This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Mastercard uses many different interchange categories to determine the rates and fees your business pays for accepting credit cards. There isnt just a single Mastercard business interchange rate. Program Level Mastercard splits commercial interchange into 5 levels. Read more about downgrades and Mastercard Standard interchange.

Merchants can, however, negotiate with their payment processor to cut costs, tweak pricing, or secure better rates. Choosing a credit card processor that offers transparent pricing, strong customer support, and top-tier security is the key to lowering processingcosts. You pay this fee for using their payment infrastructure.

Although these fees go to the issuing bank, the rates are set by card networks like Discover, American Express, Visa , and Mastercard. Mastercard debit card transactions – Rates could be approximately 0.50% + $0.22 Working on managing costs related to interchange fees can be beneficial for every business. per transaction.

The research was published in Juniper Research ‘s Global Network Tokenisation Market: 2025-2029 report , and predicts that the growth of network tokens will mean they are better placed to fight fraud, lower processingcosts and streamline checkout experiences for users in the future.

It is currently working with Mastercard to onboard a selection of existing customers into Click to Pay for a more secure and seamless payment process. By implementing Click to Pay, Mastercard estimates that merchants can increase approval rates by as much as 3% and reduce checkout times by up to 50%.

Ecommpay , an end-to-end payments platform, has fully integrated the Click to Pay flow within its online payment interface, in collaboration with Mastercard. This integration aims to enhance security and streamline the payment process for merchants and their customers.

Card Networks Companies like Visa, Mastercard, and American Express ( credit card networks ) that set processing rules and fees. The Costs You Dont See One of the biggest surprises for small businesses is the actual cost of accepting credit and debit cards.

Interchange is the fee that credit card companies like Visa and Mastercard charge businesses to accept their cards. How much does interchange cost? Visa interchange fees Mastercard interchange fees Discover interchange fees American Express interchange (OptBlue) What is the total cost of accepting credit cards?

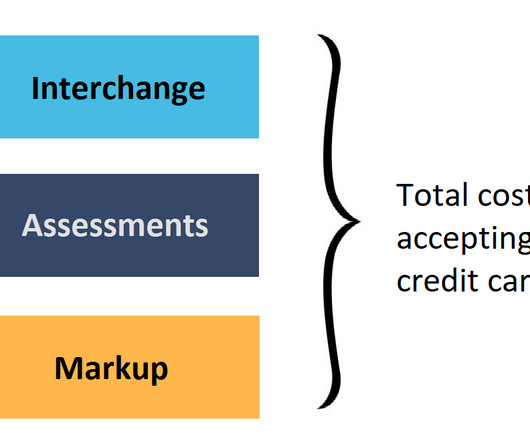

In this article, were going to focus on Visa and Mastercard interchange categories and their effect on your processing fees. But if you just want a quick overview, here it is: Interchange is one of the three core components of credit card processingcosts. Along with assessments and processors markup.)

Think: Visa, Mastercard, American Express, and Discover. Payment processor This refers to the credit card processing company that connects the merchant, card associations, and issuing banks to facilitate payments. This component is a core part of your overall transaction fees and you will see this as a part of your processing fees.

This article explores the legal landscape surrounding surcharges, shedding light on the intricacies of state and federal laws and strategies for small businesses to manage processingcosts. TL;DR Card brands such as Visa and MasterCard along with state and federal laws prohibit debit card surcharging.

As with many things in credit card processing, its complicated. Interchange, as set by Visa and Mastercard, is non-negotiable. It isnt possible to get lower rates or fees than what Visa and Mastercard publish. Costs of Processing Interchange is one of three components of total processingcosts.

Types of payment processing fee structures Interchange plus Interchange plus pricing is one of the most transparent and cost-effective fee structures. It works by passing the actual interchange fee (set by card networks like Visa and Mastercard) directly to you, plus a small markup from the payment processor.

Now citing sources familiar with the matter, The Wall Street Journal reported that the company has met with dozens of potential investors, including Visa and Mastercard, as well as payment processor First Data, to raise funding that would underpin the value of the coin.

Previously called “Cardlite,” the solution will enable BOCHK to enhance the customer experience with new offerings, including its multi-currency Mastercard debit card. The company’s international digital payments network supports more than 145 currencies, and processes billions of transactions a year.

Exactly.coms full-stack payment platform is directly integrated with major global and local payment methods, helping businesses reduce processingcosts and accelerating time to market.

The exact rate can vary based on several factors, including the type of card used (debit or credit), the card brand (Visa, MasterCard, etc.), Viewing these costs individually makes it easier to understand what is contributing to your credit card processingcosts and where you may be able to save money.

Consider payment processingcosts and ensure the provider complies with industry standards like PCI Compliance. Reviewing each providers functionality, payment collection tools, payment security, costs, and customer support will enable your business to make the best decision. and ACH/eChecks for direct bank transfers.

Mastercard states that 2 out of every 3 transactions processed on its network are now contactless, up from less than 1 out of 3 in 2020. Costs to Accept Tap on Phone Tap on phone is considered a card-present transaction and your processor will charge card-present rates. Do all credit card processors offer tap on phone?

Are you struggling with resource constraints caused by soaring credit card processingcosts? TL;DR Credit card surcharging involves adding a fee to transactions with credit card payments, offsetting processingcosts. It offsets the card processingcosts, transferring the financial obligation to the latter.

However, the idea of applying a credit card surcharge to offset the processingcost of credit cards has always been a hotly debated topic. Simply put, a surcharge amount is an extra fee that some merchants choose to levy on customers to cover the costs of processing credit card payments. The rate varies between 1.3

However, the idea of applying a credit card surcharge to offset the processingcost of credit cards has always been a hotly debated topic. Simply put, a surcharge amount is an extra fee that some merchants choose to levy on customers to cover the costs of processing credit card payments. The rate varies between 1.3

Understanding the various credit card processing fees your company may encounter will help you find effective ways to offset them and enhance operational cost efficiency. Here are some of the most common processing fees: Interchange fees are set by credit card networks like Visa and Mastercard.

Merchant: The individual business accepting the payment and in need of credit card processing. Card Association: Visa, Mastercard, American Express, and Discover. Both of these are the only mandatory fees associated with credit card payment processing since they are set by the credit card companies themselves.

North American payment processing fees are the highest in the world due to a combination of factors, including high interchange rates , which can exceed 2% per transaction, and the dominance of major card networks like Visa and Mastercard that control over 80% of the market. Unlike Europe, where interchange fees are capped at 0.3%

They share several key characteristics, including: Cost-effective and reliable digital transactions ACH and EFT both enable direct bank-to-bank transfers, reducing the costs and security issues associated with cash and checks. Checks can get lost without a trace, but electronic transfers leave behind a digital trail.

What are Interchange Fees in Canada Interchange fees are charges levied by credit card issuers (such as Visa, Mastercard, and others) to merchants for accepting and processing electronic payments. These fees serve as compensation for the risks and costs associated with facilitating electronic transactions.

They significantly impact the cost of accepting card payments. Understanding interchange fees enables merchants to effectively manage processingcosts, negotiate better rates, make informed decisions about card acceptance, and ensure compliance with payment industry standards. Can you decrease interchange fees?

Customers who want to use their credit card have to pay an additional fee covering the processingcosts. For anyone new to the term, surcharging is a payment processing option allowing merchants to pass on credit card fees. Customers who want to use their credit card have to pay an additional fee covering the processingcosts.

EMV (Europay, Mastercard, and Visa) chip card use has continued to expand in use since its tumultuous rollout in 2015. This is due to the fact that PIN debit processingcosts are often lower than credit card processingcosts. Q: Are there cost differences when accepting chip and PIN vs. chip and signature cards?

The issuing bank : this is the customers bank that issued the credit card to the customer on behalf of the card networks, such as Visa, American Express, Mastercard, and Discover. The merchant account : this is a special bank account that allows you to accept and process credit and debit card payments.

billion to chargebacks in 2023, according to Mastercard , a number expected to rise as transaction volumes increase. Chargeback abuse doesn’t just affect inventory or revenue; it also results in significant fees, increased processingcosts, and reputational damage. This issue is growing, with merchants losing a staggering $117.47

Visa, Mastercard): The intermediary networks facilitating transactions between acquiring and issuing banks. Payment Gateway: A service provider that facilitates communication between the merchant’s POS system and the acquiring bank’s payment processing system. Card Network (e.g.,

That means if a customer wants to make a credit card purchase, they’ll be charged an additional fee to cover the payment processingcosts. Although surcharging has been widely debated, it’s starting to become something of a mainstay, especially with rising processing fees. Q: What is an example of a credit card surcharge?

Visa, Mastercard, American Express, Discover, etc.) TL;DR Credit card processing fees can add up quickly and eat into a business’s bottom line. Fortunately, in states where surcharging is legal, you can recoup these processingcosts by transferring them to the cardholder. before you can start surcharging.

Credit card networks like Mastercard and Visa set a universal limit of 4% on these fees. Visa and Mastercard explicitly forbid surcharging on debit cards and prepaid cards to maintain consistency in processingcosts. This practice promotes fair and stable pricing and guarantees you retain all your revenue.

One way to do that—though often overlooked—is to optimize their payment processing to reduce fees associated with credit card purchases. Card companies like Visa, Mastercard, Discover, etc. charge interchange fees which, on top of other credit card processing fees, can eat away at your profits.

Understanding Credit Card Processing Fees There are three main components to credit card processing fees. Understanding each of them is critical to learning how to lower credit card processing fees. Interchange Fees This fee is set by credit card issuers like Visa, MasterCard, Discover, and American Express.

For example, most payment gateways accept payments from major credit cards like Visa and Mastercard, but only a small percentage accept Discover and American Express. Some businesses may receive multiple terminals, which helps reduce physical payment processingcosts. How to Evaluate and Compare Payment Gateways Step Details 1.

For businesses looking at paying with a credit card, there are often reward schemes and low-interest rates designed to attract businesses with special B2B credit card solutions offered by Visa, Mastercard, and most other card issuers. Read the section B2B processingcosts below to learn more.)

The PayTech Awards are decided by a panel of judges with extensive expertise in payment technology, including professionals from leading companies such as Mastercard and IBM. These esteemed judges conduct a rigorous and impartial evaluation process to select the most qualified nominee for each category.

This fee compensates for these alternative methods’ higher processingcosts and potential risks. Pros and Cons of Charging Convenience Fees Pros: Offset ProcessingCosts: Convenience fees help you recoup the costs of processing non-standard payment methods. appeared first on My Payment Savvy.

This article explores practical strategies to help businesses lower their credit card payment processingcosts, offering insights to enhance financial efficiency. This proactive approach allows businesses to not only save on processingcosts but also stay ahead in a rapidly changing payment landscape.

Payment network giants such as Visa and Mastercard said in their most recent earnings reports that contactless payments , especially in face-to-face transactions, surged by double digits year over year. Larger merchants have an advantage in multiple areas, including processingcosts, IT resources and distribution.”

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content