This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Guavapay’s flagship products, MyGuava (B2C) and MyGuava Business (B2B) payment apps offer users to open accounts in over 20 currencies, including GBP, USD, and EUR. With these accounts, users can send local and international real-timepayments at competitive fees.

Banking payments platform provider linked2pay wants to help financial institutions implement real-timepayments capabilities. 15) that banks using its Bank Centric Payments platform will now have access to real-timepayments thanks to a collaboration with Push Payments.

Bolstering growth through collaborations Guavapay’s flagship products, MyGuava (B2C) and MyGuava Business (B2B) payment apps enable users to open accounts in over 20 currencies, including GBP, USD, and EUR. With these accounts, users can send local and international real-timepayments at competitive fees.

Real-timepayments aren’t just an opportunity for consumers to send and receive money more quickly. Interest in fasterpayments is also on the rise for corporates, though their adoption of real-timepayments won’t look the same as it does in the B2C world. Uncovering The B2B Use Cases.

Take two announcements from just last week, related to the evolution of fasterpayments in the U.S. First, there was the Fed’s decision to slow fasterpayments progress via Same Day ACH because it wasn’t ready to approve another processing window during the day. The Fed’s Hat and the FasterPayments Ring.

Corporate payments still don’t have a clear role in driving the adoption of fasterpayment technologies and systems in the U.S. Still, others have said that B2B payments should be largely left out of the fasterpayments conversation. “Our [payment] systems are looking at 24/7/365 solutions.

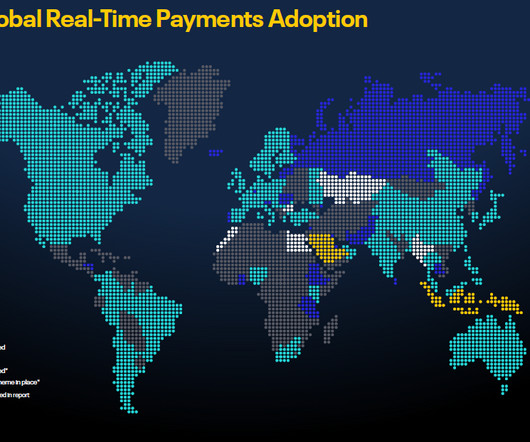

Financial players worldwide are kicking payment systems into high gear with efforts that range from easier-to-use digital solutions to new instant payment infrastructures. Roughly 40 countries had real-timepayment systems in place in 2018, and many more are currently working to provide them. APIs for Businesses.

In the first service offered by Mastercard after integrating Vocalink last year, and with an eye on real-timepayments, Mastercard Send is launching in the United Kingdom. based bank accounts and receive payments by the same means. The firms said that only a very small number of accounts in the U.K. less than 0.1

While B2B payments innovation often takes a page or two out of the business-to-customer (B2C) payments world, the rise of the gig economy and freelance professionals have challenged the payments space to develop solutions that can appear to be a hybrid of corporate and consumer solutions.

They can eliminate the pain points in business-to-consumer (B2C) transactions by keeping consumers from waiting to receive their funds, while businesses are witnessing the advantages of using real-timepayments when transacting with each other. Around The Real-TimePayments World.

To get a sense of where fasterpayments are headed, look to the consumer. There are dozens of fasterpayment schemes rooted or taking shape around the world — 54 at last count. That’s a staggering leap from the 14 live fasterpayment schemes that existed worldwide in 2014, when FIS first released Flavors of Fast.

.” On the other hand, he said, consumer-facing payment tools like Venmo are too simple for small businesses to deploy in their supplier payment operations. Businesses that embrace Venmo in their personal lives, as well as high-tech B2Cpayment solutions like Square, end up in the back office mailing paper checks.

It seems an especially low number when considering this stat: Only 3 percent of companies meet customer demands for instant business-to-consumer (B2C) payments. As much as 80 percent of firms still rely on paper checks when it comes to making business-to-business (B2B) payments. After all, fasterpayments impact cash flow, too.

The March edition of the PYMNTS FasterPayments Tracker TM , powered by NACHA, covers the latest news and developments in the FasterPayments world, including the most recent notable player forays with the blockchain, like IBM ’s recent announcement of Blockchain-as-a-Service. The Power Of Payments.

The enterprise is still unsure about faster and real-timepayments. With companies paying suppliers on strategic schedules, real-time transactions aren’t always necessary — or beneficial — for the B2B payments space. Yet there is some adoption of fasterpayment technologies among corporates.

Corporates may not be adopting faster and real-timepayments technologies as fast as consumers, but that doesn’t mean the acceleration of payments isn’t impacting corporate finance. But FX management isn’t the only area of corporate treasury seeing positive disruption from fasterpayments.

Federal Reserve is turning heads for its attention to fasterpayments, but the Fed has recently announced yet another initiative in the payments innovation space. Last week, the Fed’s Secure Payments Task Force called for comment from industry stakeholders about what challenges they face when it comes to payments security.

Fasterpayments solutions must meet a variety of demands. Small retailers want to keep their cash flow moving by receiving consumer payments quickly, while large corporations need improved data and visibility to ensure their B2B transactions arrive on schedule. In addition, the rails are expected to benefit B2Cpayments.

While real-timepayments (RTP) was previously considered an infrastructure luxury, it has now become a common method of payment in many parts of the world. This adoption has changed the payments landscape. Introduction on RTP and its adoption around the world.

It’s a well-known fact, too, that corporate payments (the B2B kind) are ripe for digitization, and for a wholesale move away from the paper chase, where checks are still stubbornly tied to 50 percent of corporate transactions. where, for example, the Federal Reserve is mulling the development of its own real-time system. (

With the B2B eCommerce market towering over B2C’s in terms of transaction value — Forrester Research estimates the U.S. trillion by 2021 — the business-to-business payments market is primed for disruption. This is particularly true as payments accelerate. “But you need to reconcile in realtime.”

If you look outside B2B or B2C, or consumer P2P, they are needed just about anywhere,” he said of APIs. another driver of API adoption comes courtesy of the real-timepayments space, where a tailwind exists from the fact that as many as 56 real-timepayment rails will be live domestically by 2020.

To gain a deep understanding of the current landscape and future outlook, Rapyd conducted a global research study surveying more than 1,000 business owners and payment decision-makers from a variety of high-opportunity industries, across ten key markets: Brazil, Canada, France, Germany, Italy, the Netherlands, Spain, Singapore, the UK and the US.

Super apps create differentiated financial ecosystems in the back end (and front end), incorporating capabilities like an aggregation of multiple service providers, digital account origination, embedded KYC abilities and real-timepayments — to name a few. Such apps promise to be a source of innovation in the new decade.

Apply Financial’s main product Validate, which allows customers to validate payments automatically, makes use of cloud technology to let firms submit the exact pinpointed numbers for bank accounts and payment details. The move is in line with the general trend toward fasterpayments.

Business to business organizations provide services or goods to other companies, unlike business to consumer (B2C), which is when businesses transact with consumers (individuals). Business to business payments, therefore, refer to the payment processes and activities between two businesses.

Instant payments started 2020 on a high note, however, with the adoption of real-timepayments and other speedy disbursement methods increasing over the past few years. Fasterpayments may not be the most popular disbursement method, but markets are regularly adopting them for consumer payouts.

Adoption of real-timepayments in the U.S. The assumption, of course, is that fasterpayment functionality only has a place in the peer-to-peer payments arena. ’s push for real-timepayments is led by The Clearing House, which aims for ubiquity of its real-timepayments (RTP) network by 2020.

As a result, firms that are lagging behind in fasterpayments investments could miss out on the full opportunities available in the global business-to-consumer (B2C) solutions market. Several global financial institutions (FIs) appear to understand the opportunities and missed opportunities that fasterpayments can provide.

As real-timepayments (RTP) gain traction with consumers via peer-to-peer (P2P), the pump may be primed for business-to-business (B2B) transactions to follow suit. Key among those conduits, of course, is the Clearinghouse RTP network, where commercial real-timepayments made their debut in the U.S.

Among the Highlights: As fasterpayments schemes proliferate around the world — there are more than 50 separate initiatives underway globally at last count — businesses must adjust to the notion of cash settling across business coffers several times a day. That is broadening, too, and crossing borders.

This month’s Deep Dive examines the factors affecting the nation’s more than $103 billion healthcare market and how digital B2C solutions can streamline the payments process. Consumers will likely be receptive to fasterpayment methods if their interactions with other services are any indication.

Use of fasterpayments technologies, too, remains limited in the B2B sphere. Separate data from NACHA found that of the 2 million same-day ACH transactions completed in the first 11 days of the service, just 6 percent were B2B payments; the rest were made up of B2C and P2P transactions.

Institutions such as The Clearing House (TCH) and the Federal Reserve have also created payment networks that have made faster, digital payments a reality for business-to-business (B2B) and business-to-consumer (B2C) payment processes alike.

Indeed, there are plans or deployments in more than 40 countries around the globe to bring fasterpayments or real-timepayments (RTP) into the fold. to fully embrace real-timepayments for both B2B and B2C activity.”. Among the factors helping to promote the growth of RTP?

One stark takeaway from this study is that while in nine of the 10 countries included, at least 30 percent of consumers preferred bank/direct debit to pay for online subscriptions, only one of the top 44 B2C subscription sites even offers bank/direct debit as an option to pay. Speed Matters for Subscription Payments.

The magnitude of the market is attractive even to B2C FinTechs, though the industry has quickly understood that B2B problems cannot be addressed with tools and technologies designed for consumer. And indeed, some businesses in need of cross-border payment solutions have been forced to revert to those B2C solutions, with lackluster results.

“We may see some coexistence in the large organizations space, where cards are already used for purchasing,” Narayanan said in the PYMNTS CFO's Guide To Digitizing B2B Payments report, powered by Comdata. It's All About Timing. For some B2C firms, that meant expanding into the B2B market.

Whether through virtual payment technologies or fasterpayment initiatives, the B2B payments ecosystem has explored ways to accelerate the time it takes a buyer to pay its supplier. Some argue electronic payments, like credit cards, are the answer.

Businesses are now digitalizing all aspects of their systems to offer seamless payments on a digital platform. Real-TimePayments. Fasterpayments benefit both consumers and businesses.

B2C companies that had once relied on intermediaries to sell goods embraced the direct-to-consumer model, while B2B firms focused on transforming their own interactions with corporate clients. Treasurers also quickly became leaders for their firms, exploring how to adjust business models in response to dramatic changes in the market.

Since there is no mandate in place for all banks to embrace the real-timepayments system, there’s been a “slow burn,” as he called it, to get banks on board. One impediment has been the lack of ubiquity, Kohli noted. That’s not to say instant is not making an impact — and there is a natural progression at work. In the U.S.,

Some analysis concludes that B2B eCommerce is becoming more like B2C eCommerce , too, with higher demands for more personalized shopping experiences. “I think, over the next five years, we’ll see some big changes, and things like fasterpayments and real-timepayment services will change things a lot.

That is the crux of the dilemma playing out on the new real-timepayments rails arena as it relates to the B2B side of the payments ecosystem. That’s where the big payments flow – and where the big opportunities for innovation, change and disruption lie.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content