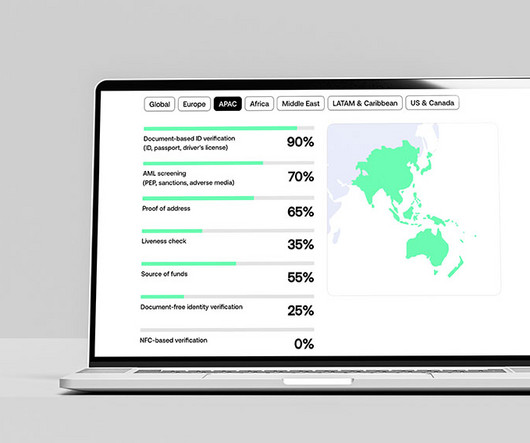

The research shows that banks in Singapore are dedicating more time and resources to KYC processes, which are vital for anti-money laundering (AML) compliance, than any other region surveyed. However, traditional banks in Singapore have been slow to adopt innovative technologies like cloud computing and AI, despite regulatory encouragement.

Cryptocurrency fraud is declining in Asia-Pacific (APAC), driven by advanced technology adoption and stricter regulatory oversight. According to the 2024 Sumsub crypto survey, countries that have implemented this technology are seeing an average improvement of 3.6% in 2023 to 2% in 2024. in verification times.

And in PYMNTS’ own coverage, the twin external forces of regulatory scrutiny and market pressures are pushing FIs to retool and strengthen their anti-money laundering (AML) efforts. Much of those revamped efforts come, perhaps not surprisingly, through advanced technologies. But AI is still relatively rare in the banking world: Only 5.5

Businesses must proactively assess fraud risks, implement adequate procedures, leverage technology for fraud detection, and foster a culture of compliance to avoid regulatory penalties. Duediligence : Ensuring employees and third parties adhere to anti-fraud policies. What’s next?

It also enables businesses to streamline risk management and ensures they meet stringent customer duediligence requirements under anti-money laundering ( AML ) regulations. ” Applicable at any business level As a global solution, it is tailored to meet the unique needs and maturity-levels of different markets.

By integrating with DVS, Sumsub ensures compliance with local anti-money laundering (AML) and Know Your Customer (KYC) regulations while reducing fraud and streamlining onboarding through automation. This solution offers real-time, government-backed validation of identity documents, including passports, driving licences, and visas.

The framework is designed to ensure compliance with international standards, particularly in relation to anti-money laundering (AML) and countering the financing of terrorism (CFT). Additionally, the proposed regulatory framework includes guidelines on technology risk management and cybersecurity.

Ensure regulatory compliance by adhering to anti-money laundering (AML) laws and Know Your Customer (KYC) requirements. Step 4: KYC and AML Checks Compliance officers or automated systems integrated with KYC and AML verification services verify the identity of business owners and ensure compliance with anti-money laundering regulations.

Financial crimes risk management software company Quantifind and Oracle Financial Services have teamed up to improve anti-money laundering (AML) compliance and to add intelligence and automation properties directly into the compliance workflows, according to a release. “We are excited to announce our collaboration with Oracle today.

However, PSPs must ensure their systems and processes support this capability, which may involve implementing blockchain analytics tools and strengthening compliance with anti-money laundering (AML) and counter-terrorist financing (CTF) regulations. Read More

FIs have made strides in establishing know your customer (KYC) and anti money laundering (AML) policies, but these changes are routinely challenged by emerging technology and cross-border transaction costs. A DIY Approach To AML/KYC. One of the problems that AML/KYC procedures face is lack of standardization.

Sumsub’s platform will enable banks to streamline user onboarding, perform anti-money laundering (AML) screenings, verify business clients, and monitor transactions for fraud with the option to adopt and manage all features through a single platform. We are pleased to partner with Sumsub, following a rigorous duediligence process.

The acquisition will provide APPC clients with a broader range of tools to fight challenges ranging from anti-money laundering (AML) to counter-terrorism financing (CTF). This collaboration has yielded flexible, customized solutions to help FIs deal with challenges ranging from anti-money laundering (AML) to counter-terrorist financing (CTF).

From EDD and eKYC to AML to CDD, we’re going to cover everything you need to know about KYC in this article. it’s the opposite: customer duediligence is an ongoing process that is a part of the KYC requirements, which in turn is part of the broader anti-money laundering (AML) regulations set in place for financial institutions.

Inadequate risk management and duediligence : Institutions faced challenges in ensuring effective customer risk profiling and duediligence, particularly for high-risk clients and correspondent banking relationships.

By combining advanced AML analytics in scoring processes and robotics in alert and case handling you tremendously improve efficiency and effectiveness in compliance. In our experience these technologies can increase the number of SARs by 20% while at the same time producing efficiency gains of 30% in alert investigation and case management.

But flipping through the latest edition of the PYMNTS AML/KYC Tracker, in collaboration with Trulioo , there is a lot of data to suggest that this is the situation in an awful lot of organizations. Which means the marketplace needs to evolve different when it comes to technology partnerships.

The US, therefore, requires financial institutions as well as financial services firms to have anti-money laundering (or AML) compliance programs in place. In this article, we’ll discuss everything you need to know about ensuring AML compliance as a payment facilitator (or PayFac). Let’s get started.

Anti-money laundering (AML) is a good example. Here are two examples of technology FICO has developed, and for which we’ve made patent applications: Machine learning (ML) for improved AML monitoring. We’re using variants of technology proven effective in other FICO products such as FICO® Falcon Fraud Manager.

In this blog, we will explore the importance of digital identity verification, the technologies involved and the challenges it faces. Therefore, businesses, governments, and other organizations often rely on regulatory technologies (Regtech) to ensure that identities are verified quickly, accurately, and securely. The “2024 U.S.

Key regulatory areas include customer onboarding, data protection, anti-money laundering (AML), and transaction monitoring. This includes duediligence, auditing, and shared responsibilities with financial institutions. A security lapse, system outage, or compliance failure can destroy a platforms credibility overnight.

Increasing anti-money laundering (AML) regulations further add complexity. Regulators only require ‘duediligence,’ but the definition of what constitutes adequate duediligence can vary.” “Regulators only require ‘duediligence,’ but the definition of what constitutes adequate duediligence can vary.”

Technology can help banks make better decisions regarding de-risking: To treat customers as individuals it is vital that proper Know Your Customer (KYC) and Client DueDiligence (CDD) happens. The FCA has indicated that AML measures in themselves are not a reason to suspend or deny accounts.

According to a report in ZDNet , Westpac said that “a mix of technology and human error” and “deficient financial crime processes” were behind the financial institution’s (FI’s) lack of compliance with anti-money laundering (AML) regulations. Australian bank Westpac Banking Corp. may stand as Exhibit A here. Crime, At Scale.

The 2018 FATF mutual evaluation report of UK anti money laundering (AML) practices highlights a problem that to many is still surprising – when you set up a business in the UK, very little is done to establish the identity of the owners of that business, whether those are individuals or other businesses.

The HKMA concluded that the bank failed to continuously monitor business relationships, conduct enhanced duediligence in high-risk situations for a period, and maintain proper records for some customers. This includes robust regulatory frameworks, advanced technological solutions, and enhanced global cooperation.

The scene is now set for the UK to adopt a digital identity scheme underpinned by the government-backed Digital Identity and Attributes Trust Framework (DIATF) and Open Banking’s real-time technology infrastructure for exchanging personal data with customer consent. This bank-centric form of digital identity already exists in the UK.

In my Financial Crimes Predictions 2021: More AI & Ransomware post , I talked about how banks will move to operationalize their Anti-Money Laundering (AML) compliance programs to achieve greater efficiencies and how robotic process automation (RPA) adoption will drive the paradigm shift. Collect data from internal and external sources.

Anti-money laundering (AML) initiatives involve laws, regulations and procedures aimed at preventing criminals from masking illegally obtained funds as legitimate income. Since the global financial crisis, AML fines totaled $56 billion, with US-based financial institutions incurring $5 billion in fines for related infractions in 2022.

Over the past years, financial crime tech has risen to prominence, driven by increasing complexity and frequency of financial crimes, stricter regulations and compliance requirements, and technological advancements. The study, which surveyed nearly 50,000 people from 43 countries, found that 25.5%

Cohen likened The Floor’s approach to building an “app store” of digital technologies that can be deployed as banks can improve their internal tech stacks with a range of new integrations. Can you imagine Google, Apple or … Amazon taking a year and a half, or even more to implement a new technology?” Cohen asked. It’s unthinkable.”.

These regulations create a comprehensive global framework, but enforcement remains inconsistent, and many institutions struggle to keep pace with data quality and technological demands. million for persistent failures in AML controls, including deficiencies in correspondent banking duediligence and transaction monitoring.

Compliance and risk management technology provider Opus is launching a new Know Your Customer (KYC) workflow solution for banks. The Software-as-a-Service (SaaS) tool also looks to streamline client onboarding and improve the accuracy of customer duediligence. A press release on Tuesday (Jan. ”

Fenergo has released their annual financial fines analysis, showcasing that penalties for failing to comply with anti-money laundering (AML), KYC, environmental, social, and governance (ESG), sanctions and customer duediligence (CDD) regulations totalled $6.6billion in 2023, up considerably from $4.2billion in 2022 and $5.4billion in 2021.

As technology advances, the threat to digital security and identity protection becomes greater, forcing regulations to quickly adapt. Madhu explained that there are two segments of KYC — customer duediligence and enhanced duediligence. But in a space that’s constantly changing, how can anyone really keep up?

The platform’s capabilities—ranging from ID Verification, Liveness and Face Match, to PoA and Ongoing AML Monitoring—were instrumental in transforming dtcpay’s operational landscape. This flexibility, alongside advanced features and constant AML monitoring has been central to dtcpay’s efforts to streamline its operations.

So the idea that the money laundering directive in Europe would mandate beneficial ownership as a part of enhanced customer duediligence “is, in some ways, the logical next step,” Gaddy said. Forex companies, in particular, move money as they change it from different currency types.

Uniting fraud protection and prevention with AML checks and compliance allows for better collaboration across the historically siloed operations of teams dealing with distinct but related crimes – fraud and financial crimes, terrorist financing or other nefarious intentions.

The partnership will strengthen compliance automation with real-time enhanced due-diligence (EDD) analytics and transactional decision making based on IdentityMind’s Trusted Digital Identities, Neoway’s data and their combined data analytics capabilities.

In yesterday’s post, my colleague TJ Horan introduced the topic of artificial intelligence being applied to anti-money laundering (AML). Based on the categorization, the right level of duediligence is being applied, with riskier customers getting more duediligence. But it’s still too high.

Intelligent compliance technology company Napier has teamed up with client lifecycle management platform KYC Portal. Intelligent compliance technology company Napier and client lifecycle management platform KYC Portal have announced a new partnership. KYC Portal made its most recent Finovate appearance at FinovateEurope in 2019.

KYT is an anti-money laundering (AML) and counter-terrorist financing (CTF) requirement. As an AML and CTF operation, Know Your Transaction complements the process of Know Your Customer (KYC) by focusing on which transactions people are making, as opposed to just who is making them. Ask an Expert What Does KYT Mean for AML Compliance?

The technology automatically contacts customers whose checks have been flagged as suspicious, and provides a user-friendly digital inquiry process to help customers resolve issues in seconds. Refine Intelligence has introduced its Digital Customer Outreach for Check Fraud Prevention solution.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content