This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

With an initial launch date set for September 2025, experienced firms in the region are joining forces to help ensure the real-timepayments platform is successful. Antonio Soares, CEO, Dock One organisation helping in this preparation phase is Dock , the banking and digital payments provider in Brazil and Pix participant.

Guavapay’s flagship products, MyGuava (B2C) and MyGuava Business (B2B) payment apps offer users to open accounts in over 20 currencies, including GBP, USD, and EUR. With these accounts, users can send local and international real-timepayments at competitive fees.

This agreement brings expanded access to global, fast, and secure payment options for CARD.com’s customers, aligning with its mission to deliver innovative financial solutions for its B2C and B2B White Label customers.

New payment rails are once again in the spotlight as real-timepayments and cryptocurrency emerge as the top focuses for innovators. In this week’s look at payment rails innovation, the European Union begins paving the way for greater crypto adoption, while Mastercard expands its own crypto accelerator initiative.

Real-timepayments aren’t just an opportunity for consumers to send and receive money more quickly. Interest in faster payments is also on the rise for corporates, though their adoption of real-timepayments won’t look the same as it does in the B2C world. Uncovering The B2B Use Cases.

Banking payments platform provider linked2pay wants to help financial institutions implement real-timepayments capabilities. 15) that banks using its Bank Centric Payments platform will now have access to real-timepayments thanks to a collaboration with Push Payments.

Everlink Payment Services is teaming with workflow solutions provider FINTAINIUM to offer B2B and B2Cpayments in realtime, leveraging the ISO 20022 global standard, according to a press release.

Today in B2B, Bloomberg broadens its credit risk data pool, and two ERP solutions secure B2Bpayments integrations. Plus, Everlink strikes a partnership for real-timeB2Bpayments. Everlink, FINTAINIUM Team Up To Offer Real-TimeB2B, B2CPayments. 2) announcement.

While B2Bpayments innovation often takes a page or two out of the business-to-customer (B2C) payments world, the rise of the gig economy and freelance professionals have challenged the payments space to develop solutions that can appear to be a hybrid of corporate and consumer solutions.

The B2Bpayments ecosystem experienced a sudden and dramatic acceleration of change upon the onset of the global pandemic, and its impacts reach far beyond the mere digitization of the B2B transaction. The Coexistence Of Rails. Often, that means the cooperation of multiple rails at once.

Bolstering growth through collaborations Guavapay’s flagship products, MyGuava (B2C) and MyGuava Business (B2B) payment apps enable users to open accounts in over 20 currencies, including GBP, USD, and EUR. With these accounts, users can send local and international real-timepayments at competitive fees.

During the 2020s, almost all businesses will have been looking at b2bpayments processing solutions to meet changing consumer needs. Online and contactless adoption multiplied, and digital payments rose. consumers using two or more types of digital payment methods increased by 8%. Learn More What are B2BPayments?

If we’re talking about business-to-business (B2B) payments, the speed of business is nothing to brag about. The outmoded B2Bpayments landscape stands in stark contrast to the business-to-consumer (B2C) and peer-to-peer (P2P) spaces where instant money and real-timepayments are becoming the norm.

Visa Canada plans to offer real-timeB2B and B2C disbursements via its Visa Direct card-to-card transfer service, competing head-on with Canada's Interac network and a product Mastercard launched in the country earlier this year.

. “By enabling their fast, secure, digital payment solutions, Xodus Travel Services will offer policyholders an improved claims experience with payment optionality and realtimepayment options.” ” Transcard said that it plans to go live with more Canadian bank connections later this year.

It may have taken some time, but faster and real-timepayments demand continues to grow in the corporate and B2Bpayments context. This week's look at payment rail innovation is all about speed, both for legacy rails and new ones. SWIFT to Launch New Real-Time Rails.

For B2B, it seems, the advent of the open API cannot come fast enough. The back and forth between businesses, whether centered on payments or data, is mired in paper, phone calls and faxes — in short, wasted time and resources. New applications should streamline those inefficiencies. In the U.S., Easier said than done.

Is it prime time for realtime, especially for B2B? The rise of Zelle , and any number of peer-to-peer (P2P) payment options, has increasingly brought consumers on board with the need for speed in payments — where settlement is marked by seconds and minutes, not hours or days. Where We Stand In The US.

In the first service offered by Mastercard after integrating Vocalink last year, and with an eye on real-timepayments, Mastercard Send is launching in the United Kingdom. based bank accounts and receive payments by the same means.

As a result, he predicted that the entrenchment of faster payments will be a linear progression that moves from consumer-to-consumer (C2C) to consumer-to-business (C2B), then to business-to-consumer (B2C) to business-to-business (B2B). So, from the beginning, start with the individual consumer. Particularly in the U.S,

They can eliminate the pain points in business-to-consumer (B2C) transactions by keeping consumers from waiting to receive their funds, while businesses are witnessing the advantages of using real-timepayments when transacting with each other. Around The Real-TimePayments World. About The Tracker.

In this week's roundup of payment rail innovation, PYMNTS finds B2Bpayments use cases serve as an important driver of adoption, with FinTechs and financial service providers embracing payment rails old and new to enable real-timeB2Bpayments and foreign exchange. OpenPayd Debuts Real-Time FX.

The collaboration empowers local licensed institutions and merchants to conduct a wide range of transactions, including B2B, P2P, B2C, and C2B payments. These services will support diverse cross-border use cases, including foreign education payments, e-commerce transactions, and local acceptance of gig economy payments.

With the B2B eCommerce market towering over B2C’s in terms of transaction value — Forrester Research estimates the U.S. trillion by 2021 — the business-to-business payments market is primed for disruption. The payment rail and technology options for B2B eCommerce platforms are vast, and continue to grow.

It seems an especially low number when considering this stat: Only 3 percent of companies meet customer demands for instant business-to-consumer (B2C) payments. As much as 80 percent of firms still rely on paper checks when it comes to making business-to-business (B2B) payments. Why B2B Lags.

Whether through virtual payment technologies or faster payment initiatives, the B2Bpayments ecosystem has explored ways to accelerate the time it takes a buyer to pay its supplier. Some argue electronic payments, like credit cards, are the answer. What Doesn’t Work.

It was only (relatively) recently that B2Bpayments finally secured significant attention and investment from innovators. A notoriously clumsy, friction-filled industry, B2B transactions must forge new paths to boost efficiency as businesses demand global solutions, speed and transparency.

Accounts payable (AP) automation technology has hit the ground running, with solutions designed to accelerate invoice processing, optimize payment strategies and promote digital adoption. That’s not to say that small- to medium-sized business (SMB) invoice payment challenges are any easier to overcome. Conflict Of Interest.

2024 is expected to be a year of innovation for the fintech industry, marked by advancements in artificial intelligence (AI), cross-border and real-timepayments, cryptocurrency and blockchain, and bundled software-as-a-service (SaaS) offerings.

The expansion of traditionally consumer-focused FinTechs widening their solution scope to include B2Bpayments tools exemplifies just how massive the opportunity is for service providers to tackle friction. Around the world, B2B transfers are expected to reach a $218 trillion valuation in the next three years alone.

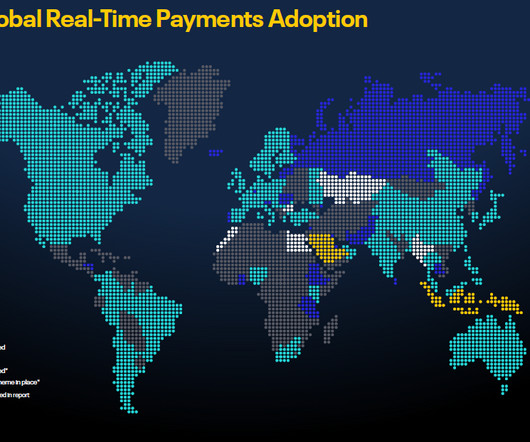

While real-timepayments (RTP) was previously considered an infrastructure luxury, it has now become a common method of payment in many parts of the world. This adoption has changed the payments landscape. Introduction on RTP and its adoption around the world.

Western Union CEO Hikmet Ersek told Karen Webster that realtime means that receivers will have funds available to spend within minutes, enabling new real-time, cross-border, cross-currency payments capabilities for C2C, B2C and B2B use cases. “We Changing The Landscape And Overcoming The Challenges

As real-timepayments (RTP) gain traction with consumers via peer-to-peer (P2P), the pump may be primed for business-to-business (B2B) transactions to follow suit. One hurdle is decidedly not with the real-time infrastructure that’s in place. Although conventional wisdom may hold that the U.S.

billion Nium is a global payments platform that makes cross-border money transfers easier for businesses and financial institutions. Using real-timepayment technology, Nium helps companies speed up international transactions, simplify operations, and scale. Nium Valuation: $1.4 Coda Valuation: $2.5 CGTZ Valuation: $2.41

One of them is NCR , and with its new Innovation Lab , the company is looking at how omnichannel eCommerce and payments can make transacting simplified. Andy Brown, NCR’s marketing director of payments, says IoT and other emerging technologies are critical to this initiative, especially in B2B commerce and payments.

To gain a deep understanding of the current landscape and future outlook, Rapyd conducted a global research study surveying more than 1,000 business owners and payment decision-makers from a variety of high-opportunity industries, across ten key markets: Brazil, Canada, France, Germany, Italy, the Netherlands, Spain, Singapore, the UK and the US.

If the pandemic has taught banks anything, it’s that corporates need to offer a range of payment methods to their customers — whether those customers are consumers (for B2C transactions) or enterprises ( B2B ). The value lies in offering payments anywhere, anytime, across a range of B2C and increasingly B2B use cases.

In the future, all B2Bpayments will be digital. It’s no secret that B2B, as an industry, has lagged behind B2C by leagues when it comes to going paperless. ” During the live discussion they provide insight on the evolution of B2B will discuss what comes next, over the near term and longer term. .”

.” With that in mind, the Federal Reserve’s Secure Payments Task Force has developed various work streams on which its members can focus, with payments security in the context of faster and real-timepayments a key theme.

But the speed of payments for B2B solutions still has a long way to go, with many paper checks still circulating at sluggish speeds, and high percentages of businesses requiring numerous different sign-offs before money reaches where it’s going.

While there’s been much hype surrounding venture capitalists’ growing attention on B2B FinTech, this year has largely been lackluster for the industry. This week, however, B2B startups enjoyed a solid moment of funding, as familiar names like Tipalti were joined by newcomers like Zervant to address an array of business finance needs.

The pandemic has shone a light on some glaring inefficiencies in B2Bpayments. B2Bpayments have none of those hallmarks, Gupta noted. Now the question is: How do the financial institutions and the banks provide the same quality of service, which is provided today in B2C, to their B2B customers?”

To better understand what and who is involved in these transactions, this article will dive into common business-to-business (B2B) terminology and payment methods. What are B2Bpayments? These payments occur for various reasons, including purchasing raw materials, settling invoices, and procuring services.

“I think one of the largest reasons [insurers are still using checks] is because claim payments, the paying out of a claim, is [a] loss of money, and it is really hard for companies to focus or invest resources in a place in which you are losing money already,” Michele Schmitt, senior product manager for B2B insurance technology firm Tr?v

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content