This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

ORO Bank, touted as Asia’s first full-reserve digital bank, leveraged global financial software provider Finastra’s SaaS core banking solution to launch its cloud-based platform within six months. The Bhutanese bank had launched last week.

To tackle this menace, regulators have slapped fines on banks who fail to stop money laundering. It’s not that banks haven’t put in controls to tackle this menace. Each bank has dedicated large teams whose sole purpose is to monitor financial and non-financial transactions and identify and create suspicious activity reports, or SARs.

Taiwan, along with South Korea, Hong Kong SAR, and Singapore, forms the group known as the ‘Four Asian Tigers,’ renowned for their rapid industrialisation since the 1960s. Additionally, nearly 80 per cent of these banks utilise blockchain technology, particularly for certifying letters of credit.

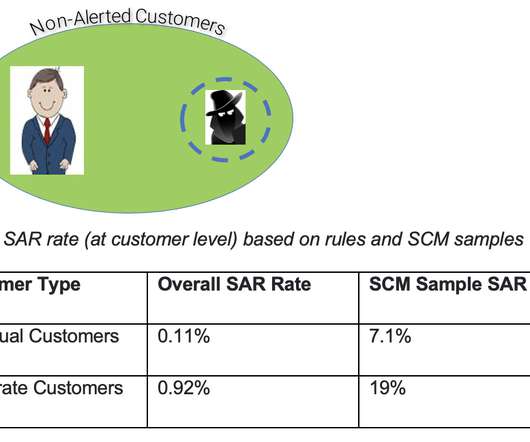

As regulations become ever more demanding, the rules-based systems grow more and more complex with hundreds of rules driving know your customer (KYC) activity and Suspicious Activity Report (SAR) filing. Using Bayesian learning , we take customers’ banking transactions in aggregate and generate “archetypes” of customer behavior.

For instance, Aite Group LLC in its 2015 report Global AML Vendor Evaluation noted that “increasingly, regulators recognize that rules alone are not an effective manner of detection and are pressuring banks to include more sophisticated analytics.” The weights of the model are either expert-driven or based on limited SAR data.

FICO’s new Anti-Money Laundering (AML) Threat Score and AML Soft-Clustering Misalignment Score, respectively, help large global banks and financial institutions to achieve a 50%+ reduction in alert false positives , and reveal outlier transactions that are highly likely to be money laundering, and otherwise not alerted.

The US subsidiary of a Canadian bank was issued a fine of $65million for unsafe practices related to operational, compliance, and strategic risk management controls. The bank was ordered to pay the fine to resolve investigations by The Office of the Comptroller of the Currency (OCC), an independent bureau of the US Department of the Treasury.

A recent guest blog presented by G2 Web Services explores the obligations acquirers and third parties have when it comes to filing a Suspicious Activity Reporting (SAR) form if there is any suspicion of transaction laundering. To learn more about who, when and why to file a SAR per the Bank Secrecy Act, please see the infographic below:

BankShift BankShift is a brand-on-banking ecosystem for digital banking platforms, crafted by humans with experience in digital-first and data-driven innovations from leading financial institutions and brands. Banks, credit unions, payment providers, and financial institutions focused on unsecured consumer lending.

A partnership aimed at helping banks, payment providers and fintechs meet the ever stronger regulatory demands while reducing effort and expense. . We serve corporates, insurance companies, and banks – be it a retail, private, wealth management, automotive or telecom bank, tier 1 or tier 3 bank. What do you do?

From its Vision 2030, to the launch of its new open banking framework, the Kingdom is a frontrunner in fintech innovation. The new annual event is hosted by the Financial Sector Development Programme (FSDP), Saudi Central Bank (SAMA), Capital Market Authority (CMA), Insurance Authority (IA), and co-organised by Fintech Saudi and Tahaluf.

He noted three ways AI systems improve on traditional AML solutions: More effective than rules-based systems: “As regulations become ever more demanding, the rules-based systems grow more and more complex with hundreds of rules driving know your customer (KYC) activity and Suspicious Activity Report (SAR) filing.

The Bank Secrecy Act (BSA) establishes AML program requirements for financial institutions in the US while the USA Patriot Act lays down which entities are required to comply. As such, the Bank Secrecy Act (BSA) establishes certain AML program requirements for financial institutions in the US. Let’s get started.

They establish your identity by non-intrusively examining user patterns (such as keystroke analysis of the way you enter your password), geolocation, and other behaviors around your device, such as your gait and which browser you prefer. 3: FICO Digital Banking Study: Security And Authentication In A Digital World.

As more people have worked, learned, banked, exercised, relaxed, and even sought medical care from home during Covid-19, they have gotten a crash course in just how much can be accomplished at home. Branchless banking. BANKING, HEALTHCARE, RETAIL SECTORS LIKELY TO EXPERIENCE SIGNIFICANT GROWTH IN CHATBOT USE. Branchless banking.

The global march of the challenger banks carried on, now with the announcement that EI incumbent Monzo is looking to raise $130 million to, among other things, mount a U.S. Speaking of profound changes … The March Of The Challenger Banks. has its own challenger banks — not to mention thousands of regular banks and credit unions.

Duguid before the end of June 2021, I believe the court will not only provide some clarity on what an ATDS is but, in doing so, will further facilitate the use by banks and other businesses of legitimate, non-marketing automated or prerecorded voice and text messages to the mobile phones of customers who have the provided requisite consent.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content