This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

With an initial launch date set for September 2025, experienced firms in the region are joining forces to help ensure the real-timepayments platform is successful. Antonio Soares, CEO, Dock One organisation helping in this preparation phase is Dock , the banking and digital payments provider in Brazil and Pix participant.

Will this be the year that real-timepayments — and, especially, peer-to-peer (P2P) — reach critical mass in the United States? The data points to a confluence of events, as Wilcox told PYMNTS: a readiness on the part of consumers to embrace real-timepayments, and an increasing readiness of FIs to serve them. “I

Is it prime time for realtime, especially for B2B? The rise of Zelle , and any number of peer-to-peer (P2P) payment options, has increasingly brought consumers on board with the need for speed in payments — where settlement is marked by seconds and minutes, not hours or days. Where We Stand In The US.

They can eliminate the pain points in business-to-consumer (B2C) transactions by keeping consumers from waiting to receive their funds, while businesses are witnessing the advantages of using real-timepayments when transacting with each other. Around The Real-TimePayments World.

If you look outside B2B or B2C, or consumer P2P, they are needed just about anywhere,” he said of APIs. another driver of API adoption comes courtesy of the real-timepayments space, where a tailwind exists from the fact that as many as 56 real-timepayment rails will be live domestically by 2020.

In the first service offered by Mastercard after integrating Vocalink last year, and with an eye on real-timepayments, Mastercard Send is launching in the United Kingdom. based bank accounts and receive payments by the same means.

The collaboration empowers local licensed institutions and merchants to conduct a wide range of transactions, including B2B, P2P, B2C, and C2B payments. These services will support diverse cross-border use cases, including foreign education payments, e-commerce transactions, and local acceptance of gig economy payments.

Peer-to-peer (P2P) payments are blazing a hotter path in the digital economy as the second half of 2019 gets underway – and there is fresh evidence that the payment method is not only growing, but helping to influence related endeavors. The freshest news from this part of the global payments world demonstrates those points.

As a result, he predicted that the entrenchment of faster payments will be a linear progression that moves from consumer-to-consumer (C2C) to consumer-to-business (C2B), then to business-to-consumer (B2C) to business-to-business (B2B). Along with demand for faster payments , the information conveyed in them has significant value.

It seems an especially low number when considering this stat: Only 3 percent of companies meet customer demands for instant business-to-consumer (B2C) payments. As much as 80 percent of firms still rely on paper checks when it comes to making business-to-business (B2B) payments. Three percent of, well, anything is not a lot.

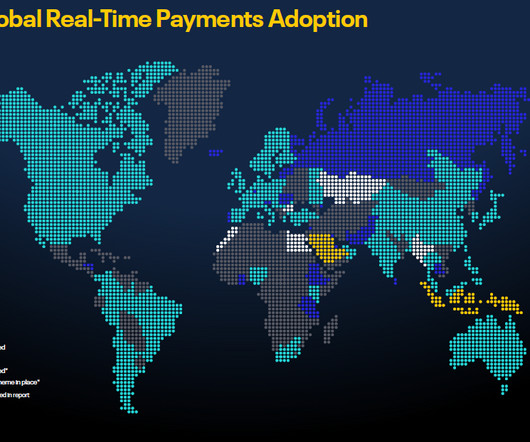

While real-timepayments (RTP) was previously considered an infrastructure luxury, it has now become a common method of payment in many parts of the world. This adoption has changed the payments landscape. Introduction on RTP and its adoption around the world.

The outmoded B2B payments landscape stands in stark contrast to the business-to-consumer (B2C) and peer-to-peer (P2P) spaces where instant money and real-timepayments are becoming the norm. It works both ways as traditionally B2C sellers dip their toes into lucrative B2B waters.

billion Nium is a global payments platform that makes cross-border money transfers easier for businesses and financial institutions. Using real-timepayment technology, Nium helps companies speed up international transactions, simplify operations, and scale. Nium Valuation: $1.4 Coda Valuation: $2.5 CGTZ Valuation: $2.41

But the speed of payments for B2B solutions still has a long way to go, with many paper checks still circulating at sluggish speeds, and high percentages of businesses requiring numerous different sign-offs before money reaches where it’s going.

As real-timepayments (RTP) gain traction with consumers via peer-to-peer (P2P), the pump may be primed for business-to-business (B2B) transactions to follow suit. Key among those conduits, of course, is the Clearinghouse RTP network, where commercial real-timepayments made their debut in the U.S.

Payments made with cash and checks are dropping in volume — the use of cash alone declined 40 percent over the past five years in Canada. Instant payments started 2020 on a high note, however, with the adoption of real-timepayments and other speedy disbursement methods increasing over the past few years.

The company also helps third-party organizations across various industries integrate instant payments with traditional payment tools into their existing payment and money movement use cases including A2A, P2P, Bill Payment, B2B and B2C disbursements.

The March edition of the PYMNTS Faster Payments Tracker TM , powered by NACHA, covers the latest news and developments in the Faster Payments world, including the most recent notable player forays with the blockchain, like IBM ’s recent announcement of Blockchain-as-a-Service. The Power Of Payments.

Still, others have said that B2B payments should be largely left out of the faster payments conversation. remains in its early days of faster and real-timepayments adoption, so neither of these two schools of thought have been proven correct. Adoption and implementation will rely significantly on market demand.

Separate data from NACHA found that of the 2 million same-day ACH transactions completed in the first 11 days of the service, just 6 percent were B2B payments; the rest were made up of B2C and P2P transactions. And despite these statistics, B2B payments innovators remain confident that progress will be made.

It was in a convergence of these trends that Visa launched its real-timepayments solution, Visa Direct , a technology enabling push payments onto recipients’ Visa cards. .” ” Unsurprisingly, this distribution model largely focuses on the massive opportunity in real-time peer-to-peer (P2P) transactions.

The rise of faster peer-to-peer (P2P) payment services has had an unintentional ripple effect for businesses, banks and merchants. As a result, firms that are lagging behind in faster payments investments could miss out on the full opportunities available in the global business-to-consumer (B2C) solutions market.

Since there is no mandate in place for all banks to embrace the real-timepayments system, there’s been a “slow burn,” as he called it, to get banks on board. Kohli said person-to-person (P2P) use cases are among the first to gain ground. One impediment has been the lack of ubiquity, Kohli noted. In the U.S.,

That faster payments, whether via the Fed or via the TCH’s Real-TimePayments (RTP) network or both, is a big threat to how banks monetize the movement of money between senders and receivers and their depository accounts. NACHA reported that in Q4 2018, SDA volume hit 51.3

EFT payments are transactions between the sender and receiver that transfer funds electronically from the sender’s bank account to the receiver’s. This can include peer-to-peer payments, and business-to-business (B2B) or business-to-customer (B2C) transactions. There are several EFT payment types that we’ll discuss in this post.

Businesses are now digitalizing all aspects of their systems to offer seamless payments on a digital platform. Real-TimePayments. Faster payments benefit both consumers and businesses. Real-timepayments offer a solution to delayed payment options like ACH transactions, credit cards, debit cards, checks, etc.

Super apps create differentiated financial ecosystems in the back end (and front end), incorporating capabilities like an aggregation of multiple service providers, digital account origination, embedded KYC abilities and real-timepayments — to name a few. Such apps promise to be a source of innovation in the new decade.

Peoples Payment Solutions — working with TELUS Health and Payment Solutions — will be among the first companies in the country to implement Visa Direct’s capabilities to enable real-timepayments, Visa said in an announcement. trillion opportunity.

After two decades of tweaking and updating its existing Real-Time Gross Settlement (RTGS) system, Hong Kong determined it needed a new rail. Kaura said FPS will also help corporations quickly reconcile accounts as well as access real-time information and payments. per transaction. Hong Kong required a new solution.

3: P2P Rises And Could Move Into B2B. Peer-to-peer (P2P) payment services are stretching their wings, heading into the new decade with mostly robust growth — and even some new plans to gain customers and keep a tight hold on existing consumers. Venmo also offers an example of P2P expansion. 10: Via Faster Payments.

Accelerating The Real-TimePayments Demand Curve: What Banks Need To Know About What Consumers Want And Need. This study showed that consumers display significant interest in real-timepayments once they fully understand them. Key Data Points: It takes only 78.5

That motion, Secil Baysal, president and COO of FastPay, noted, is the motor that drives the payments ecosystem as a whole, not just the consumer-facing side. Today, B2Cpayments are so much further ahead than B2B when it comes to digitization. For example, trying to forecast the rise of real-timepayments in the U.S.

The skewed flow of funds to the business-to-consumer (B2C) space comes amid a backdrop where valuations for domestic FinTech unicorns have been inflated. VCs have been pushing money toward a number of peer-to-peer (P2P) companies with questionable economics. In fact, he said, real-timepayments carry a relatively higher risk of fraud.

It’s a wave that was set in motion worldwide a few years ago when regulations in a few countries mandated that consumers and businesses have a right to access funds sent to them in real-time. In other words, it’s a teeny and tiny part of the payments mix in the countries where it was required to happen. Here in the U.S.,

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content