This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If youre a software provider looking to boost revenue, streamline operations, and deliver more value to your users, ISV integratedpayments can be a game-changer. Embedding payments directly into your platform can unlock tremendous benefits both for you and your users. The best part?

For companies looking to scale, Independent Software Vendors (ISV) are a crucial tool that provides specialized software solutions that integrate seamlessly with existing business tools. ISV integrations offer numerous advantages, from improved functionality to a superior customer experience. The Benefits of ISV Integrations 1.

As the global demand for faster, more affordable, and increasingly transparent cross-border payments intensifies, Project Nexus is emerging as a foundational initiative to meet the G20’s ambitious roadmap. Eli Shoshani Eli Shoshani is Head of APAC at Bottomline , a leader in global business payments with extensive expertise in the region.

Payments company Thunes announced today it has raised US$150 million in its Series D funding round, the largest in the company’s history. The round was led by private equity firms Apis Partners and Vitruvian Partners. said Floris de Kort, CEO of Thunes.

Supply chain finance fintech Taulia partnered with Lloyds to embed Visa-enabled Virtual Cards into SAP Business Suite solutions, streamlining supplier payments. Businesses using Taulia’s platform will be able to issue virtual cards globally through Lloyds, enhancing automation, cash flow visibility, and payment efficiency.

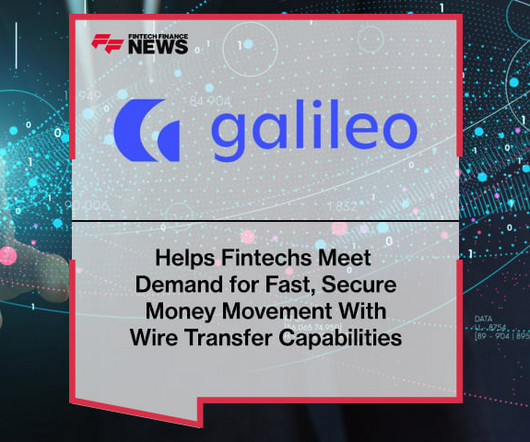

Galileo Financial Technologies , a leading financial technology company owned by SoFi Technologies, Inc. Through its wire transfer API, Galileo connects fintechs partnering with Community Federal Savings Bank (“CFSB”) with Fedwire via sponsor bank CFSB.

Swift drives global interoperability and innovation, aligning with the UK’s National Payments Vision to enhance seamless, secure payments. The UKs payments landscape is at an inflexion point.

From an acronym known mostly by programmers in the early 2000s to something thousands of innovators have embraced to ignite numerous innovative solutions, it’s been an electric journey for the application program interface (API). The API hype cycle has all but ignored what it takes to use APIs,” David Koch noted. Two To Tango.

Cross River Bank (“Cross River”), a technology infrastructure provider that offers embedded finance solutions, announced the launch of Request for Payment (RfP), a transformative addition to its growing suite of instant payment capabilities. RfP is a smarter, more flexible way to receive incoming funds.

Offline settlements with a digital pound: Lessons from the BoE’s report 16 June 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? A Bank of England experiment proving that offline payments with a digital pound are technically feasible, but complex. Why is it important? What’s next?

marked its third anniversary of adopting its open banking framework, making it the leading market to drive the concept of unlocking customers’ bank account data for integration with third-party solution providers. to bring its blockchain-powered corporate trade financing technology into the entity. Last week, the U.K.

The acquisition brings together two major players in API-based financial innovation, aligning with Fabrick’s broader mission to enable embedded finance across the region. The convergence between Fabrick and finAPI aims to improve customer experience in payments and access to financial data, making it increasingly secure, fast, and reliable.

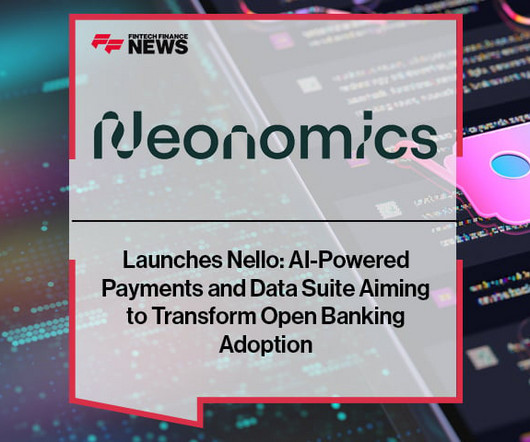

A pioneer in open banking, Neonomics unveils an innovative new product suite launched as Nello, with the goal to bring open banking to the next level through AI-driven solutions and seamless payments. Nello AI will be available as a white-label integration for financial institutions and others to easily integrate.

Conferma , the leading virtual card provider, has entered into a strategic partnership with the ground transportation automation and management platform, GroundSpan to facilitate simple, virtual payments for ground transportation. The strategic partnership was formed in direct response to customer demand for ground transportation integration.

These days, with the emergence of the cloud, open banking and application programming interfaces (APIs, the moniker “as-a-Service” applies to pretty much any business function that is now able to be outsourced to a third party. Technology brings the concept of flexible payments into reality. Flexibility Is Key.

No longer is open banking solely for consolidating financial information into a single platform for one enduser. Enterprise resource planning (ERP) technology provider Acumatica is embracing bank connectivity with the launch of its newest offering, Acumatica Advanced Expense Management and Electronic Bank Feeds. In the U.K.,

The capabilities to unlock bank data and integrate new services into emerging FinTech platforms via APIintegrations is a FinTech trend that hasn’t ignored the B2B payments arena. Service providers are increasingly understanding that, like consumers, businesses demand a better and more seamless end-user experience.

According to Convictional Co-Founder and Chief Operating Officer Chris Grouchy , this is the crux of the problem of a lack of eCommerce technology adoption. What it comes down to is a lack of integration and automation on both sides of the transaction.”. APIintegrations can address a range of problems. he explained.

For all of the innovation that's occurred in the banking landscape, it's often consumers – not corporates – that benefit from the latest technologies. As Dux explained, FinTechs have enabled banks to ease the "build-versus-buy" debate and more easily access tools that can be integrated into the back office. ""It The Drive To Upgrade.

Foreign exchange solutions company OANDA is enhancing its application programming interface (API) that opens up its foreign exchange (FX) technology to third-party apps. The company announced news on Thursday (March 8) that its Exchange Rates API has been updated to include real-time FX rates.

In a major leap for subscription services, Trustly , the global leader in open banking payments, today unveiled its innovative AI-powered recurring payments solution poised to revolutionise how merchants handle repeat transactions through a single integration.

Artificial intelligence (AI) can improve the eCommerce experience – not just in terms of warding off fraud, but also in making sure payments can be processed efficiently and that the most effective payment gateways are accessed. Consider the fact that just a few years ago, alternative payment rails Zelle and Venmo didn’t even exist.

In the journey to improve the payments experience, sometimes the best user experience (UX) is an unnoticeable one. Key to achieving this goal is data integration, yet in markets where open banking frameworks aren't as advanced as jurisdictions like the U.K., A Better Payments Experience. Making Payments Invisible.

The conversation delved into the transformation journey of Currencycloud into Visa Cross-Border Solutions , a foreign exchange and cross-border payments solution within Visa, and how it addresses the challenges of cross-border payments in today’s fintech landscape.

Considering the mind-bending level of competition in the FinTech space today, the rise of the API may raise some eyebrows. After all, if a company has worked so hard to develop some type of financial technology, why would they want to lend that technology out to just about anyone?

The acquisition of Property Monitor reinforces Dubizzle Groups leadership in real estate classifieds and technology through a portfolio of brands, including Bayut and dubizzle. Appointments GoCardless , the bank payment company, has announced the appointment of Shaun Puckrin as chief product officer.

In today’s ever-evolving digital landscape, integratedpayment processing has emerged as a key to business success. Whether you’re running an e-commerce platform, a cutting-edge software-as-a-service (SaaS) solution, or any digital enterprise, choosing the right integratedpayment provider is paramount.

Embedded versus integratedpayments: what exactly is the difference? Are these two payment models actually one in the same? Keep reading as we explain the key differences between embedded and integratedpayments. However, there are variations in each integration approach. of integratedpayments.

October 7th 2025 15:00 BST | 16:00 CEST | 10:00 EDT Online Join this Webinar Why have banks’ priorities shifted from core modernisation to ensuring end-to-end bank modernisation? How can banks update their approach to APIs, digital experiences, data insights, and the wider banking platform?

When it comes to payments in commerce, what — and who — you don’t know can hurt you. For software companies and platforms that seek to integratepayments and provide value-added services to merchants, there is the never-ending challenge of balancing trust and risk. Risks for Merchants — and Providers. The Partnerships.

The concept of embedded banking has opened up a new frontier for financial service providers to drive holistic, elevated experiences for end-users. But the continued evolution of FinTech has made integration far more accessible, and today, it’s up to those FinTech providers to facilitate connectivity.

This week's look at the latest in bank-FinTech collaborations explores how a range of banks is turning to partners and API connectivity to enhance small business services, from lending to payments. Also focused on unlocking bank data is Visa, which recently announced a partnership with API provider Codat in Europe.

million in a funding round to go toward the startup's goal of providing a way for third parties to integrate banking services through an application programming interface (API), according to a report from TechCrunch. Unit has raised $18.6

FinTech still exists as a fragmented market, where businesses striving to offer payment services to endusers pick and choose among providers, integrate with those providers, and must often navigate across complex technological and regulatory hurdles as they expand into new markets. The Transition In Payments, Too.

Finally, looking at Canadian “fintech” (financial technology) specifically, funding was up substantially in the first half of the year. Canadian fintech companies raised $251M through the end of H1’19, nearly double the $133M raised in H1’18. APIs) directly to end-users. Company subcategories.

As these ecosystems evolve, ISV partnerships have become essential for companies looking to scale, reach new markets, and offer integrated ISV solutions. AWS, Microsoft, Salesforce) to integrate, co-market, and grow together. AWS, Microsoft, Salesforce) to integrate, co-market, and grow together.

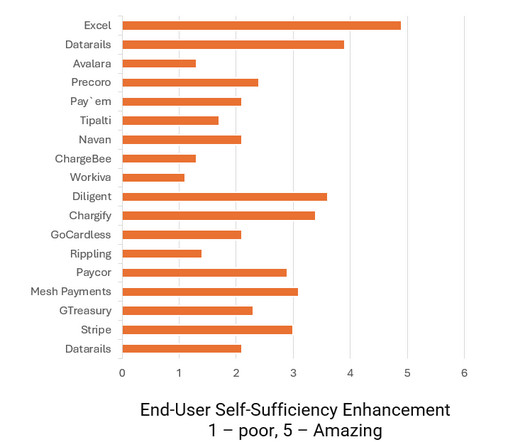

Question 1: End-User Self-Sufficiency Enhancement Which software has been most effective in transforming end-users to be more self-sufficient, resulting in a reduction of tickets opened with the IT helpdesk? This question was tricky, and we were eager to see the results.

New research says businesses are eager to make the leap into real-time payments (RTP) — and to embrace new payment rails in their effort. A new survey from Citizens Bank says businesses are jumping into the real-time payments opportunity. Faster Payments Council Announces Board Advisory Group. This week, the U.S.

Understanding the VAR Sheet Consider the VAR Sheet as a vital handbook for payment processing setup. It is a comprehensive document containing the necessary details and configurations that payment processors use to accurately prepare a merchant’s system for accepting payments. When is a VAR Sheet Unnecessary?

These days, with the emergence of the cloud, open banking and application programming interfaces (APIs, the moniker “as-a-Service” applies to pretty much any business function that is now able to be outsourced to a third party. Technology brings the concept of flexible payments into reality. Flexibility is Key.

Visa introduced a platform on Monday morning (April 22), complete with beta application programming interfaces (APIs), that will allow issuers and issuer processors to build and test new products. The initial beta APIs on offer will help those within the Visa ecosystem to create digital cards on demand and add digital services.

It may be an open road for open banking as, three years after the rollout of the second Payment Services Directive (PSD2), bank-FinTech collaborations and new initiatives unlocking bank account data continue to flourish. But it may not always be smooth sailing ahead. ThinCats Links Up With Open Banking FinTech Salt Edge. In the U.K.,

That means financial functions beyond banking are taking advantage of application programming interface (API) data integrations, with productivity gains particularly large for business end-users of these products and services. Unlocking Data, Unlocking Opportunities.

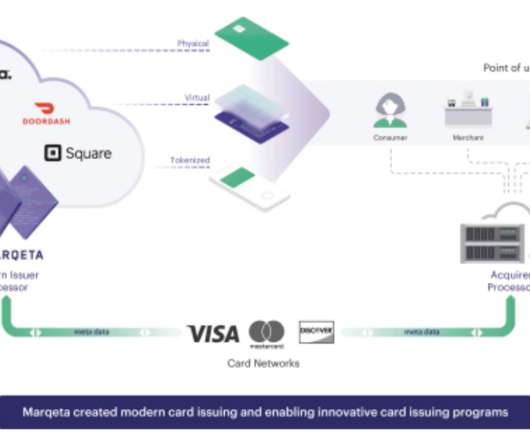

Marqeta , a cloud-based open API platform for modern card issuing and transaction processing, recently filed its S-1 in preparation for its shares to start trading publicly in June. Marqeta allows businesses to offer payment card products to customers without having to deal directly with a traditional bank. First name. Company Name.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content