This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Embedded payments are becoming a staple in the B2C world, and more businesses are also jumping on board, aiming to streamline and automate processes from payroll (automated invoicing) to procurement (trade credit). However, B2B transactions in embedded payments are more challenging and don’t flow as easily as B2C ones.

Guavapay’s flagship products, MyGuava (B2C) and MyGuava Business (B2B) payment apps offer users to open accounts in over 20 currencies, including GBP, USD, and EUR. With these accounts, users can send local and international real-time payments at competitive fees.

Take two announcements from just last week, related to the evolution of fasterpayments in the U.S. First, there was the Fed’s decision to slow fasterpayments progress via Same Day ACH because it wasn’t ready to approve another processing window during the day. Then came PayPal’s debut of Instant Transfer to Bank.

Bolstering growth through collaborations Guavapay’s flagship products, MyGuava (B2C) and MyGuava Business (B2B) payment apps enable users to open accounts in over 20 currencies, including GBP, USD, and EUR. With these accounts, users can send local and international real-time payments at competitive fees.

While B2B payments innovation often takes a page or two out of the business-to-customer (B2C) payments world, the rise of the gig economy and freelance professionals have challenged the payments space to develop solutions that can appear to be a hybrid of corporate and consumer solutions.

When you’re a small business, and you have 60 or 80 payments a month, automation is nice, but it’s definitely not the value proposition that will shift businesses off checks.” It’s among the biggest differences between B2B and B2Cpayments, Bar noted. Where FasterPayments Fits. The result?

In addition, they can spare tenants from fines related to late rental payments by helping them more rapidly move money into their landlords’ accounts. . Simply developing new real-time payment rails is not enough, though. Easy Consumer Access . That popularity has largely continued, and the service processed 754.5

Corporate payments still don’t have a clear role in driving the adoption of fasterpayment technologies and systems in the U.S. Still, others have said that B2B payments should be largely left out of the fasterpayments conversation. “Our [payment] systems are looking at 24/7/365 solutions.

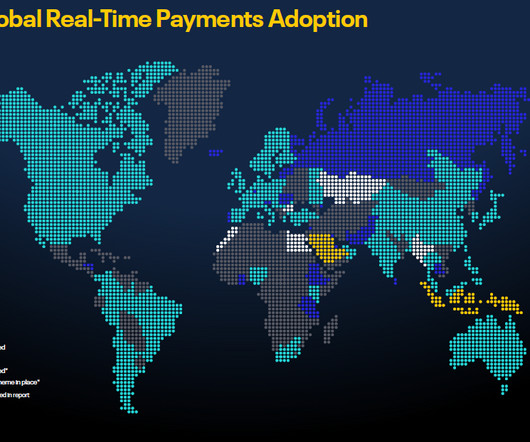

To get a sense of where fasterpayments are headed, look to the consumer. There are dozens of fasterpayment schemes rooted or taking shape around the world — 54 at last count. That’s a staggering leap from the 14 live fasterpayment schemes that existed worldwide in 2014, when FIS first released Flavors of Fast.

Traditional banking activities, done though traditional (brick-and-mortar) banking conduits can prove costly, unwieldy, paper-based and time-consuming — particularly as funds cross borders, payment schemes and currencies. Discussing flexibility, she said businesses can get access, through virtual IBAN, to many payment types.

The digital economy is here and, for many consumers, it has become a way of life. Direct deposits, push payments, eWallets, same-day ACH transfers, PayPal, Zelle and myriad other platforms and tools are now second nature. But, with this progress comes friction in the form of a payments patchwork. Supply and Demand.

The demand for mobile disbursements comes as more consumers rely on their smartphones for their financial needs. These individuals also expect fasterpayments in their day-to-day lives thanks to their interactions with peer-to-peer (P2P) payment apps. consumers now use mobile payment apps.

The March edition of the PYMNTS FasterPayments Tracker TM , powered by NACHA, covers the latest news and developments in the FasterPayments world, including the most recent notable player forays with the blockchain, like IBM ’s recent announcement of Blockchain-as-a-Service. The Power Of Payments.

Fasterpayments solutions must meet a variety of demands. Small retailers want to keep their cash flow moving by receiving consumerpayments quickly, while large corporations need improved data and visibility to ensure their B2B transactions arrive on schedule. In addition, the rails are expected to benefit B2Cpayments.

They can eliminate the pain points in business-to-consumer (B2C) transactions by keeping consumers from waiting to receive their funds, while businesses are witnessing the advantages of using real-time payments when transacting with each other. Immediate disbursements are gaining favor in various industries and sectors.

It seems an especially low number when considering this stat: Only 3 percent of companies meet customer demands for instant business-to-consumer (B2C) payments. As much as 80 percent of firms still rely on paper checks when it comes to making business-to-business (B2B) payments. The Larger Picture.

Corporates may not be adopting faster and real-time payments technologies as fast as consumers, but that doesn’t mean the acceleration of payments isn’t impacting corporate finance. But FX management isn’t the only area of corporate treasury seeing positive disruption from fasterpayments.

However, to push insurance providers in the direction of ePayments, service providers have to acknowledge the nuances of the insurance payments machine. Consumerpayment solutions like Venmo and Zelle are taking off because they rely on less data to move funds as quickly as possible. “That’s the difficult part.”

During the 2020s, almost all businesses will have been looking at b2b payments processing solutions to meet changing consumer needs. Online and contactless adoption multiplied, and digital payments rose. consumers using two or more types of digital payment methods increased by 8%.

Developers are increasingly exploring how to address some of the biggest B2Cpayment friction points in the market, most notably the pain of renters making monthly payments to landlords, often via paper check or clunky, fee-heavy online payment portals.

For small and medium-sized businesses (SMBs) and consumers, payments that arrive promptly are worth far more than payments of the same dollar value that trickle in after weeks of delays. Payment speed can be dragged down in many ways. FasterPayments Deliver ‘Instant Gratification’ for India’s Migrant Workforce.

Real-time payments aren’t just an opportunity for consumers to send and receive money more quickly. Interest in fasterpayments is also on the rise for corporates, though their adoption of real-time payments won’t look the same as it does in the B2C world.

Subscription Payments Meet Emerging Markets. Subscription-based offerings can be key to helping business-to-consumer (B2C) companies establish long-running relationships and lock down more predictable revenue streams. Effective subscription offerings require careful strategizing around payments, however.

B2B payments have a reputation for being slow to innovate , though the last couple years has challenged that notoriety. Fasterpayments initiatives, blockchain and other disruptions all show promise to make major changes in the B2B payments space. Regulation Throws FinTech Off-Guard.

Few are investing energy in building taller silos for their data, bumpier and more friction-filled experiences for their customers, or slower and more opaque payments processes. He noted that with rates being as volatile as they’ve been of late, time in this instance is literally money for consumers, possibly quite a lot of it.

As a result, firms lagging behind in fasterpayment investments could miss out on the full opportunities available in the global business-to-consumer (B2C) solutions market. “A

As a result, firms that are lagging behind in fasterpayments investments could miss out on the full opportunities available in the global business-to-consumer (B2C) solutions market. The new FasterPayments Tracker highlights the latest fasterpayments developments from several global markets.

The rise of Zelle , and any number of peer-to-peer (P2P) payment options, has increasingly brought consumers on board with the need for speed in payments — where settlement is marked by seconds and minutes, not hours or days. to fully embrace real-time payments for both B2B and B2C activity.”.

The conversation took place against a backdrop where, as reported in the Next-Gen Debit Tracker , non-cash payments have been rising 6 percent a year, and where payroll cards and debit transactions are gaining ground. Debit really is — and always has been — about fasterpayments,” Schroeder told PYMNTS.

Instant payments started 2020 on a high note, however, with the adoption of real-time payments and other speedy disbursement methods increasing over the past few years. More than 42 percent of consumers received at least one instant payment in 2019, but such disbursements have a way to go before they are as common as many would like.

“I think one of the largest reasons [insurers are still using checks] is because claim payments, the paying out of a claim, is [a] loss of money, and it is really hard for companies to focus or invest resources in a place in which you are losing money already,” Michele Schmitt, senior product manager for B2B insurance technology firm Tr?v

The expansion of traditionally consumer-focused FinTechs widening their solution scope to include B2B payments tools exemplifies just how massive the opportunity is for service providers to tackle friction. The FasterPayment Demand.

Mastercard said in a release on Wednesday (June 6) that the payments service will make it possible for various stakeholders in the financial realm — ranging from financial institutions, digital customers, FinTech companies and various enterprises — to send real-time payments to U.K.-based less than 0.1 The first U.K.-based

To gain a deep understanding of the current landscape and future outlook, Rapyd conducted a global research study surveying more than 1,000 business owners and payment decision-makers from a variety of high-opportunity industries, across ten key markets: Brazil, Canada, France, Germany, Italy, the Netherlands, Spain, Singapore, the UK and the US.

The most familiar change, though, is tied to the consumer (through their acceptance or denial of requests to share and use data). to adopt APIs, such as with the Revised Payment Services Directive (PSD2). If you look outside B2B or B2C, or consumer P2P, they are needed just about anywhere,” he said of APIs.

America’s cash-strapped consumers are often burdened by the cost of healthcare, frequently struggling to make ends meet while paying for treatments. Consumers are sometimes forced to pay out-of-pocket for services, then wait weeks for their insurance companies to reimburse them. Insurance Reimbursements. Hospital Overbilling.

Patients can struggle to afford the high costs associated with medical care, and hospitals can struggle to keep the lights on when bill payments trickle in slowly. They can also threaten healthcare providers’ bottom lines and consumers’ financial securities. percent of consumers reported receiving instant disbursements.

As a result, firms that are lagging behind in fasterpayments investments could miss out on the full opportunities available in the global business-to-consumer (B2C) solutions market. The new FasterPayments Tracker highlights the latest fasterpayments developments from several global markets.

“We are not too far off when the difference between local and international payments is going to get very blurred to the point where it won’t matter.”. That includes the ability of fasterpayments initiatives to address corporate, cross-border transactions in addition to consumer, national transactions, he said.

Payments are moving toward greater speed, efficiency and choice – and in P2P payments, that’s led to the rise of financial technology giants. Syncapay, the launch of which was announced earlier this week, is a holding company that plans to acquire payments companies operating in the buyer-initiated payments industry.

As real-time payments (RTP) gain traction with consumers via peer-to-peer (P2P), the pump may be primed for business-to-business (B2B) transactions to follow suit. Key among those conduits, of course, is the Clearinghouse RTP network, where commercial real-time payments made their debut in the U.S. roughly two years ago.

Adoption of real-time payments in the U.S. The assumption, of course, is that fasterpayment functionality only has a place in the peer-to-peer payments arena. In a statement, Payrailz CEO Fran Duggan pointed to the benefits for both banks and their consumer and corporate end-customers of connecting into the RTP network.

The latest Global Recurring Payments Tracker delves into the state of global subscriptions, how much of a role consumerpayment preferences have and why speed matters so much for cross-border transactions. How Do Consumers Want to Pay? consumers were just behind at 22 percent for both types of subscriptions.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content