This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Webinar The final countdown: What’s next for Verification of Payee? The Verification of Payee (VOP) deadline is just around the corner. Could VoP become the global standard for payee verification, similar to how GDPR reshaped data privacy? VOP will become a requirement across the SEPA region on 9 October 2025.

It even allows contributions from friends or family members towards bills, and accepts multiple payees for a single payment, enabling flexibility for houses of multiple occupancy, such as student accommodation. This is particularly beneficial in improving trust between parties and minimizing the risk of fraud.

Card payment clearing: Facilitates credit and debit card transactions by ensuring funds are transferred from the payers bank to the payees account. ACH networks process transactions in batches, making them cost-effective and suitable for high volumes. These systems are critical for large-value transactions.

The Bank for International Settlements (BIS) defines offline payments as the transfer of a digital money token between devices that takes place without the payer and payee requiring a networked connection to any ledger system or backend system to complete the payment. G+D Filia® Unplugged makes digital offline transactions a reality.

It even allows contributions from friends or family members towards bills, and accepts multiple payees for a single payment, enabling flexibility for Houses of Multiple Occupancy, such as student accommodation. This is particularly beneficial in improving trust between parties and minimizing the risk of fraud.

However, with so much sensitive information being transferred with each transaction, the need to keep the datasecure has never been greater. In the new Smarter Payments Tracker , PYMNTS explores the latest efforts by banks and businesses to keep payments datasecure from fraudsters, cybercriminals and other bad actors.

Business consultancy CGI has announced a collaboration with invoice payments FinTech Ordo to develop a service that combats fraud for both payers and payees. A key focus of the collaboration is fraud and datasecurity, the firms noted. CGI and Ordo are focusing on transparency throughout the invoice payment process.

The intent of the organization is to help payers better identify [the] payee information they need in order to make electronic payments,” he said in an interview, adding that the directory aims to be “payment agnostic” and support payments made via a variety of rails, including FedWire, ACH, SWIFT, lockbox and, yes, paper check. “The

Clear Junction has a growing reputation for ensuring the highest adherence to regulatory compliance obligations and datasecurity standards. Clear Junction implemented its Confirmation of Payee (CoP) a year ahead of the mandated deadline to boost payment security and minimise fraud risk for its clients and their customers.

This request includes data such as the payment amount, payee information, and payment due date. Transmission: The payment request is transmitted electronically to the payee's system via EDI. Receipt: Once the payment request is received by the payee's system, it is verified to ensure accuracy and completeness.

The bank recently debuted “Siri for Westpac,” a new feature designed for consumers to link bank accounts to their iPhone or other Apple devices and make payments to payees at any bank. Westpac , one of Australia’s “Big Four” FIs, for one, is rolling out new omnichannel banking offerings.

“In addition, AI-driven risk management will continue improving datasecurity and reduce the possibility of fraudulent attacks on merchants in the coming years.”

Where the rubber hits the road — in terms of executing those ideas — is when the plans to switch to an instant payments paradigm are taken to those enforcing compliance and risk, she said, and when firms start taking a real look at how they can get instant payments up and running as an option safely and securely. .

In the last year, it has launched Confirmation of Payee (CoP) to verify account users, and achieved the globally recognised ISO27001 datasecurity standard, the highest standard for information security.

Merchant accounts provide a secure channel for handling sensitive financial information, such as cardholder data, in compliance with industry standards like the Payment Card Industry DataSecurity Standard (PCI DSS). Cash registers and bill counters may also be required if your business handles cash.

These include advanced datasecurity and new state and federal regulations governing payout mechanisms – to say nothing of the irrevocable nature of instant payments. You can’t pull them back. That will play out as optionality, and payers are starting to think about what those options will be.

For small companies, that includes issues surrounding logistics, datasecurity and protection, and the ability of these factors to coordinate with the actual payment itself.

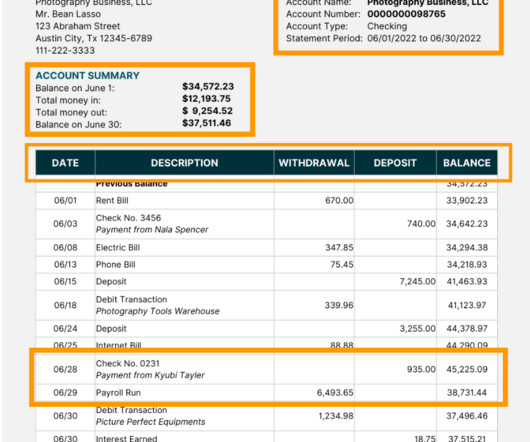

Different bank statements Bank statement processing is extracting and analyzing financial data on bank statements. It involves extracting key details from bank statements, such as transaction amounts, dates, descriptions, account balances, payee names, account numbers, and transaction types (e.g.,

This would take them to the gateway where they can pay by credit card, Paypal, or other payment options the payee wishes to add. Security and compliance Ensure that the payments platform prioritizes security and compliance with industry standards such as PCI DSS (Payment Card Industry DataSecurity Standard).

The payment process using ACH transfers involves the payee creating a payment order which is received by the originator bank. One of the most common methods of automated payment systems is ACH transfers. The originator bank compiles all the POs and sends them to an ACH for processing.

Quickbooks Online trial on a receipt What we liked Multiple optional fields like Payee, Customer, Location, Ref no, etc. Datasecurity and compliance: Ensure the app protects your sensitive financial data with robust security measures.

Blockchain could be used to create a more direct payment flow that connects payers and payees — across borders or domestically — without intermediaries, at ultra-low fees and almost instant speed. Gem is using Ethereum blockchain-enabled technology to create a secure, universal data-sharing infrastructure for the space.)

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content