This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

23) that they have entered a strategic partnership to launch Visa Commercial Pay, billed as a suite of B2B payment solutions for enterprises making the shift to digital transactions, and, specifically, virtual cards — and away from paper-based manual processes. She said 89 percent of B2B buyers are making more online purchases than last year.

The B2B payments ecosystem experienced a sudden and dramatic acceleration of change upon the onset of the global pandemic, and its impacts reach far beyond the mere digitization of the B2B transaction. How that is achieved is a matter of innovation and experimentation. The Coexistence Of Rails.

There are a multitude of benefits that open banking brings to B2B payments. The following Deep Dive explores open banking initiatives around the world, how APIs can harness open banking to facilitate B2B payments and how APIs can reduce the prevalence of outdated and insecure data-sharing methods. Both the U.K.

In B2B payments, the path to making transactions as seamless and invisible as possible is often about closing the gap that separates buyer and supplier. While a growing population of B2B FinTech solutions has helped to connect B2B buyers and sellers, more platforms can create more friction on either end of the equation.

From a lack of supplier acceptance of electronic payments to outdated infrastructure within accounts payable (AP) departments, the B2B payments ecosystem still has much room for improvement on multiple fronts. Moving the needle in the journey away from paper checks isn’t a one-sided battle, either. An Ecosystem Approach.

Citi’s Treasury and Trade Solutions is bringing its accounts receivable (AR) Payer ID solution to more markets around the globe. 6) that Payer ID is now available in 44 countries, as Citi brings the B2B payments tool across North America and Western Europe. The financial institution (FI) announced news on Monday (Nov.

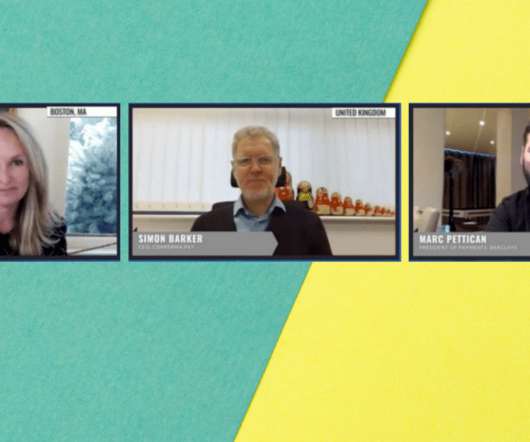

Historically, corporate travel and expense ( T&E ) management has been viewed as an entirely separate function from other B2B payment workflows. As a result, the lines that once separated T&E from other B2B payment workflows are blurring, according to Conferma Pay CEO Simon Barker and Barclays President of Payments Marc Pettican.

Today In B2B, U.K. challenger bank Tide runs dry of SMB loan funds, while Payer launches an ID verification service for B2B eCommerce platforms. Plus, Just Cashflow collaborates with Railsbank, and HashCash streamlines its B2B payments offering. Payer Financial Debuts New ID Verification Service.

With B2B payments being an increasingly attractive target for innovators, the landscape is growing crowded as more banks and FinTechs roll out their accounts payable (AP) automation solutions. “I think everybody recognizes that B2B payments are an enormous opportunity in the U.S. The competition is undoubtedly heating up.

Bank of America’s latest offering, for example, addresses payment acceptance challenges, while Bill.com marries accounts receivable (AR) and AP with tools that tackle friction in processes that touch both ends of the B2B payments journey. Bank introduced a new eBilling tool also designed both for billers and payers. Finally, U.S.

National Institutional Facilitation Technologies (NIFT) has announced a partnership with B2B FinTech Haball for a new contextual railroad to help boost B2B payments in Pakistan, according to a press release. Based on the ISO 20022 framework, the CFT will provide detail on transactions, the press release stated.

During the 2020s, almost all businesses will have been looking at b2b payments processing solutions to meet changing consumer needs. But what about in the business-to-business (B2B) sector? Industry data shows that the B2B payments landscape is rather diverse. Learn More What are B2B Payments? Not sure where to start?

With speed being the most obvious value proposition of real-time payments capabilities, it’s not difficult to imagine that corporate payers would be eager to embrace faster payments functionality in their accounts payable (AP) departments. And for many firms, that’s exactly what they’re beginning to do.

Today in B2B payments, TripActions announces new funding that values the T&E startup at $5 billion, while OneSource Virtual launches invoice payment capabilities. Plus, iBanFirst launches B2B payment traceability tool, Georges rebrands with new funding, and HashCash partners with a bank on blockchain payments. 21) blog post.

Though credit cards were not originally designed to address the needs of corporate payers, advances in commercial card technology have positioned the payment tool as one that’s gaining traction in the accounts payable department. This, he noted, is Mesh’s entryway to the market of cross-border B2B payments.

For years, any attention given to solving B2B payments friction was typically focused on the payer. Pain points experienced by B2B vendors when collecting cash will inevitably seep into their own AP processes. Furthermore, the challenges faced by suppliers when collecting payments can mean additional friction for their payers.

It marks a significant advancement in account-to-account payment solutions, offering businesses a fully integrated payment experience with the Worldline brand at the forefront to build trust towards payers. Additionally, it offers cross-border capabilities that are essential for merchants operating in multiple markets.

When it comes to strengthening the B2B payment proposition, oftentimes, tackling friction for only one side of a transaction is no longer sufficient. For the payer, this means interest-free cash flow for up to 55 days, the company said in its announcement. Tat Capital Eases Card Acceptance For Vendors.

In a separate statement, Argo CEO Luigi Botto pointed to the benefits virtual cards can have for corporate payers. “With WEX payment solutions and Argo, our clients will have better control over their cash flow and will gain operational agility by automating payments and reconciliation of travel expense,” the executive said.

Paystand, the only feeless B2B blockchain-enabled payment platform, today brings its automated payment solution to Acumatica, an all-in-one cloud-based ERP system for business management that includes finance, inventory, CRM, and payroll. The Acumatica Paystand integration is available for Acumatica users as of January 31, 2024.

While optimizing back-office functions like accounts payable and accounts receivable can support enhanced cash-flow management, B2B partnership collaboration is also critical to supporting the financial health of an organization. AscendantFX Eases Payment Instruction Hurdles. ”

The solution is compatible with existing Citi accounts receivable solutions, including Citi Payer ID Accounts for automated reconciliation. Users can view transaction activity and manage online banking entitlements, the bank explained.

The firm revealed the rollout of its commercial payment solution, TSYS Virtual Payment Precept (VPP), a virtual payment tool for accounts payable and accounts receivable to streamline reconciliation and heighten risk controls in the B2B payments space, the company said.

With the B2B eCommerce market towering over B2C’s in terms of transaction value — Forrester Research estimates the U.S. But the reconciliation, security, payment terms and buyer-supplier relationship do not mean one size fits all for B2B transactions initiated on an eCommerce platform. They want to combine them.”

At the same time, due to manual reconciliation, these healthcare providers also lack visibility into the claim payment status, putting even more strain on their billing teams. Integrating Mastercard’s innovative virtual card platform, which makes complex B2B payments fast, easy and secure, holds promise for the healthcare industry.

Within the B2B space, especially, technology can improve payments processes that are time-consuming and error-prone. All too often, he said, bringing automated payments processes and reconciliation, as well as improved cash collections, are not viewed as offering significant enough returns on investment.

In B2B payments, corporates’ continued use of paper checks confounds FinTech firms working to give businesses more affordable, faster and more efficient payment options. Yet, for many business payers, the reason for using checks can be quite straightforward: It’s simply the way payments have always been made.

As Biegel explained, a lack of data standardization across payment tools remains a challenge to the reconciliation and cash application process, even when that data is electronic. The B2B arena certainly continues to see a high prevalence of paper checks in the U.S. Lockbox Data Headaches. Automating Lockbox Data – And Beyond.

Unlike traditional B2B areas, where the supplier and customer have agreed upon pricing, and it is the exception when the payment amount does not equal the billed amount, “ he told PYMNTS, “it is standard practice in healthcare for a provider to bill one amount only to have the payer decide to pay a completely different amount.”.

To better understand what and who is involved in these transactions, this article will dive into common business-to-business (B2B) terminology and payment methods. What are B2B payments? A reliable B2B payment system plays a pivotal role in the smooth operation of businesses across industries. How do B2B payments work?

Even when technologies come close to addressing multiple challenges that exist today when sending, receiving and reconciling B2B payments, those benefits typically come with a cost — whether it be the interchange fees of cards or the burden of replacing legacy infrastructure.

In B2B payments, it’s not just the movement of money that’s a pain point for companies — it’s the tracking of that payment and the ability to reconcile those transactions that can be a major headache for both payers and payees. In an announcement on Tuesday (Oct. In an announcement on Tuesday (Oct.

That includes corporates, too, as firms like PayPal press into the B2B payments and small business finance market – but they’re not always doing it alone. Working with PayPal, the company said, could ease friction for both payers and payees in the B2B payment process, encouraging firms to pay their vendors more quickly.

The competition is heating up between payment technologies in accounts payable, with ACH and virtual cards seeing significant pushes in the B2B payments space to combat the dreaded paper check. For many businesses, which payment tool is best depends on many factors, from what their vendors prefer to payers’ own cash positions.

With so much paper stuck in AR and AP departments, the B2B payment functions are prime digitization targets that could yield efficiencies and cost savings well after economic disruption settles. “The ultimate B2B payment is really a virtual card,” he said. That PDF is probably still going to be printed out at some point.”

Before the pandemic, concern was growing over the issue of late B2B payments and the struggle among small businesses to get paid on time. For small business clients, she said, the growing preference is to use credit cards over direct bank transfers, often due to the ability for cards to provide extra capital float for the payer.

B2B payments friction isn’t only experienced on the payer side. These hurdles can also stifle electronic payments adoption in the B2B arena. Having access to key data surrounding a transaction is critical for both sides’ reconciliation processes, he added, which is where the collaboration with Paymode-X comes in.

Adoption of commercial cards in B2B payments has emerged as one of the hottest industry topics of the year thanks to new FinTech innovations and industry leaders like Visa and Mastercard making a push further into the market. percent of incoming payments volume for B2B vendors by 2020 — up just 1.5 percent from 2017 volume.

The partnership will allow WEX to connect its corporate customers to Billtrust’s B2B payments services, which addresses friction for both corporate payers and the suppliers accepting payments. “We’re pleased to partner with Billtrust to solve for the ‘last mile’ of automated settlement and reconciliation.

This creates an interesting predicament for B2B payments disruptors: Should technology be used to make paper checks less friction-filled, or should it be used to entice businesses away from the paper check altogether? Card payments, meanwhile, are also subject to fraud as payers often email or phone in card details.

As payments giants like Visa and Mastercard shift the innovation spotlight onto B2B transactions, developers of new accounts payable solutions are ushering in a growing trend: designing payment tools not just for the payer, but for the B2B supplier as well. Discover Targets Reconciliation Data.

With newer digital, automated payment technologies emerging in the B2B space, businesses continue to stick to what’s familiar: paper. The process added friction not only to payment processes, said Cooley, but also in terms of reconciliation and the ability to access payment data. Speaking The Same (Payments) Language.

In many ways, the rise of crypto and digital currencies like Bitcoin aims to address some of these issues, empowering payers and payees with a way of bypassing the “middleman” of the inter-banking system for faster transaction speeds. Choice, he said, is key to guiding corporates toward a digital currency ecosystem.

percent of survey respondents reporting that they are “very” or “extremely” satisfied with paper checks, it seems like B2Bpayers really don’t find them to be all that bad. Yes, checks were nearly bottom-of-the-barrel in terms of satisfaction levels, but with 63.5 Keeping the Supplier In Mind.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content