This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Home Credit , a global non-bank consumer lender, has successfully reduced its creditrisk while maintaining loan volumes and keeping approval rates steady by incorporating the FICO® Score X Data to optimize its loan process in China. They are one of our most sophisticated clients in terms of advanced analytics.”.

16) said Lendingkart will offer its creditriskassessment technology to banks and other alt-lenders starting in 2017. “We plan to offer our analytics technology to other NBFCs [non-banking financial companies] and financial institutions sometime in 2017,” the executive said in an interview with Livemint.

The FCA’s final guidance, issued in April 2025, outlines “reasonable procedures,” including fraud riskassessments, internal controls, staff training, and governance oversight. Next steps/action required: Conduct a comprehensive fraud riskassessment across all channels and partners.

PayFacs handle riskassessment, underwriting, settling of funds, compliance, and chargebacks which exposes them to greater potential risks. Major risk factors for PayFacs include fraudulent transactions, merchant creditrisk, regulatory compliance, and operational risks.

(Photo by Christine Roy on Unsplash ) This is reflected in reports from major banks like Wells Fargo and JPMorgan Chase, which have not observed companies making large withdrawals from credit lines—a sharp contrast to the early days of the Covid-19 crisis, when businesses rushed to secure cash.

Traditional underwriting processes may not assess creditworthiness accurately for a borrower who derives income from non-traditional sources. Filtering customers based on income and savings, in addition to credit scores, can be a stronger predictor of mortgage risk. Verify KYC/AML based on geography.

Morgan’s financial strength and Slope’s innovative approach to creditriskassessment and monitoring. All of these features are powered by our AI-driven underwriting and risk-scoring infrastructure, which is built in-house from the ground up. The partnership brings together J.P. By combining J.P.

Securitization plays a key role in driving increased liquidity in the mortgage market, ensuring that banks can fund more loans, at lower cost. FICO Scores, of course, play an important role in the risk management and transparency that powers the secondary market. This in turn gives consumers greater access to affordable mortgages.

This capability not only enhances operational efficiency but also empowers non-technical users to contribute effectively. A low-code platform with drag-and-drop functionality allows digital lenders to quickly develop, customize, and deploy applications without extensive coding expertise, significantly speeding up the loan origination process.

A partnership aimed at helping banks, payment providers and fintechs meet the ever stronger regulatory demands while reducing effort and expense. . We serve corporates, insurance companies, and banks – be it a retail, private, wealth management, automotive or telecom bank, tier 1 or tier 3 bank. What do you do?

Credit unions are different and they inherently think of themselves that way – as part of a microcosm, somewhat separate from the broader financial services industry. But the reality is that credit unions are still competing for customers in the same market as big banks and FinTechs. Let’s consider the competition.

Gold Loan Management System Gold loan management system streamlines the management of gold-backed loans, helping lenders enhance efficiency, ensure compliance, and optimize riskassessment. Core Capabilities of Finflux by M2P Advanced Appraiser Module : Ensures precise gold valuation with reliable and accurate assessments.

We also wanted to know what to expect from the Netherlands-based, cloud-banking software specialist in the second half of 2015. Michiel Schipper: During our first appearance, we showcased a solution where medium-sized enterprises could build their own financing solution from the bank’s assortment.

Creditrisk analytics provider Carrington Labs teamed up with real-time decisioning infrastructure company Oscilar. The partnership will make Carrington Labs’ explainable AI-powered, advanced creditrisk and cash flow underwriting models available via Oscilar’s decisioning platform.

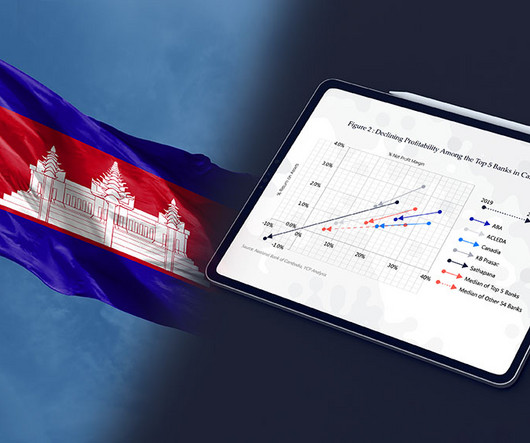

Cambodia’s banking sector, traditionally known for its rapid growth and dynamic transformation, is facing a significant decline in profitability, with banks in the country experiencing a decline in return on asset (ROA) and net profit margin (NPM), a new paper by YCP and Confluences says. and NPM from 26.6% and NPM from 27.2%

These institutions offer more than just microloans; they also provide savings accounts, insurance products, and other financial services designed for low-income individuals and micro-entrepreneurs who otherwise lack access to basic banking. Irregular RiskAssessment Inaccurate income assessments lead to poor credit profiling.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content