This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

FXC Intelligence, a data platform specializing in the cross-border payment and e-commerce sectors, has released its annual selection of the world’s most promising cross-border payments companies in 2024. Another company from Singapore featured on the list is Tazapay. It claims more than 20,000 business customers.

FXC Intelligence, a data platform specializing in the cross-border payment and e-commerce sectors, has released its annual Cross-Border Payments 100 list, highlighting the 100 most influential players in global payments. Released on May 08, the 2025 Cross-Border Payments 100 recognizes industry leaders across the sector.

EPI is the bank-led organisation responsible for building Wero , a unified mobile payments service for Europe. “The aim is to cover all use cases (person-to-person and commercial payments both online and in-store) across the markets of the participating solutions.”

America Biometric Payments 2 Global, especially mobile-first markets Cash Payments 5 Emerging Markets, some developed regions Central Bank Digital Currencies (CBDCs) 1 Asia, Caribbean Credit Cards Overview : Credit cards allow consumers to make purchases on credit, paying later and often with interest.

A new report by Deloitte delves into the latest developments in the cross-border payment sector in Asia-Pacific (APAC), identifying four major trends reshaping the landscape and offering significant opportunities for merchants. Public-private collaborations also play a critical role in developing and promoting cross-border payments.

James Hurren explores what early CBDC deployments across Asia, the Caribbean, and Europe reveal about usage, adoption, and the future of cross-border digital money. Central bank digital currencies (CBDCs) have rapidly evolved from theoretical concepts into live pilots and national deployments.

Traditional banks often view SMEs as high-risk due to limited credit history and collateral. Despite their significant contributions to GDP and employment, SMEs in emerging markets remain underserved by traditional banking. Traditional banks typically require extensive documentation, credit history, and collateral, which many lack.

Making cross-border payments simple Liv, the UAE’s first and largest digital bank launched by Emirates NBD, is introducing a new way to flex, letting people access multiple currency accounts from a single card. The Flexible Credential gives consumers more choice and control over their finances.

For online shopping, Visa passkeys replace passwords or one-time codes. Click to Pay – Enables consumers to complete online transactions within a few clicks, powering a more seamless and secure checkout experience at scale. to broaden its merchant coverage network across Japan. .”

With mobile wallet adoption expected to reach 63% in 2025 and the prepaid card and e-wallet market projected to grow, the country stands as a digital payments leader in Southeast Asia. From bank-backed apps to fintech-led super apps, the market is being shaped by innovation, integration, and rising user expectations.

From digital payments to decentralised finance (DeFi), these companies are solving real-world challenges like financial inclusion and cross-border transactions, while setting new global standards for innovation. billion digital asset, Web3 WeLab 1 billion digital banking, lending Micro Connect 1.7 Nium Valuation: $1.4

The report notes how stablecoins, supported by regulatory developments, are driving advancements in digital commerce and cross-border transactions. The report also notes a shift in consumer preferences, with rising adoption of digital wallets, mobile POS payments, and BNPL services.

This ambition, however, hinges on the capability to execute seamless cross-border transactions — a theme extensively explored in Mastercard’s Borderless Payments Report 2023. However, this shift towards global integration is not without its challenges.

FXC Intelligence, a data platform specializing in the cross-border payment and e-commerce sectors, has released its annual selection of the world’s top cross-border payment companies, recognizing the leading publicly traded companies, startups and private companies operating in the space worldwide.

Datapro , a leading provider of core banking systems and digital solutions, recently collaborated with Mastercard to expand the integration of Mastercard Cross-Border Services, a solution within the Mastercard Move portfolio of money transfer solutions.

While online payments have taken off, many consumers still favour credit cards or cash for offline purchases. Digital wallets are especially popular for online shopping, paying bills, and mobile transactions. Digital wallets are especially popular for online shopping, paying bills, and mobile transactions.

While transaction fees and fraud prevention dominate immediate merchant concerns, forward-thinking businesses are leveraging payment method diversity, cross-border capabilities, and emerging technologies to gain measurable advantages. Recent market data shows this demand is reaching a tipping point across Europe.

The European Union’s leading bank, BNP Paribas and Ant International , a digital payment and financial technology leader, have formed a strategic partnership to enhance cross-border payment solutions for merchants and consumers in Europe.

Alipay+ , Ant International’s cross-bordermobile payment and digitalization solution, revealed three trends shaping the future of tourism to the benefit of global merchants and the industry. By using Alipay+, cross-border travelers can experience a new country or market and pay like a local.

They include: the merchant, cardholder, card associations, acquiring bank, issuing bank, and payment processor. These are not banks, but rather governing bodies that set interchange rates, and arbitrate between acquiring and issuing banks. Acquiring Bank: The business’ (i.e., merchant’s) bank.

In a press release , the companies said Interac is using Mastercard Send, a push-payments service to send money cross-border, on the Interac eTransfer platform. That will enable customers to send money from Canada to bank accounts in Europe. Citing the World Bank, the companies said $25.4

The treasury management unit of PNC Bank is joining RippleNet, the firm said on Wednesday (Sept. PNC Treasury Management joined the Ripple cross-border payments network that uses blockchain to facilitate global transactions.

Visa brings Click to Pay to Vietnam A growing number of Vietnamese banks have become early adopters of Visa’s Click to Pay service. Instead, Click to Pay allows users to identify themselves through their email address or mobile phone number.

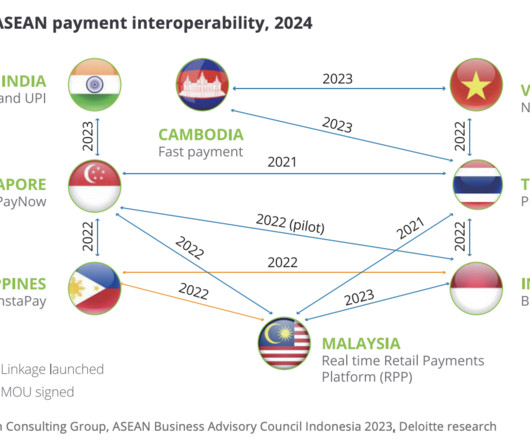

year-over-year (YoY), according to the National Bank of Cambodia (NBC). To strengthen its cross-border payment capabilities, the Cambodian government has expanded Bakongs integration with global platforms such as Alipay+ , Malaysias Maybank , and South Koreas JB Financial Group. million transactions in 2023, up 28.7%

TransferMate Announces Strategic Partnership with Deutsche Bank Embedded B2B payments infrastructure-as-a-service company TransferMate has forged a strategic partnership with Deutsche Bank. The partnership will enable TransferMate to provide in-country collections, cross-border payments, and local fund storage.

The expansion of Exactly.com Spain Coverage enhances local payment performance and fortifies cross-border capabilities. Bizum has emerged as a well-established mobile payment solution in Spain, offering instant transfers directly between bank accounts via users’ mobile numbers. million transactions daily.

To serve eCommerce companies’ needs, as transactions continue to shift online, banking needs to go digital, too. As has been profiled in this space previously, virtual IBANs serve as reference numbers issued by banks. Platforms and single access points help bridge the gap between traditional banks and eCommerce.

Payoneer has quietly built one of the most robust and widely used financial platforms for cross-border payments. It powers financial operations for a global workforce, from the gig economy to Amazon sellers, offering multi-currency accounts, mass payout infrastructure, banking alternatives, and working capital products.

The widespread shift to online reliance has created a greater demand for accessing various services online, including government public services and online retail payments. This increased digital dependency has raised the need for secure access and quick and easy identity verification online.

These methods leverage digital wallets, mobile payments, bank transfers, and other innovative technologies to deliver more flexible options for consumers. Region-Specific Preferences : In Europe, 36% of online purchases are made through bank transfers, while Asia sees a dominance of digital wallets at 70% of transactions.

On top of that, 69% of Americans online in 2023 said they used digital payment methods to make a purchase. A typical payment processing procedure involves multiple parties, including the merchant, customer, payment processor, payment gateway, issuing bank, acquiring bank, and card networks. billion transactions and $9.76

As digital wallets reshape finance and big tech challenges traditional banks, who will control the future of money? The partnership signals a potential shift in power, where platforms like X aim to rival traditional banks in how money moves and who controls financial access.

Visa’s new AI-enabled solutions offer regional partners including AI platforms, fintechs, banks, and merchants a seamless way to connect to the Visa network to deliver secure, frictionless payment experiences. Visa is also collaborating with local banks in Vietnam to launch Flex Credential in the next few months.

Perhaps most critically, tokenisation enables interoperability, a prerequisite for any payment system that hopes to scale across borders, devices, and partners. This is what distinguishes tokenisation from being solely a security measure: its enabling of cross-border capital flows, fractional ownership models, and financial inclusion.

Banks do not always have the budgets or resources to craft cutting-edge online and mobile experiences, although they can no longer afford to put off digital transformations. The number of onlinebanking customers is growing worldwide, and FIs’ consumers are coming to expect seamless digital experiences as a result.

TL;DR You get to choose from traditional payment methods like cash and checks, online payment methods like digital wallets and ACH transfers, and emerging payment methods like BNPL services and cryptocurrencies. They let buyers initiate payments by placing their mobile phone near a compatible payment terminal.

In the landscape of commerce, mobile payments have emerged as a disruptive force, altering the way people engage in financial transactions. As technology advances and consumer preferences evolve, the trajectory of mobile payments promises unparalleled convenience, robust security, and seamless integration into our daily lives.

Facilitating cross-border payments can be problematic for businesses and their partner banks, especially as real-time payment platforms become more popular. The cross-border payment problem . Third-party providers cannot eliminate all the frictions associated with cross-border payments, however.

Choosing the right one can change how you operate, how fast you grow, and how well you serve your customers, especially if you plan to offer cross-border payments. That means actual funds reside in their account inside your system, not just a link to their card or bank. They sound similar, but they serve different purposes.

We often explore how fintechs are changing the banking and payments landscapes, and sometimes look into how their solutions are supporting financial inclusion and helping people develop healthy financial habits. Sending cross-border payments, for example, often comes with heavy processing costs and conversion fees.

This solution aims to simplify cross-border payments for education agents and international students, addressing a key challenge in the education industry. By eliminating the need for multiple redirects, students and education agents can now securely complete large cross-border payments through a single interface.

European Payments Initiative (EPI) , a European-grown player committed to offering a sovereign payment solution to all consumers on the continent, has announced the launch of its mobile-first wallet and instant account-to-account payment solution, wero , for customers of German Sparkassen and Volksbanken, Raiffeisenbanken.

Cross-currency money transfer firm Western Union has announced the launch of Digital Location, a new tool that enables people to send money from home. A card is used for payouts into any bank account, digital wallet or agent locations supported by Western Union. Over 40 countries have the ability to use the Western Union Mobile app.

The move is an attempt to make it easier for those students to make cross-border transactions. Paying tuition used to be a difficult process, and involved exchanging yuan to South Korean won at a bank and then paying the university, noted the report. Now, the process is shortened to several minutes, according to Tencent.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content