This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As money moves between banks, consumers, businesses and beyond in a complex cycle, credit and debit cards continue to play a leading role in the payment experience, said Chris Como, Head of Cards and Money Movement at FIS.

This integration provides users with an unprecedented payment experience, allowing faster and safer transactions while redefining how Colombians shop. In a country where mobile payment growth is projected at 22% annually, adopting solutions like Google Pay is essential to meet market demand. billion by 2025, compared to $59.74

What’s more, financial barriers continue to impact quality of life for people globally. Describe how Almond FinTech ensures the affordability of cross-border transactions for end-users. Almond’s SOE puts end-users at the core of our mission. Let’s dive in. One-third of adults don’t have access to a bank.

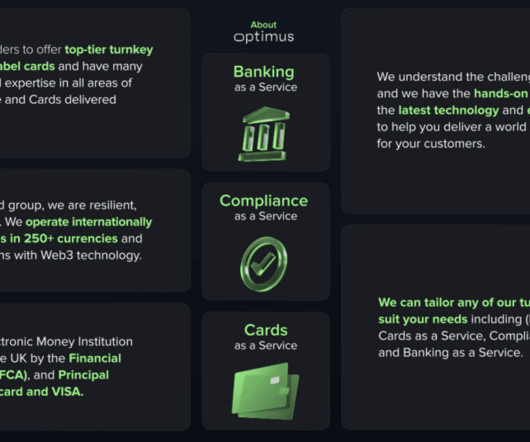

Virtual account and IBAN issuance: Recognising the growing demand for digital payment solutions, Optimus provides businesses with the tools to create and manage virtual accounts for their customers. Optimus’s solution enables corporate and retail end-users to send payments utilising local banking rails.

Think your customers will pay more for data visualizations in your application? Five years ago they may have. But today, dashboards and visualizations have become table stakes. Discover which features will differentiate your application and maximize the ROI of your embedded analytics. Brought to you by Logi Analytics.

Currently, large enterprises are the primary users, while small businesses and consumers have shown limited adoptionlikely due to unclear policies on customer eligibility and risk exposure. Strengthening KYC procedures is critical, ensuring that verification extends beyond master account holders to individual vIBAN endusers.

Undoubtedly, fintech and payments will continue to serve as pivotal forces shaping the financial landscape, but what trends will define the market next year? Jeff Parker, CEO, says, “Digital payments will continue to grow rapidly, with mobile wallets expected to reach 4.8

Therefore, the adoption of solutions like Google Pay is a must for organisations to stay competitive and meet market demands. This system allows a payment token to be sent to the user’s device, which is then converted into card information before communicating with the bank.

One thing is certain: The seismic shifts have shone a spotlight on the fact that cash (and even plastic cards) has seen – and will continue to see – dwindling use. To get there, according to some of the executives we queried, agility is key, and responding to endusers’ demands will be paramount.

Why do some embedded analytics projects succeed while others fail? We surveyed 500+ application teams embedding analytics to find out which analytics features actually move the needle. Read the 6th annual State of Embedded Analytics Report to discover new best practices. Brought to you by Logi Analytics.

By enabling Fedwire transfers, Galileo is helping fintechs capitalize on this growth, with a scalable solution that caters to the increasing demand for rapid financial transactions. ” Enabling wire capabilities benefit endusers in several ways: Fast Transactions: Recipients receive their funds on the same day they’re sent.

To realise the true potential of virtual cards, payment giant Mastercard is launching a new programme that will help banks, platform partners, and mutual end corporate customers transform their commercial payment offerings , powered by Mastercard’s Virtual Card Number (VCN) technology.

That is to say, mass adoption will take time, and the factors driving that adoption will almost certainly continue to change and shift as endusers’ needs do the same. Among corporates, there is an increasing demand that their global payment activity is able to keep up with the pace of doing business.

In financial services, demand for ease of use and security are sky-high, even for business customers. Regulatory mandates “seem to update every year,” he added, meaning service providers will continue to have to stay on their toes to keep security and compliance at the center of their cloud migration and digitization initiatives.

The concept of embedded banking has opened up a new frontier for financial service providers to drive holistic, elevated experiences for end-users. What we’ve seen is an increasing demand from corporates to not have to do it themselves.”. Such functionality can drive retention for a firm’s own end-users, she said.

While FinTech innovators continue to drive competition with a focus on product functionality and an optimal enduser experience, businesses are often forced to use outdated tools, according to Frank Dux , managing director of CoCoNet. The Drive To Upgrade. Connectivity Is Key.

The global nature of its business required G2A.COM to scale its fraud prevention and payments program to meet growing demand. Forter’s technology uses the speed and sophistication of AI to detect patterns across vast datasets and the savvy of fraud experts to continuously update its models.

While this strategy can yield results, it can also create silos, hampering a bank’s ability to achieve one of the most vital goals of DX: seamless integration of operations that boost efficiency and improve the end-user experience. “Banks are technology companies,” Rio Tinto recently told PYMNTS.

Daily use of mobile payment platforms is becoming increasingly common, with users citing the security, reliability and convenience of digital solutions as core driving factors. “As familiarity and understanding of NFC continues to grow, so too does demand for additional applications and use cases for the technology.

This is part of Swiss4’s recently launched application that combines financial services and high-end lifestyle management, the first of its kind in Switzerland. With Marqeta’s platform, Swiss4 can swiftly design and introduce novel payment features, continually enhancing the enduser experience.

Ongoing Maintenance: Continuous updates and support require dedicated resources. He says: “A lot of smaller companies can end up overspending by thinking they need enterprise-scale solutions. This urgency often leads organisations to choose vendors who claim to deploy solutions swiftly to meet compliance demands.

Devices and end-user computing emerged as the second most important investment priority for the finance sector, with over a third (36 per cent) of respondents planning to invest in this area in 2024.

Consumers keep demanding a better, more convenient, seamless, secure user experience that makes their lives better. Instant payments are critical to fully delivering on that enduser experience, she noted. The Road Ahead. have disappeared from public life.

Service providers are increasingly understanding that, like consumers, businesses demand a better and more seamless end-user experience. The higher the level of anti-fraud risk you build into your transaction monitoring rules and into your platform, the more clunky the system becomes for endusers,” he continued.

These exceptions can be linked to changes in weather, customer demand, and other logistical risks that impact where and when deliveries occur. Continuous Data. Supply chain management has always presented a challenge for global corporates, with digitization and automation technology aiming to reduce friction and enhance visibility.

Rapid globalisation and available technological advancements have spurred the demand for more efficient, transparent, and accessible cross-border payment systems. Balancing incentives between sending and receiving jurisdictions is crucial, and costs should not be passed solely to the end-user.

That includes Payments-as-a-Service (PaaS) in which providers help enterprises accept a range of transactions from their end customers — whether those endusers (the ones actually paying and getting paid) are consumers or corporates. Flexibility Is Key. Technology brings the concept of flexible payments into reality.

Companies can capitalize on: Subscription-based integrations , where users pay extra for advanced functionalities. Through Stax Connect , the API enables the software company the ability to offer their users a more complete, all-in-one solution. And it goes even further as the API can integrate with other solutions.

Effective next month, joint customers who continue to use Gusto for payroll will need to manually enter information the API does not support, such as banking and tax details.” ” Gusto, on the other hand, said its decision to request changes on Zenefits’ end stems from security issues.

To that end, in an interview with PYMNTS, Vincent Caldeira , chief technologist, Financial Services, APAC at Red Hat , said that moving to the digital age will require banks to renovate their suite of core banking functions (checking and savings, for example) by moving to the cloud — and to microservices in particular.

SaaS companies deliver software applications over the internet on a subscription basis, simplifying access and management for users. ISVs, or Independent Software Vendors, are businesses that develop and distribute software products to end-users. Primarily through direct-to-user subscriptions and third-party distributors.

According to the publication, Foursquare has the data of more than 12 billion user check-ins on its platform that it extends to 125,000 businesses that use that location information. Foursquare began strengthening its B2B services in 2015 following partnerships with Twitter and Microsoft as demand for Big Data increased.

These legacy methods falter under high demand and diverse consumer preferences, leading to an 8% churn due to card expirations and insufficient funds, with an additional 12% of setups failing from manual entry errors. Trustly’s new solution taps into the growing subscription market, projected to reach $1.5

Volt will power Sumsubs Penny Drop Verification flow, which involves an enduser being directed to their banking app after scanning their identity document. Rozenfeld will drive AlphaSense’s continued growth as am AI-first engineering organisation and will report to CEO and founder, Jack Kokko.

Consumers demand easy, digital banking, but this pressure for banks to deliver is also coming from corporate clients. Take mobile banking, which has propelled the introduction of mobile-only banks to meet demand for better services on smaller screens. Analysts say the tangible benefits of digitization and a happier enduser are clear.

And he said the opportunity surrounding cross-border real-time payments (RTP) will have the most significant impact on end-users due to the “potential implications” for changing how the FinTech conducts business. And Praeger says veteran players in the FinTech space will continue to grow this year. Blockchain.

Banking as a Service (BaaS) is poised to change the enduser experience of corporates as they navigate the daily challenges of cash flow management, supply chain activity and the need to become digital-first. So far, corporate banking users are always left out in the cold.” They’re out there; they just have to be used.”.

Small and medium-sized businesses can be fickle when it comes to adopting new technologies, for instance, or SMEs can feel hesitant to adopt emerging solutions, like on-demand services. Though, according to experts, it’s not the cloud service that’s usually to blame for data breaches; it’s the enduser.

Here are six practical ways to optimize the experience, boost adoption, and drive more valuefor both your users and your business. Native packages with integrated payments are a great way to provide an easy, seamless user experience and controlled payment processing to your software users. Heres how to select the best provider.

The fallout from the global pandemic occurred almost overnight for organizations, which were suddenly struggling to ensure business continuity as professionals worked from home. And we’ve seen incredible demand for integrated receivables and more advanced receivables automation as a result of this.” A Gradual Process.

Brands and their manufacturers today continue to rely on legacy technologies and manual processes to sell products online, said King. Today, paper checks continue to be the dominant form of B2B payment. "The core difference between B2B and B2C is that in B2B, the individual researching and buying has a job to do,” King said.

” At the same time, ongoing shifts in customer expectations and demands mean that addressing the underbanked does not necessarily mean having to build more physical bank locations. He added that open banking appears to be an “inevitability” as the broader financial services market continues to innovate worldwide.

We'll give an overview of its features, AI integrations, and user feedback on how effective it is. It allows users to contextualize real-time performance data and predict future outcomes, facilitating quicker and more confident decision-making. Pros and Cons Based on Users’ Reviews Pros Gaining 4.6 Let's get started.

“This trend suggests that the coming months may serve as a wakeup call for many payment intermediaries, as embedded finance threatens to disrupt traditional roles, potentially leading to the obsolescence of third-party intermediaries and consequent cost reductions for endusers.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content