This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

NACHA — The Electronic Payments Association — announced that its membership has approved three new rules that will expand Same-DayACH for all financial institutions and their customers. Funds from Same-DayACH credits processed in the existing first window will be made available by 1:30 p.m.

With the SameDayACH rollout coming in just two weeks and other faster payments initiatives taking off, financial institutions are taking significant steps to ensure the transition to a faster processing environment, including improving their payment security platforms to keep fraudsters at bay. How Fraudsters Attack.

Unlike traditional ACH transfers, which can take several days to process, instant ACH transfers significantly reduce the waiting time, making funds available to recipients within minutes. When users initiate an instant ACH transfer, their financial institution sends the transaction details to a payment processor.

13, 2018, NACHA , the rules and standards body for the ACH network, announced that its voting members had approved amendments to the NACHA Operating Rules & Guidelines to establish a third SameDayACHprocessing and settlement window,” the Federal Reserve wrote in the announcement. . “On Sept.

The good news is that SameDayACH is on the way, but experts continue to discuss how the initiative will impact corporate payments, if at all. At the center of many of these discussions is the issue of ACH underwriting, which sees FIs establish how long it takes for funds to actually settle into an account.

The October edition of the PYMNTS Faster Payments Tracker™ , powered by NACHA, looks at notable developments in the global remittance market, including new real-time payment tools for SMBs, blockchain and the latest trends in faster payments infrastructures, including the recent rollout of SameDayACH Phase 2.

As described by Stone, T+3 settlement has been the standard for most stock market and mutual fund trades since 1995 when it replaced the T+5 settlement process. As T+3 was being implemented in the early 90s, the concept of using ACH was raised, but there were two problems that, at the time, were insurmountable.

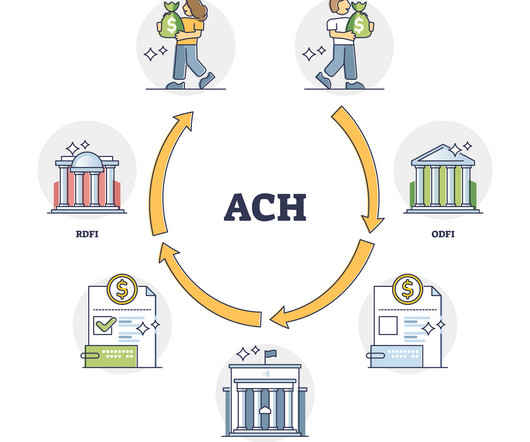

ACH transfers are managed by the National Automated Clearing House Association (NACHA) , which ensures a safe and efficient way to make various financial transactions, including direct deposits, direct payments, tax payments, and other business payments without the need for physical or cash. What is an ACH transfer limit?

Read on and learn everything you need to know about ACH transfers , including their types, benefits, potential downsides, and their alternatives. What Is ACH Bank Transfer?: ACH transfers are electronic, bank-to-bank money transfers processed through the ACH network.

Understanding the ACH deposit meaning is important because it’s a fast, secure, and cost-effective way to transfer money. In this article, we’ll break down the meaning of an ACH deposit and how the process works. We’ll also show you how ACH deposits can benefit your personal finances and business operations.

In fact, he said, they often create even more friction for small businesses because of interchange fees that can tack on a 3 percent processing charge for each of those dozens, or even hundreds, of transactions. Alas, ACH is a far-from-perfect payment rail, Koeppel admitted.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content