This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Account takeover attacks exploit credential stuffing and social engineering techniques, with UK finance recording 34,114 cases of card identitytheft in the first half of 2022 alone, leading to gross losses of £21.4 This highlights the opportunity for smarter systems to deliver both trust and throughput, without compromising either.

Account takeover attacks Account takeover attempts by criminals: Account takeover (ATO) attempts involve criminals gaining unauthorized access to online accounts, often through stolen or compromised credentials. This type of fraud can lead to financial losses, identitytheft, and reputational damage for both individuals and organizations.

Account takeover attacks Account takeover attempts by criminals: Account takeover (ATO) attempts involve criminals gaining unauthorized access to online accounts, often through stolen or compromised credentials. This type of fraud can lead to financial losses, identitytheft, and reputational damage for both individuals and organizations.

According to the IdentityTheft Resource Center’s (ITRC) 2023 Business Impact Report , 73% of small business owners in the US reported a cyber-attack within the previous year, underlining the growing popularity of small businesses as a target among malicious actors.

For 2022, we saw a significant increase in compromised cards resulting from skimming activity. Total compromise cards were up 368% from 2021, with more than 161,000 impacted cards identified — nearly a 5x increase over 2021. Now that we have data from the entire year to review, we are seeing the alarming trend continue.

Business email compromise (BEC) attacks can be a major risk to businesses’ finances and reputations. Let’s look at what business email compromise attacks are and explore some of the many ways you can combat them. What Is a Business Email Compromise Attack? Reported losses in 2020 exceeded $4.2

Wawa is getting in touch with customers and offering free credit card monitoring, as well as identitytheft protection, to anyone who has been affected. Under Federal Communications Commission (FCC) rules, telecommunication firms are required to promptly notify users when there is a breach.

The United States Supreme Court has rejected an appeal by online shoe company Zappos over a data breach in 2012 that compromised the information of 24 million customers, according to a report from Reuters. Originally, a Nevada judge claimed only people who had suffered financial loss were eligible for damages. The 9th U.S.

district court in San Jose, California, ruled late last week that most of a lawsuit concerning Yahoo’s data breach, which exposed 3 billion users’ personal data, can proceed. Initially, Yahoo only revealed that 1 billion accounts had been compromised. According to news from Reuters , U.S.

As if Yahoo didn’t have enough on its plate, the tech company is now facing a probe from the Securities and Exchange Commission as to whether or not it could have acted more promptly in response to two massive data breaches that left over a billion customers’ information compromised. 2013 had compromised even more user data.

Once a customer has used a compromised card reader, the fraudster can download or wirelessly transfer the card details and the video of the PIN being typed, giving them complete access to the account. One of the most insidious aspects of skimming fraud is that a transaction at a compromised location usually goes through without a hitch.

Scores add precision to the broad-brush approach of rules-based detection. In the meanwhile, check out our previous posts on application fraud, including: Trends in Application Fraud – From IdentityTheft to First-Party Fraud. Best Practices in Establishing Your Fraud Risk Appetite. ELI5: How Does the Dark Web Work?

The CFPB will issue its final debt collection rule in the fall of 2020. Forty-two years after the enactment of the Fair Debt Collections Practices Act, the CFPB proposed the first set of rules governing third-party debt collection activities. I predict we will see the final rule during the early portion of the 2020 NFL season.

That’s a lot of compromised data, of course. And Equifax has taken steps to stanch some of the bleeding of personal information – you know, the kind for sale on the Dark Web – by forging new pacts focused on identity verification. The latest tally comes to 147.9 million, up 2.4 In plain language: Nobody’s happy but the lawyers.

First, think about using separate rules and strategies to address the different exposure types. Debbie Cobb is Senior Director of Product Management, serving as the global product leader for FICO’s transactional fraud solutions including FICO Falcon Fraud Manager, FICO Falcon Compromise Manager and Card Alert Service. See all Posts.

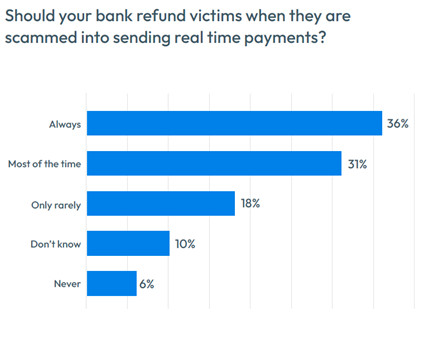

Some legislators and regulators, such in the US and UK , are pushing for rules that would require banks to reimburse scams victims for losses. Who Should Cover the Losses from APP Fraud? Consumer defection and acquisition are costly, as are customers who may maintain but cease to use an account. Debbie holds a B.A.

Financial institutions and their partners must have data security standards in place to avoid getting compromised. This helps determine who is responsible for addressing any data privacy concerns and avoiding cyber-attacks and identitytheft. It’s also important to define the roles and responsibilities of all parties.

If one of these accounts gets hacked, it can lead to more accounts being compromised, particularly if your security settings are low and you aren’t using a variety of username/password combinations. Other digital payment service users : Fraudsters may also target a cardholder’s mobile wallet app and/or full-service neobank account.

Key regulations governing EFT payments include the National Automated Clearing House Association (NACHA) rules, which establish guidelines for ACH transfers, and the Payment Card Industry Data Security Standard (PCI DSS), which sets security standards for handling card information.

This Act, which supersedes Section 43A of the IT Act, 2000 and the SPDI Rules, 2011, brings about considerable changes to the norms of data protection. The DPDP Act is lean and principle-based, with details around implementation to be set out in future rules. Appoint a data auditor to assess compliance with the Act.

She also contends that the access was permissioned and not identitytheft as Worden alleges in the complaint against her. If you ignore the previous rule, don’t do it from a computer on the space station — because when someone traces the access records to the account, one IP address labeled “NASA” is really going to be a dead giveaway.

After all, your very name, address, telephone number, maiden name and so on are all ticking time bombs, putting you at risk for identitytheft. If the SSN and all manner of traditional identifiers have been compromised and are floating around the dark web, biometrics is the cure-all. Biometrics May Not Be the Panacea.

Action: Using analytics-based decisioning and rules-driven workflow automation , banks can trigger holding periods for payments above a specific threshold (such as those exceeding a percentage of the available balance) to allow customers to reconsider, or for further fraud investigation. What About Declining High-Risk Payments Outright?

Rise in Fraud & Delinquency – Fraudulent activities, including identitytheft and misuse of loan funds, significantly threaten the financial stability of both microfinance institutions (MFIs) and their clients. This lack of transparency can lead to inefficiencies, delayed repayments, or even defaults.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content