This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The results reflect growing adoption of the FedNow Service and RTP Network and an expanding array of usecases in both consumer and business contexts. However, challenges such as interoperability and fraud must be addressed to fully unlock the potential of faster payments.

Payment Service Providers must strengthen due diligence, monitoring, and collaboration with regulators to address these risks. Financial regulators are intensifying scrutiny, highlighting gaps that PSPs must urgently address. This may be due to unclear PSP policies regarding target customers, acceptable usecases, and associated risks.

Each ID-Pal Once profile is built from already-verified identity data, but critically, this information is re-validated against an organisation’s own risk rules, without requiring the enduser to repeat the submission process. This ensures ongoing compliance while minimising user friction.

What is Project Nexus, and how does it address today’s cross-border payment challenges? Nexus aims to address each of these areas directly. On top of that, the platform can support a competitive FX marketplace, so institutions can access better rates, further lowering overall transaction costs, also benefiting the endusers.

It highlights major trade-offs in security, privacy, and policy that must be addressed before offline CBDC payments can scale. Many people still don’t use smartphones for payments, and low tech literacy adds to the challenge. More complex risks, like counterfeiting and double spending, also need to be addressed to build trust.

. “Organisations are now thinking about how AI specifically applies to them, and they are leveraging these benefits across their operations and customer-facing services to address challenges specific to their workflows, industry and endusers not just joining the AI hype because its trending.

These may include: Configuring the software or payment platform and terminal settings Integrating the software with other apps and other software Migrating the data to the platform Training their team on using the product 6. Integrated payment processing is crucial as it provides convenience and improves the user experience.

Integrating Swift with the upgraded FPS would enable a unique reference to be embedded within each transaction, delivering end-to-end tracking across both cross-border (Swift) and domestic payment flows. To date, Swift has enabled European VoP providers from France, Italy and the Netherlands to expand their reach across borders.

Its infrastructure supports a business-to-business-to-consumer (B2B2C) model that facilitates stablecoin yields, denominated in USD and EUR, for endusers through partner platforms. They described OpenTrade’s model as one that is positioned to address structural gaps in access to stablecoin-based yields.

Despite an abundance of performance data, many firms still lack visibility into what really matters: how systems function at the point of use. Without insight into the end-user experience, problems often go undetected until they escalate into serious disruption. It expresses the views and opinions of the author.

The B2B opportunity in distribution A true upside By addressing the financial needs of their distribution channels, companies using embedded finance solutions enhance the operational capabilities of their merchants and solidify their role as essential partners.

Increasingly, consumer and corporate endusers of various platforms are seeking a more seamless experience, and the owners of those platforms are finding a big opportunity to integrate a range of financial products and services, from payments to financing. But across usecases, Bloh said two key themes are emerging.

That is to say, mass adoption will take time, and the factors driving that adoption will almost certainly continue to change and shift as endusers’ needs do the same. There are a few major pain points in corporate cross-border payments today, Halpin explained, which are greatly addressed with faster and real-time payment networks.

The study sheds light on how various factors, including usecases, benefits, and industry challenges, are shaping the future of instant payments. “The widespread adoption of instant payments will not only enhance user experiences but will also foster greater competition, innovation, and inclusion in financial services. .

Increasingly, those value-added services are not only focusing on speed of payment, but also enhancing the data that end-users can access about their transactions, with new solutions from Bank of America and Scotiabank some of the latest to bring real-time rails to corporates. Visa Talks Payment Rail Innovation.

The small business FinTech arena continues to blossom as more developers explore ways to address a market historically underserved by traditional financial institutions (FIs). The Front-End Strategy: UX. The opportunities to address friction in the B2B banking arena are numerous. The Back-End Strategy: Flexibility.

AI Integrations At Planful, their vision lies in delivering a complete, off-the-shelf AI solution for structured and dynamic planning usecases. Their in-house experts possess a deep understanding of the frustrations finance teams face, resulting in a tool specifically designed with AI to address complex technical needs.

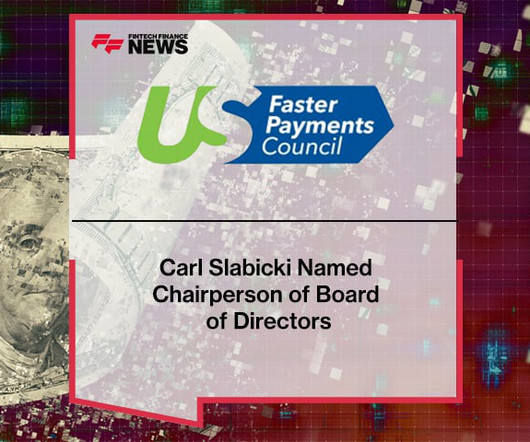

As the FPC looks to add even more value, Carl’s experience and judgment will be invaluable in assessing the growing need for coordination and standardization to streamline the adoption of faster payments across various usecases.” The post Carl Slabicki Named Chairperson of U.S.

The key to Web3 development focuses on providing a user-friendly interface and experience for decentralised applications. It’s common for end-users to interact with Web3 applications instead of the blockchain directly. These native and powerful browser applications are numerous and well-suited to financial usecases.

Investors at Alcedo Digital Ventures provided the investment, which Envoy said will be used to accelerate company expansion in the Latin American market, as well as to develop new functionality around its NVOY Stellar cross-border payment solution. ClearMetal.

It allowed for the emergence of various usecases and innovative solutions to address customer needs. Whether evolution or revolution, the future of finance promises exciting possibilities for both industry players and end-users alike. The post Evolution or Revolution?

ISVs, or Independent Software Vendors, are businesses that develop and distribute software products to end-users. ISV software products are tailored to meet the specific needs of industries and users. Customer Support In-house support teams maintain direct relationships with end-users for assistance.

Finding that right balance between what financial institutions obviously need to cover from a regulatory perspective and eliminating friction from the enduser experience isn’t so easy — especially when many millennials haven’t built up enough of a credit profile for banks to easily make that call. It’s All About The UseCase .

These comment letters highlighted the need for features to address accessibility, interoperability, security, liquidity, and fraud prevention,” Montgomery said. Interoperability, he added, will be fostered through the use of ISO 20022, for standardized messaging. Certainly FedNow is addressing the instant payment component of that.”.

FinTechs and banks continue to develop new solutions to address many of the biggest pain points of global business payments, from speed to foreign exchange. “A lot of FinTechs are coming into the space at scale, building the pipes, building the connections, applying technology to lower costs for endusers,” McCarthy said.

The Real-Time Recurring Work Group will promote the development and adoption of real-time recurring payment solutions to be used by business endusers and financial institutions. The list of usecases for real-time recurring payments has grown substantially in recent years.

With a focus on addressing these data pain points, EvoluteIQ connects businesses to technology designed for "citizen users" — that is, endusers that are not data analytics by specialization.

However, the idea that digital assets are exclusively some form of currency is slowly falling by the wayside as different usecases are emerging and being rapidly adopted. The potential usecases and benefits for users are hazy at best. In recent years, digital currencies have been all the rave.

Efforts were also made to advance digital assets, tokenization and central bank digital currency (CBDC) experimentation with initiatives such as Project Guardian and Project Orchid expanding to include more usecases and moving towards “live” pilots.

Additionally, our tech partners are really starting to understand merchant challenges and working with our merchants to address key usecases to help streamline a secure checkout experience.”. These platforms enable ads with highly relevant and engaging content for the enduser,” said Wind.

Liability needs to be shared across the chain, he said, but the first pieces of data and the initial relationships between the end-user and the organization that they are directly interacting with are the most important. The Micro Level. There is ample technology to help solve these challenges.

It’s another story in the financial services community, of course, where banks and FinTech firms have accelerated their embrace of the application program interface (API) to open up data and unlock new product development opportunities for endusers — from individual consumers to multinational corporates.

Few usecases have the potential for growing volumes as do commerce payments yet paying a merchant with a credit push transfer isn't easy. Thise session envisions the art of the possible for commerce usecases in the U.S. (Foundry Ballroom) Payment networks need volume to scale and keep costs low.

And as payments are done in bits and bytes, across all manner of usecases, consumers prize convenience and personalization. Fraud is always top of mind – and the webinar will address whether the digital age necessarily means higher vulnerability to attacks.

In some cases, lack of understanding of usecases within an organization or the resources needed to support faster payments adoption may be contributing to this feeling of complexity, and ultimately, may be holding back implementations.

The inaugural Faster Payments Barometer was widely circulated and received well over 700 responses from a broad array of payments stakeholder segments including financial institutions, core processors, payment network operators, business endusers, acquirers, fintechs, and more. The survey was conducted from Sept. 18 – Oct.

In this comprehensive guide, we'll explore everything you need to know about RPA - from what it is and how it works to its benefits, usecases, pitfalls and more. Robotic Process Automation (RPA) is a game-changing technology that enables businesses to automate repetitive and mundane tasks using software robots.

FinTech still exists as a fragmented market, where businesses striving to offer payment services to endusers pick and choose among providers, integrate with those providers, and must often navigate across complex technological and regulatory hurdles as they expand into new markets. The process is a complicated one.

Far-flung governments are requiring banks to make customer data available to third parties in an effort to provide services and provide transactions for those endusers. But the road to progress and innovation can be a bumpy one, at least when it comes to certain endusers adapting to, and adopting, Open Banking.

QR codes have enjoyed mounting adoption in the consumer payments landscape around the world in recent years as FinTech solutions embrace end-user efficiency and take advantage of smartphone penetration. Their use for B2B payments, however, remains limited — but in the U.K., open banking may be able to change that.

.’s broader digitization initiative to address changing customer demands for modernized, efficient services and products. Head of Digital Transformation Jonathan Holman said in a statement, pointing to the “speed, transparency and ease of use” that endusers require from their banking services.

That means financial functions beyond banking are taking advantage of application programming interface (API) data integrations, with productivity gains particularly large for business end-users of these products and services.

“Connect the dots” is used as a metaphor for describing how a series of discrete events can explain a “big picture” – often high-impact – action or outcome. Card rails are using push payments to close those gaps and support many new usecases for instant money. See First Data and Fiserv. See Visa and Earthport.

More established financial players offer scale and reach along with decades of experience in touching millions, even billions, of endusers’ financial lives. This includes prepaid card offering VamosPay, which is building new usecases to serve the Latino community through prepaid cards and other solutions. “We

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content