This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

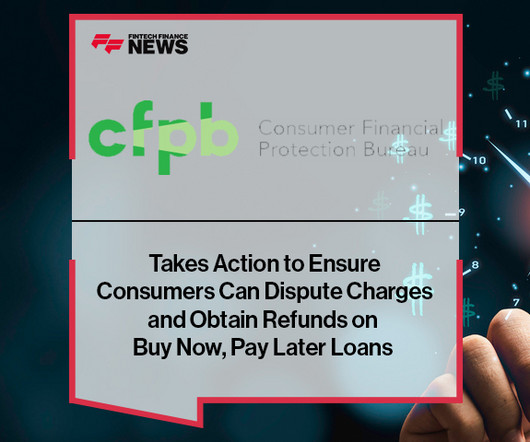

“Whether a shopper swipes a credit card or uses Buy Now, Pay Later, they are entitled to important consumerprotections under longstanding laws and regulations,” CFPB Director Rohit Chopra said.

Regulatory clarity and consistent standards are critical for providers offering safe, transparent and responsible financial services and even more important for consumers who expect protections when utilizing financial services including Buy Now Pay Later,” said Phil Goldfeder, Chief Executive Officer of AFC.

The American Fintech Council , the industry association representing responsible fintech companies and innovative banks, has welcomed new recommendations regarding buy now, pay later (BNPL) but warns that providers need more time to ensure compliance.

The Consumer Financial Protection Bureau (CFPB), a US government agency responsible for protectingconsumers in the financial sector, has ruled that buy now, pay later (BNPL) lenders must treat consumers as credit card providers do, ensuring they receive the same key protections.

The Consumer Financial Protection Bureau (CFPB) has issued an interpretive rule that confirms that Buy Now, Pay Later lenders are credit card providers. Accordingly, Buy Now, Pay Later lenders must provide consumers some key legal protections and rights that apply to conventional credit cards.

ETA supports a uniform policy framework for AI that appropriately preserves the innovation and security AI brings, while ensuring appropriate consumerprotection. Modernize the CFPB The payments industry is committed to delivering innovative products and services in a transparent and secure manner.

Consumer Financial Protection Bureau (CFPB) issued a new interpretation under the existing Truth in Lending Act. Regardless of whether a shopper swipes a credit card or uses Buy Now, Pay Later, they are entitled to important consumerprotections under longstanding laws and regulations already on the books.”

Late last month, the Consumer Financial Protection Bureau (CFPB) issued an interpretive rule stating that Buy Now, Pay Later (BNPL) lenders are credit card providers. This ruling is slated to have some significant impact on BNPL, which was once one of the hottest subsectors in fintech. territories.

The OCC outlines safety and soundness principles and appropriate risk management processes for its regulated institutions that engage in BNPL lending. The OCC expects that banks engaged in BNPL lending “do so within a risk management system that is commensurate with associated risks.” By Arthur S.

Open banking, BNPL, cybersecurity and AI will all be under the microscope for regulators and policymakers, but not all areas will see major action in 2023. The CFPB's New Open Banking Proposal Will Accelerate Exciting Product Innovations. There Will be Changes in the BNPL Market, but Major Regulatory Action Is at Least a Year Away.

For payments firms, the intersection of payments and credit is becoming a competitive battleground, especially as BNPL and embedded lending scale. While some governments prioritise competition and innovation, others focus on financial inclusion, consumerprotection, or market-driven adoption. reached $1.1

the Consumer Financial Protection Bureau (CFPB) has been studying the BNPL industry since at least late 2021. At this point, much of the CFPB’s impact on BNPL has been minimal. There has some concern at the state level , with state attorneys general voicing consumerprotection warnings.

The landscape and ongoing tug: As new payment models like Buy Now, Pay Later (BNPL) and EWA took off in recent years, the Consumer Financial Protection Bureau (CFPB) has been watching how they affect consumers. 7428 in 2024, which classifies EWA as a non-credit product with consumerprotections.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content