This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

With an initial launch date set for September 2025, experienced firms in the region are joining forces to help ensure the real-timepayments platform is successful. Antonio Soares, CEO, Dock One organisation helping in this preparation phase is Dock , the banking and digital payments provider in Brazil and Pix participant.

Guavapay’s flagship products, MyGuava (B2C) and MyGuava Business (B2B) payment apps offer users to open accounts in over 20 currencies, including GBP, USD, and EUR. With these accounts, users can send local and international real-timepayments at competitive fees.

Bolstering growth through collaborations Guavapay’s flagship products, MyGuava (B2C) and MyGuava Business (B2B) payment apps enable users to open accounts in over 20 currencies, including GBP, USD, and EUR. With these accounts, users can send local and international real-timepayments at competitive fees.

Real-timepayments aren’t just an opportunity for consumers to send and receive money more quickly. Interest in faster payments is also on the rise for corporates, though their adoption of real-timepayments won’t look the same as it does in the B2C world. Uncovering The B2B Use Cases.

New payment rails are once again in the spotlight as real-timepayments and cryptocurrency emerge as the top focuses for innovators. In this week’s look at payment rails innovation, the European Union begins paving the way for greater crypto adoption, while Mastercard expands its own crypto accelerator initiative.

While B2B payments innovation often takes a page or two out of the business-to-customer (B2C) payments world, the rise of the gig economy and freelance professionals have challenged the payments space to develop solutions that can appear to be a hybrid of corporate and consumer solutions.

It may have taken some time, but faster and real-timepayments demand continues to grow in the corporate and B2B payments context. This week's look at payment rail innovation is all about speed, both for legacy rails and new ones. SWIFT to Launch New Real-Time Rails.

They can eliminate the pain points in business-to-consumer (B2C) transactions by keeping consumers from waiting to receive their funds, while businesses are witnessing the advantages of using real-timepayments when transacting with each other. Around The Real-TimePayments World.

Will this be the year that real-timepayments — and, especially, peer-to-peer (P2P) — reach critical mass in the United States? The data points to a confluence of events, as Wilcox told PYMNTS: a readiness on the part of consumers to embrace real-timepayments, and an increasing readiness of FIs to serve them. “I

In the first service offered by Mastercard after integrating Vocalink last year, and with an eye on real-timepayments, Mastercard Send is launching in the United Kingdom. based bank accounts and receive payments by the same means.

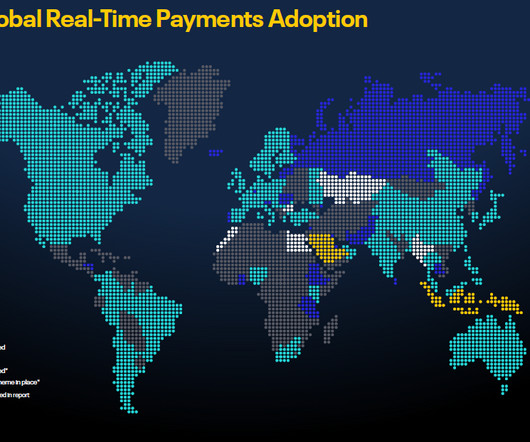

To get a sense of where faster payments are headed, look to the consumer. There are dozens of faster payment schemes rooted or taking shape around the world — 54 at last count. That’s a staggering leap from the 14 live faster payment schemes that existed worldwide in 2014, when FIS first released Flavors of Fast.

The collaboration empowers local licensed institutions and merchants to conduct a wide range of transactions, including B2B, P2P, B2C, and C2B payments. These services will support diverse cross-border use cases, including foreign education payments, e-commerce transactions, and local acceptance of gig economy payments.

2024 is expected to be a year of innovation for the fintech industry, marked by advancements in artificial intelligence (AI), cross-border and real-timepayments, cryptocurrency and blockchain, and bundled software-as-a-service (SaaS) offerings.

It seems an especially low number when considering this stat: Only 3 percent of companies meet customer demands for instant business-to-consumer (B2C) payments. As much as 80 percent of firms still rely on paper checks when it comes to making business-to-business (B2B) payments. Separately, Visa Direct debuted in the U.K.

While real-timepayments (RTP) was previously considered an infrastructure luxury, it has now become a common method of payment in many parts of the world. This adoption has changed the payments landscape. Introduction on RTP and its adoption around the world.

During the 2020s, almost all businesses will have been looking at b2b payments processing solutions to meet changing consumer needs. Online and contactless adoption multiplied, and digital payments rose. consumers using two or more types of digital payment methods increased by 8%.

The most familiar change, though, is tied to the consumer (through their acceptance or denial of requests to share and use data). to adopt APIs, such as with the Revised Payment Services Directive (PSD2). If you look outside B2B or B2C, or consumer P2P, they are needed just about anywhere,” he said of APIs. In the U.S.,

The outmoded B2B payments landscape stands in stark contrast to the business-to-consumer (B2C) and peer-to-peer (P2P) spaces where instant money and real-timepayments are becoming the norm. It works both ways as traditionally B2C sellers dip their toes into lucrative B2B waters.

billion payments Coda 2.5 billion payments, gamification Airwallex 5.5 billion payments Advance Intelligence Group Valuation: $2 billion Founded in 2016, Advance Intelligence Group is the parent company of Atome Financial, ADVANCE.AI, and Ginee. Atome Financial specialises in consumer financing, ADVANCE.AI

Western Union CEO Hikmet Ersek told Karen Webster that realtime means that receivers will have funds available to spend within minutes, enabling new real-time, cross-border, cross-currency payments capabilities for C2C, B2C and B2B use cases. “We Changing The Landscape And Overcoming The Challenges .

To gain a deep understanding of the current landscape and future outlook, Rapyd conducted a global research study surveying more than 1,000 business owners and payment decision-makers from a variety of high-opportunity industries, across ten key markets: Brazil, Canada, France, Germany, Italy, the Netherlands, Spain, Singapore, the UK and the US.

Is it prime time for realtime, especially for B2B? The rise of Zelle , and any number of peer-to-peer (P2P) payment options, has increasingly brought consumers on board with the need for speed in payments — where settlement is marked by seconds and minutes, not hours or days. Where We Stand In The US.

Payments made with cash and checks are dropping in volume — the use of cash alone declined 40 percent over the past five years in Canada. Instant payments started 2020 on a high note, however, with the adoption of real-timepayments and other speedy disbursement methods increasing over the past few years.

“I think one of the largest reasons [insurers are still using checks] is because claim payments, the paying out of a claim, is [a] loss of money, and it is really hard for companies to focus or invest resources in a place in which you are losing money already,” Michele Schmitt, senior product manager for B2B insurance technology firm Tr?v

Credit and debit card payments accounted for 75.3 percent of all non-cash payments made, with debit cards being roughly twice as popular as credit cards. Financial institutions (FIs) and payment providers are constantly looking to improve and accelerate payments for various reasons.

Adoption of real-timepayments in the U.S. The assumption, of course, is that faster payment functionality only has a place in the peer-to-peer payments arena. ’s push for real-timepayments is led by The Clearing House, which aims for ubiquity of its real-timepayments (RTP) network by 2020.

Financial players worldwide are kicking payment systems into high gear with efforts that range from easier-to-use digital solutions to new instant payment infrastructures. Roughly 40 countries had real-timepayment systems in place in 2018, and many more are currently working to provide them. Easy Consumer Access

Patients can struggle to afford the high costs associated with medical care, and hospitals can struggle to keep the lights on when bill payments trickle in slowly. They can also threaten healthcare providers’ bottom lines and consumers’ financial securities. percent of consumers reported receiving instant disbursements.

But while there are a nearly endless number of cases presenting corporate payments challenges, increasingly, businesses of all kinds are seeking a similar experience — and prepaid card technology can be a valuable tool in meeting those requirements. It’s on your phone, it’s virtual, and in seconds it’s pushing a payment to a person’s phone.”.

If the pandemic has taught banks anything, it’s that corporates need to offer a range of payment methods to their customers — whether those customers are consumers (for B2C transactions) or enterprises ( B2B ). The value lies in offering payments anywhere, anytime, across a range of B2C and increasingly B2B use cases.

Corporates may not be adopting faster and real-timepayments technologies as fast as consumers, but that doesn’t mean the acceleration of payments isn’t impacting corporate finance.

As efforts to innovate payments infrastructure continue, speed remains top priority. But it's not only consumers driving demand for realtime. Everlink, FINTAINIUM Partner For Real-TimePayments. OpenPayd Debuts Real-Time FX.

“You cannot have business resiliency without resilient technology,” Gupta said, adding that "it's becoming critical to ensure that your payment infrastructure is highly resilient, highly scalable and highly available." Commerce as conducted by consumers, he said, takes such robust infrastructure for granted.

As real-timepayments (RTP) gain traction with consumers via peer-to-peer (P2P), the pump may be primed for business-to-business (B2B) transactions to follow suit. Key among those conduits, of course, is the Clearinghouse RTP network, where commercial real-timepayments made their debut in the U.S.

Still, others have said that B2B payments should be largely left out of the faster payments conversation. remains in its early days of faster and real-timepayments adoption, so neither of these two schools of thought have been proven correct.

When you’re a small business, and you have 60 or 80 payments a month, automation is nice, but it’s definitely not the value proposition that will shift businesses off checks.” “Buyers and sellers in the B2B world, they do not share interests, many times,” he said. The result? Conflict Of Interest.

A good education on this online retail trend — an education backed by original data — comes from Azita Habibi, business development lead at Braintree , a payments services firm owned by PayPal. The research shows that 58 percent of consumers have participated in contextual commerce experiences. Igniting B2B eCommerce.

Things have changed of course, because the very nature of payments has changed, and is changing. Batch processing, increasingly, is giving way to real-timepayments and processing throughout the day. As a result, treasurers must grapple with the notion (and the needs) of cash crossing accounts many times a day.

This new feature, available to PayPal customers in good standing, leverages the company’s partnership with Chase, and Chase’s connection to The Clearing House’s RTP network, to move money instantly into the bank accounts of consumers and SMBs. Meanwhile, there are already two ubiquitous faster (than before) payments rails in the U.S.:

The latest Global Recurring Payments Tracker delves into the state of global subscriptions, how much of a role consumerpayment preferences have and why speed matters so much for cross-border transactions. How Do Consumers Want to Pay? consumers were just behind at 22 percent for both types of subscriptions.

Separate data from NACHA found that of the 2 million same-day ACH transactions completed in the first 11 days of the service, just 6 percent were B2B payments; the rest were made up of B2C and P2P transactions. And despite these statistics, B2B payments innovators remain confident that progress will be made.

There is never a dull moment in the world of payments and commerce, and no matter how hard you work to keep up, it can be easy to miss something. For all the progress that’s been made on digital payments , the world still has 1.7 The Real-TimePayments Receivables Conundrum.

Paper-based payment methods such as checks and cash are awkward and cumbersome in either business-to-business (B2B) or business-to-consumer (B2C) transactions. Manual payment generation is both time-consuming and demanding, tying up personnel who could instead be focusing on other tasks.

“We may see some coexistence in the large organizations space, where cards are already used for purchasing,” Narayanan said in the PYMNTS CFO's Guide To Digitizing B2B Payments report, powered by Comdata. It's All About Timing. For some B2C firms, that meant expanding into the B2B market.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content