This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Real-Time Payments (RTP) & Instant Payments Overview : Real-Time Payments (RTP) systems allow funds to transfer instantly between bank accounts, offering 24/7 availability, even outside standard banking hours. Usage : RTP systems are growing rapidly; India’s UPI processed 74 billion transactions in 2023, while Zelle in the U.S.

The results reflect growing adoption of the FedNow Service and RTP Network and an expanding array of use cases in both consumer and business contexts. Meanwhile, financial institutions are prioritizing P2P payments (51%), bill pay (38%), and payroll (38%).

The two companies signed a new multi-year agreement, which will power PromptPay, the region’s RTP platform, to help develop Thailand’s growing digital economy. Thai consumers can utilise PromptPay for shopping, receiving government welfare and tax rebates, and fast P2P transactions.

Real-time payments (RTP) could reach $193.1 .” Merusha Naidu, global head of partnerships , says, “Global cashless payment volumes are projected to increase by more than 80% between 2020 and 2025, from about 1 trillion transactions to almost 1.9 trillion, and to almost triple by 2030.

Its fair to say that traditional financial systems left many people and communities underserved, but LPMsfrom mobile wallets in Africa to RTP schemes like UPI in Indiabridge this gap, and theyre empowering billions of consumers to participate in the digital economy. And thats a really positive development.

Similarly, a record 98 million transactions were made through The Clearing House (TCH-RTP) network in Q4 2024 [3]. In addition to mitigating fraud, this would also enable banks to compete with the likes of Venmo and PayPal in facilitating mobile, peer-to-peer (P2P) payments. million transactions settled in the same period [2].

Emergence of SWIFT & RTP: The 1980s–1990s saw global messaging standards (MT-103, MT-202) and real-time rails (Fedwire, TARGET2) democratize cross-border settlement but reliance on intermediaries, queue times, and compliance checks remained major pain points.

Its purpose is to enable instant money transfers between banks and other financial institutions, but there are person-to-person (P2P) elements as well. If FedNow is offered by a customer’s bank as a P2P option to pay someone immediately (similar to Venmo or PayPal) the customer will need to have those funds available.

The rise of Zelle , and any number of peer-to-peer (P2P) payment options, has increasingly brought consumers on board with the need for speed in payments — where settlement is marked by seconds and minutes, not hours or days. The Clearing House [TCH] launched its own RTP network at the end of 2017.). RTP And RFP.

Consumers have meanwhile transitioned even more toward payment solutions that allow them to send or receive money in real time, with P2P apps like Zelle and Venmo reporting jumps in user activity during the first half of 2020. Payment frictions and P2P’s impact. now have access to such payments via the RTP® network, for example.

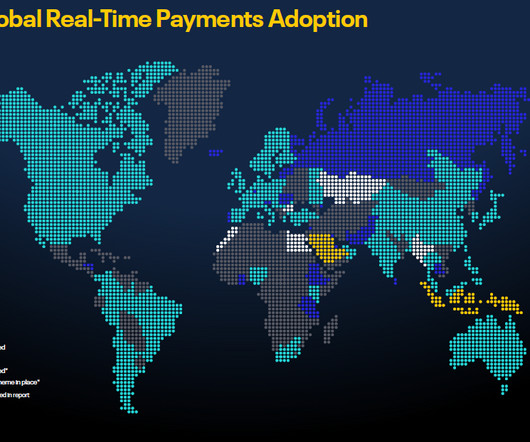

Introduction on RTP and its adoption around the world. While real-time payments (RTP) was previously considered an infrastructure luxury, it has now become a common method of payment in many parts of the world. Digital and RTP payments have dramatically accelerated the pre-existing, but slow-moving trend, away from cash and checks.

This interest notably appears to be translating into action as more than 85 percent of firms are either in the process of implementing RTP or expect to do so within the next three years. RTP is particularly relevant in the current climate. PYMNTS research from January found that 66.7 A November survey from PYMNTS showed that 44.7

The appetite for new payments approaches is only growing, with The Clearing House (TCH) reporting that 400 more FIs have already gained technical access to the RTP network.”. RTP Doing Its Part for a Quicker Recovery. There’s no shortage of interest or activity as more FIs begin offering and promoting RTP.

Ranta said RTP is already past the “early adopter” stage and moving into the “fast follower” phase of its evolution. After all, The Clearing House’s RTP infrastructure is already up and running. And beyond TCH and RTP, the Federal Reserve’s FedNow real-time payments solution looms. 2021 Could Be The Game-Changer .

FIS® (NYSE: FIS), a global leader in financial technology, today announced that it is unlocking the Neural Payments solution to its clients, expanding the availability of peer-to-peer (P2P) payments by leveraging the company’s global scale and NYCE debit rails to bring this capability to a wider range of institutions.

Offerings like the Real-Time Payments® (RTP) network are drawing attention from bad actors as well. Customers tapping into digital channels to buy their new vehicles also want their auto financing loans to arrive quickly, which is pushing some lenders to adopt RTP® to speed along those disbursements. Check out the story in the Tracker.

Peer-to-peer (P2P) payments are blazing a hotter path in the digital economy as the second half of 2019 gets underway – and there is fresh evidence that the payment method is not only growing, but helping to influence related endeavors. Venmo, of course, is not the only major P2P player in the game. Larger P2P World.

As real-time payments (RTP) gain traction with consumers via peer-to-peer (P2P), the pump may be primed for business-to-business (B2B) transactions to follow suit. Key among those conduits, of course, is the Clearinghouse RTP network, where commercial real-time payments made their debut in the U.S. roughly two years ago.

Peer-to-peer (P2P) payment apps have become particularly appealing to consumers during the COVID-19 pandemic, with P2P app Zelle reporting rises in the number of transactions and transactions’ values in recent months. PYMNTS’ data revealed that many consumers are now seeking real-time access to their funds, with 35.2

The Clearing House ’s (TCH) Real-Time Payments (RTP) network received multiple shows of support from B2B FinTechs this week as service providers embrace the U.S.’s But RTP isn’t the only novel network to gain traction in the small business in corporate realm. Finxact Enables Banks’ RTP Product Development.

When people began experiencing the joy of instant peer-to-peer (P2P) payments a few short years ago, the genie was out of the bottle. Now, the major real-time payments (RTP) players are ready to push the button on real-time, all the time, redefining fast money and revolutionizing multiple aspects of the commercial biome.

Working with Real-Time Payments (RTP) networks around the world, we are overlaying decades of Visa expertise in applying AI to help mitigate fraud for account-to-account payments on RTP networks.

The Clearing House is working to add its Real-Time Payments (RTP) network as a third payment rail for Early Warning Services’ Zelle P2P payments service and to enable Zelle bill pay and possibly point of sale transactions.

Cross River, a company that provides banking services for technology companies, will join The Clearing House’s (TCH) RTP network, according to a release. By joining the network, Cross River will be able to give its clients the ability to send, settle and clear payments instantly, along with messaging capabilities, while ensuring compliance.

As such, the consequences of real-time payments aren’t solely impacting consumers’ peer-to-peer ( P2P ) transaction activity. It works OK, but it’s not nearly as slick as it will be with the RTP network.”. Today, we put that information in bank-to-bank wire instructions.

This new feature, available to PayPal customers in good standing, leverages the company’s partnership with Chase, and Chase’s connection to The Clearing House’s RTP network, to move money instantly into the bank accounts of consumers and SMBs. On its website, TCH also says RTP is the system that “all federally insured U.S.

The company recently became the first such provider to integrate with TCH’s RTP® network, which offers businesses and employees quick access to these funds through their FIs. I do it all the time [with P2P apps].’”. P2P, the pandemic and on-demand payroll. The vast majority of U.S. What is the difference?

Real-time payments (RTP) methods aren’t much use if few people understand what they are, where to find them and how to use them. The fact is that people love the idea of RTP — once they understand it — and “consumers are even willing to pay fees to ensure that recipients can access funds quickly and seamlessly. Consumerizing RTP.

Demand for instant and peer-to-peer (P2P) payments is heating up, and financial institutions (FIs) are seeking to cater to that need, knowing that if they don’t, their customers are likely to turn elsewhere. Dee p Dive: How RTP Has Changed the Bill Payments Game. it’s not just P2P seeing a rise in demand for instant payments.

There will be self-service portals for end-to-end payments, and simpler applications for mobile payments that include Request to Pay (RtP) services. And, there will be flexible person-to-person (P2P) services with added layers of security authorizations.

We are also seeing that certainly RTP is playing a bigger role, though clearly that’s not a ubiquitous option at this point for small businesses unless they have relationships with larger financial institutions,” McFarland said.

MUFG Union Bank is now offering business customers real-time payments on The Clearing House (TCH) RTP network, MUFG announced on Thursday (Jan. The RTP network provides instantaneous payments that allow customers the convenience of using funds right away. The RTP network is the first payments framework created in the U.S.

Peer-to-peer (P2P) and voice assistant payment capabilities are poised to become important areas of CU innovation in the near future, with 55 percent and 66 percent of credit union executives saying they are ‘very’ or ‘extremely interested’ in focusing on them, respectively,” the report states. “ RTP, P2P and the People Who Love Them.

Just ask the folks at Zelle, whose P2P network via their bank accounts is really awesome if the sender’s and receiver’s banks are connected to the network – and not so awesome if they’re not. TCH cleared its first RTP transaction on November 14, 2017. Banks also know that unless such a network is ubiquitous, it’s not worth much.

Instant ACH Transfer Alternatives RTP Network The RTP (Real-Time Payments) Network, launched by The Clearing House, is an alternative option for those seeking instant money transfers. The RTP Network enables real-time transactions for various use cases, such as B2B and P2P transactions, payroll, and Request for Pay (RfP) services.

HSBC Bank has launched real-time payments capabilities on the RTP network that gives businesses the ability to pay and be paid immediately, the company said in a press release Monday (Nov. This is the latest enhancement of HSBC’s implementation of the RTP network. depository institution on the RTP network. payments industry.

Additionally, as real-time payments (RTP) gain traction, 40 percent of survey respondents feel that accounting and ERP integration is their primary concern with adoption of corporate RTP in the United States.”. Digitize to Actualize. The historic moment hinted at earlier isn’t far off, at least not in relative terms.

Peer-to-peer (P2P) instant money apps and real-time payments (RTP) are the most exciting developments in getting paid in decades, and alternative credit is having the same effect on borrowing.

The platform lets B2B, P2P and other commerce take place over Mexico’s real time gross settlements payments system, known as SPEI (in turn tied to wire transfers) for short. The buyer’s bank validates the transfer. Why Not Just Merge These Things?’.

Significant challenges remain before the benefits of real-time payments (RTP) really start to show themselves. New RTP Rails. They include the rush by “a lot of industry segments” to enable customers and individual consumers to make real-time payments and the ongoing rise of real-time peer-to-peer (P2P) payments. RTP Security.

That’s because that software supports any combination of real-time payment (RTP) events, point-to-point (P2P) application programming interface (API) data exchanges, and traditional batch data. The Challenges Of Multi-Channel Payment Innovation.

Direct deposit volume and person-to-person (P2P) transfers continued a multi-year trend of steady growth. Similarly, the value settled on the RTP® network, the instant payments system also operated by The Clearing House, jumped 94% in 2024, while transaction volume grew 38%. Business-to-business payments increased almost 11.6%

It has clarified the banking processes, but RTP is hardly ubiquitous within Italy, much less across the Eurozone. That increase has been driven by P2P payments, where parents are sending money to their children, and, perhaps not surprisingly, tech-savvy younger demographics are sending money to one another using banking apps.

The company also helps third-party organizations across various industries integrate instant payments with traditional payment tools into their existing payment and money movement use cases including A2A, P2P, Bill Payment, B2B and B2C disbursements. Launching Payfinia will help Tyfone further build on the instant payments experience.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content