This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

EuroPA solutions are rooted in domestic infrastructures, with varying technological approaches. It accelerates the adoption of A2A payments across all transaction types: P2P, B2C, C2B, B2B WHAT ABOUT THE DIGITAL EURO? Wero enables instant, account-to-account (A2A) payments without relying on traditional card networks.

Genome , a leading European Electronic Money Institution (EMI) regulated by the Bank of Lithuania, and Sepagon , an open banking technology provider specializing in seamless, card-free payments, are pleased to announce a partnership that enhances the efficiency of transactions.

The collaboration empowers local licensed institutions and merchants to conduct a wide range of transactions, including B2B, P2P, B2C, and C2B payments. It will help to provide new technologies that will simplify the lives of our customers and strengthen MBANK’s position as one of the leaders in Kyrgyzstan.”

India-based Airpay raised new venture capital for its combination of C2B and B2B payment solutions. Airpay said it will use the funds to continue building out its technology and focus on sales, distribution and support infrastructure. Reports Tuesday (March 21) said Airpay raised $3.6

Seamless omnichannel experience is valued by shoppers of any age, notes Forbes Technology Council. OpenWay , a payment technology provider, has collected insights from omnichannel players that use its Way4 acquiring software platform – Nexi, Shift4, Halyk Bank, SmartPay, Banesco, Equity Bank Kenya, and others.

If you look across the technology industry and the payments industry, the pace and movement of change is accelerating,” Mike Kresse, division executive for card and money movement at FIS , recently told PYMNTS in an interview. Processors, including FIS, he said, can act as the technology department of their FI clients.

Cross River, a company that provides banking services for technology companies, will join The Clearing House’s (TCH) RTP network, according to a release. By joining the network, Cross River will be able to give its clients the ability to send, settle and clear payments instantly, along with messaging capabilities, while ensuring compliance.

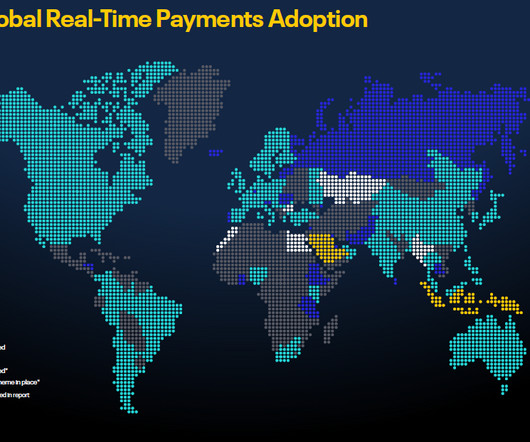

RTP technology facilitates payments across all payment categories, including business-to-business (B2B), business-to-consumer (B2C), consumer-to-business (C2B), peer-to-peer (P2P), government-to-citizen (G2C), and account-to-account (A2A) transactions. Current status of RTP adoptions around the world How RTP is used?

. “DadeSystems has developed a uniquely simplified process for managing account receivables by leveraging advanced data management and machine learning technologies,” said Tom Richardson, managing director for Wells Fargo Strategic Capital. and holds over 180 portfolio investments.

It’s not as much of a one-on-one relationship that you would see from a C2B perspective. Technologies like APIs and QR codes can be useful tools to achieve this, creating yet another area in which corporate treasurers can provide strategic guidance. The B2B eCommerce evolution is also facing pressure from a shift in buyer behavior. “The

an FI must invest in technology that can support and maintain such efforts at scale. And in looking toward the evolution of real-time payments, he said it’s likely the movement will be from P2P to consumer-to-business (C2B) — especially in paying small businesses such as lawn care companies or car repair shops.

Fiserv comes to the conversation with 30 years of insider industry knowledge, and on the heels of a year in which it moved more than $75 trillion across 30 billion digital payments in peer-to-peer (P2P), consumer-to-business (C2B) and business-to-consumer (B2C) transactions. In other words, it’s seen some stuff. Alphabet Soup.

” While he highlighted the continent’s “cutting edge” mobile payment technology ecosystem, one country is not the same as the next in terms of mobile payments usage, either. . “There’s not only a variety of banks to deal with when sending payments back-and-forth but also different regulatory regimes.”

Clearly, the investments and interest in blockchain technology are real, but will it ultimately be the technology used as the foundation for the financial industry’s real-time payments solution? The Power Of Payments. That’s revolutionary,” he said.

Today in PYMNTS’ data, financial services firms are moving electronic money and data, banks have major concerns about data management, multiple zettabytes of information are now produced on a global scale, consumers are more satisfied with features offered by large-format stores than small-format ones and ransomware is crippling small businesses.

Such was the case in Hong Kong, where the existing RTGS system was only serving high-value interbank transactions, leaving peer-to-peer (P2P) and consumer-to-business (C2B) payments to languish. These payments were typically only processed during work hours, could take days to clear and came with a price tag of up to HK $200 ($25.50

It’s a world where technology and commerce intertwine, creating a seamless web of online merchants and eCommerce platforms that cater to your every need. Consumer-to-Business (C2B) C2B eCommerce reverses the traditional buyer-seller relationship. Not exactly. But what is an online merchant, and what is eCommerce?

Technology, improvements in logistics and, of course, new innovations in payments have all played a role in bringing trade to an ever-broadening global stage. Technology, increasingly, is enabling the current model of cross-border trade,” said Agarwal. Macro Trends as Tailwinds. Only 20 years ago, eCommerce was an unheard-of notion.

They’re just a few of the latest developments covered in the Faster Payments Tracker, and there are clear implications for peer-to-peer (P2P) and consumer-to-business (C2B) transactions. Again, it’s an indication that financial services players are confident faster payment technologies will see demand from corporates.

Technology is rapidly evolving, and the world of payments isn’t left behind. These payments offer instant round the clock transfers for B2B (Business-to-Business), B2C (Business-to-Consumer), C2B (Consumer-to-Business), and P2P(Peer-to-Peer). The payment ecosystem has been significantly influenced by technological advancement.

Financial institutions are witnessing technological change in digital payments, coupled with higher customer expectations for faster payments. C2B) to better capture the benefits of digital and mobile transacting, and how it's beginning to happen in the U.S., The Clearing House has gained momentum with its RTP service.

Bose said there are significant changes taking place amid Citi’s corporate clientele, which include a shift from purely business to business flows to business to consumer (B2C) and consumer to business (C2B) flows.

Dozens of countries already have real-time payments programs in operation, with several more under development, as identified by financial services technology provider FIS in its latest Flavors of Fast report. In the three years since FIS began this annual report, the number of real-time payments programs more than doubled, researchers noted.

As Founder Masayoshi Son has said, the goal may be to build a company that can grow 300 years down the road, banking on game-changing technologies, such as artificial intelligence. There is money to be made with these enablers, who are, at their core, technology businesses.”. As a result, last month, the company reported a $6.5

Don’t miss your chance to see all of these companies, and more, demo their technology live. DAVO Technologies’ automated technology solution solves small-to-mid-sized merchants’ sales tax pain points. Today, we’re revealing the first group of companies that will take the stage at the event.

“Without collaboration between banks, [FinTech firms] and technology providers, it will be hardly possible to create a seamless experience [that] our clients are asking for,” he said. What’s more, Tutsch noted, the end user shouldn’t be able to notice the complexities of all these collaborations and integrations.

Its survey took a look at how individual consumers are interacting with these technologies as individuals, and eventually corporates, make use of “futuristic” payments technologies. We break down the highlights of the survey below. 21% of consumers expect bitcoin to become a viable currency within the next decade.

The next-highest category, consumer-to-business (C2B) cross-border payments, paled in comparison at just $54 billion. Combined with the growing sophistication of online trade, supply chain finance platforms and logistics technologies, large corporate cross-border payments are playing an increasingly prominent role in business operations.

The COVID-19 pandemic’s impacts are already being felt across various business sectors, and efforts to reduce its spread are sending ripple effects through supply chains and shifting B2B and consumer-to-business (C2B) payment practices.

Switching has to create enough value to invest in the people, processes and technology to make the move. Businesses now see the value and competitive opportunities in many C2B, C2C and B2C real-time payments use cases. For innovation to ignite, stakeholders must find enough value to switch.

Technology and the Internet of Things mantra is exciting, exhilarating and in many ways, an innovator’s dream. Early Warning, which bought clearXchange , is expanding its banking network to enable real-time solutions between banks for B2B, B2C, C2B and C2C solutions. Or is it just a new source of friction?

Predictions suggest that Zelle may explore new use cases, such as business-to-business (B2B) and consumer-to-business (C2B) payments, providing a valuable tool for small businesses and contractors who benefit from real-time transactions.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content