This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Interchange is the fee that creditcard companies like Visa and Mastercard charge businesses to accept their cards. In this article, we will break down creditcard interchange fees so you will know exactly how much you’re spending when running your business. Request Quote What Are Interchange Fees?

As consumers shop amid ongoing public health restrictions, they almost invariably reach for their creditcards — whether the physical varieties in their wallets or the digital versions stored on their browsers and mobile devices. More than ever, creditcards are becoming the coin of the realm in the global connected economy.

Marqeta , the global card issuing platform, debuted its new Tokenization-as-a-Service (TaaS) product, which allows cardissuers to access its tokenization technology, the Oakland, California-based company announced on Tuesday (Sept. It is used to instantly provision cards into a mobile wallet.

Are you struggling with resource constraints caused by soaring creditcard processing costs? Creditcard surcharging can help offset these expenses, but it can be tricky. TL;DR Creditcard surcharging involves adding a fee to transactions with creditcard payments, offsetting processing costs.

The INVEX creditcard business said on Monday (Oct. 22) that it has linked with Ondot , which focuses on mobile payments, to deliver what is being billed as the first instant digital creditcard in Mexico. They can use the digital card instantly for online commerce and manage the card using mobile devices.

The partnership will allow corporates to centralise more payment types within their travel programme, expanding virtual card use beyond core hotel and air payments. The process is seamless and requires no additional work for our bookers vs. conventional creditcard payments.”

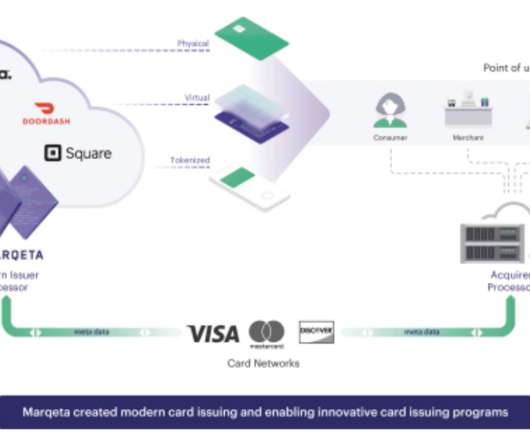

First, the acquirer-facing side of payments, which allows merchants to accept payments, has seen significantly more innovation over the last decade than the issuer-facing side, which allows businesses to customize card products for their endusers. The post Modern CardIssuer Marqeta Is Going Public.

The corporate card can have a home in the digital wallet thanks to collaborations and technology platforms designed for cardissuers. And in another Nium collaboration, the company is joining forces with Volopay to provide a new and bolstered business creditcard to let firms have a closer watch over expenditures.

In today’s competitive landscape, implementing a card product can be a powerful addition for businesses looking to enhance customer loyalty, streamline expenses, or broaden their financial offerings. Designing and launching a debit or creditcard product requires navigating a complex web of stakeholders and intricate processes.

This week's Commercial Card Innovation Tracker finds FinTechs and payment technology players like Mastercard, Visa and Nets embracing partnerships to roll out new corporate card solutions, including virtual commercial cards and small business creditcards designed to enhance spend management and help SMBs access credit during turbulent times.

Eko Investments Eko Investments ‘ white-label solution allows 10,000 banks and credit unions to offer digital investing directly on their existing banking platform. Banks and credit unions of all sizes. Merchants, retailers, brands, marketplaces, insurers, cardissuers, and logistics companies.

Commercial cards account for only a portion of corporates’ overall spend, as checks stick around and ACH gains ground. However, their market share is on the rise as cardissuers develop more robust rewards programs, and the ability to integrate card spend into back-office spend management and analytics platforms.

Creditcard skimmers are a headache for fuel retailers, but there is more than one way that fraudulent actors can target fleet spend. In addition to stolen credentials and skimmed cards at the fuel point-of-sale, employees are often able to overspend with their commercial fleet card products, or file fraudulent expense reports.

Having recently announced a $400 million Series F funding round, Nubank is developing a small business banking solution after expanding from its initial services as a creditcardissuer. While the company may be operating in a different market than the U.K., Europe, U.S.

Reduce processing fees and costs ACH payments cost much less compared to creditcard payments. Card transactions are, in fact, the most expensive mode of payment as fees are calculated based on a percentage of the transaction. It initiates data exchange among the merchant, cardissuer, and customer to validate the payment.

CEO Chris Hopen called the technology “the first ever consumer payment solution that automates both the challenge of secure account access and the ‘card on file’ problems users face every day.” “How many people have ever had to replace a creditcard?” “Was it fun?”

If that wasn’t true, there would be no need for players like Apple and PayPal to issue old-school, low-tech, network-branded plastic debit and creditcards that consumers trust and like to use – which merchants can immediately accept without any change to their POS systems. It’s always been that way and will always be that way.

It allows customers to view all of their financial transaction information dispersed at multiple institutions, such as banks, creditcardissuers, and brokerages, on a single page. Kim Sung-tae: In 2025, IBK plans to transform i-ONE Bank into an open platform based on banking.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content