This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Mastercard uses many different interchange categories to determine the rates and fees your business pays for accepting credit cards. There isnt just a single Mastercard business interchange rate. Program Level Mastercard splits commercial interchange into 5 levels. Read more about downgrades and Mastercard Standard interchange.

In this blog, we’ll explore how to approach credit card processing like an opportunity instead of just another expense. Types of payment processing fee structures Interchange plus Interchange plus pricing is one of the most transparent and cost-effective fee structures.

If you process more than $1 million per year in Amex cards, you’ll go direct to Amex. Additionally, while Visa and Mastercard do set interchange rates, your processor is ultimately responsible for your total processingcosts. Pricing model, markup, and interchange padding all play a role in how much you’ll pay.

Reasons to Use AVS Aside from acting as a fraud deterrent, saving you the hassles of processing a fraudulent transaction and dealing with the repercussions of that, one of the biggest reasons to use the Address Verification Service is that it’s part of the required qualifications for lower cost interchange categories.

In this blog post, well help you understand the factors and features you need to consider to find the right payment gateway to suit your unique business needs. For example, most payment gateways accept payments from major credit cards like Visa and Mastercard, but only a small percentage accept Discover and American Express.

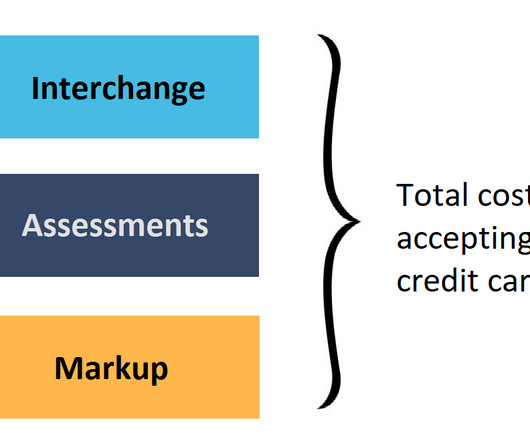

As with many things in credit card processing, its complicated. Interchange, as set by Visa and Mastercard, is non-negotiable. It isnt possible to get lower rates or fees than what Visa and Mastercard publish. Costs of Processing Interchange is one of three components of total processingcosts.

In early 2017, Visa announced a staged digital wallet fee, which came well after Mastercard imposed a similar fee in 2013. These fees can result in higher interchange costs for small businesses. Mastercard Staged Digital Wallet Fees Mastercard’s fee bears the mouthful name “Staged Digital-Wallet Operator Annual Network Access Fee.”

Mastercard states that 2 out of every 3 transactions processed on its network are now contactless, up from less than 1 out of 3 in 2020. Costs to Accept Tap on Phone Tap on phone is considered a card-present transaction and your processor will charge card-present rates. Do all credit card processors offer tap on phone?

This complicated matrix of charges based on those factors is called interchange and I’ve written about it extensively in the CardFellow blog. With some credit card processors, you pay the “true” cost of interchange, plus a markup that your processor charges. Assessment fees go to the card brands themselves (Visa, Mastercard).

In this article, were going to focus on Visa and Mastercard interchange categories and their effect on your processing fees. But if you just want a quick overview, here it is: Interchange is one of the three core components of credit card processingcosts. Along with assessments and processors markup.)

The exact rate can vary based on several factors, including the type of card used (debit or credit), the card brand (Visa, MasterCard, etc.), Viewing these costs individually makes it easier to understand what is contributing to your credit card processingcosts and where you may be able to save money.

Are you struggling with resource constraints caused by soaring credit card processingcosts? TL;DR Credit card surcharging involves adding a fee to transactions with credit card payments, offsetting processingcosts. It offsets the card processingcosts, transferring the financial obligation to the latter.

They significantly impact the cost of accepting card payments. Understanding interchange fees enables merchants to effectively manage processingcosts, negotiate better rates, make informed decisions about card acceptance, and ensure compliance with payment industry standards. Can you decrease interchange fees?

That means if a customer wants to make a credit card purchase, they’ll be charged an additional fee to cover the payment processingcosts. Although surcharging has been widely debated, it’s starting to become something of a mainstay, especially with rising processing fees. Train your staff to effectively communicate.

In this blog post, we’ll cover why it’s essential for your business and what steps you can take to get started. This can be especially beneficial for any business, including high-risk merchants , looking at ways to speed up their payment processing. Cost Savings. We’re here to help!

Interchange fees Interchange fees are the per-transaction costs charged by the credit card brands (such as Visa and Mastercard). In terms of the pricing structure for your clients, using the interchange plus model, your clients will pay the actual cost of the transaction plus any markup you add.

Capture your business spend: no Pokeball needed – TradeShift blog. Mastercard Accentuates the Digital. Mastercard ( F14 ) enhanced Masterpass , allowing consumers to make in-store payments at 5 million brick & mortar stores. billion , giving Mastercard a potentially larger role in the overall U.K.

As quoted in Forbes, Allen stated, Theres no reason banks and large companies like Visa and Mastercard should profit from the required collection of sales tax and tips. Allen is arguing that Visa, Mastercard, and acquiring banks dont provide any service related to the tax or tips and thus should not profit from those line items.

Surcharging, defined as adding a fee to purchases made with a credit card, was prohibited by the card brands (Visa and Mastercard) until a class action lawsuit in 2013. The idea is that a business can defray the costs of accepting credit cards by charging the consumers that choose to pay with a credit card. First, a quick refresher.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content