This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It could enable self-optimising financial assistants, adaptive credit assessments, and proactive compliance monitoring, making financial services more intelligent, efficient, and inclusive. But these systems still require users to set preferences, approve transactions, or manually adjust settings.

Central to these changes are new statutory trust requirements, more prescriptive record-keeping, reconciliation standards, and the mandate for external safeguarding audits. Safeguarding audits: Firms are required to arrange safeguarding audits to assess compliance with the rules.

This comprehensive assessment identifies any discrepancies between your existing frameworks and the regulatory standards, enabling you to pinpoint areas that require enhancement. Regular reviews and audits ensure your systems and processes stay aligned with regulatory changes. Best practices for implementing the DORA compliance 1.

This comprehensive assessment identifies any discrepancies between your existing frameworks and the regulatory standards, enabling you to pinpoint areas that require enhancement. Regular reviews and audits ensure your systems and processes stay aligned with regulatory changes. Best practices for implementing the DORA compliance 1.

This comprehensive assessment identifies any discrepancies between your existing frameworks and the regulatory standards, enabling you to pinpoint areas that require enhancement. Regular reviews and audits ensure your systems and processes stay aligned with regulatory changes. Best practices for implementing the DORA compliance 1.

This comprehensive assessment identifies any discrepancies between your existing frameworks and the regulatory standards, enabling you to pinpoint areas that require enhancement. Regular reviews and audits ensure your systems and processes stay aligned with regulatory changes. Best practices for implementing the DORA compliance 1.

At Neopay, we offer a range of solutions tailored to firms’ needs as they adjust to the changing attitude of the Regulator. All of our audits draw on the market-leading experience of our team to deliver a detailed and practical report. Regular audits are more important than ever.

assessment, understanding these changes to Requirement 10 will help you strategize your implementation approach. Changes Access Controls "Limit viewing of audit trails" to those with a need. Minor adjustments to testing scope. audit log security principles are mostly unchanged. Maintains the risk assessment step.

The consultation set out proposals for a range of legislative and governance reforms to be implemented in the Code in 2024, including the introduction of a new regulatory body, known as the Audit, Reporting, and Governance Authority (ARGA), which would replace the FRC. A description of company policies for tendering external audit services.

Internal audits play a crucial role in assessing a company's internal controls, corporate governance, and accounting processes. These audits are essential for ensuring compliance with laws and regulations, as well as maintaining accurate and timely financial reporting and data collection.

Step 1: Conduct a Marketing Audit Why Start with an Audit? A marketing audit provides a snapshot of your current position and helps identify areas that need improvement. Key Activities in a Marketing Audit SWOT Analysis: Assess your internal strengths and weaknesses, as well as external opportunities and threats.

Key Proposals in the RBI’s Draft Guidelines Standardized Gold Valuation Lenders must use a transparent and uniform method for valuing pledged gold, with valuation done by certified personnel and subject to periodic audits. Purity checks must be documented and auditable.

Audit Bank Reconciliation Guide Both internal and external accounting audits are essential parts of financial management as well as organizational risk management. A bank reconciliation audit is one such process that helps in identifying financial gaps or discrepancies. Looking out for a Reconciliation Software?

The concern is regarding the period of adjustment and whether this leaves firms exposed to operational and compliance risks, particularly in the absence of established precedents. This will also include verifying the legitimacy of assets, auditing their technical infrastructure, and assessing market risks simultaneously.

Over the years, the auditing landscape has undergone remarkable transformations, and among the most significant advancements has been the advent of audit automation software solutions. Computer-Assisted Audit Tools and Techniques (CAATTs) have been available to auditors since the early 1990s. The situation has changed now.

Audit Trail and Transparency: AI Insurance Claims Processing systems maintain detailed audit trails of all activities within the claims processing workflow. This transparency is essential for regulatory audits, allowing authorities to review the entire process and verify that each step adheres to compliance requirements.

Outdated risk assessments, limited awareness of emerging risks, and failure to adjust processes during operational changes, like customer migrations, left gaps that allowed high-risk transactions to bypass scrutiny. Internal assessments categorised Nordeas overall AML risk as critical, yet systemic upgrades were not prioritised.

Instead, you pay a predictable monthly fee that adjusts based on your specific needs and growth—a much more budget-friendly approach. Regular audits and updates ensure your systems comply with industry regulations, offering you peace of mind and protecting your critical business information.

AdviceRobo has pioneered the use of psychometric data, behavioral analytics, and alternative data to assess risk far beyond FICO scores. Imagine a suite of AdviceRobo agents: One analyzing psychometric data, Another adjusting for behavioral shifts, A third scanning macroeconomic risks. And with response times as fast as 0.03

Firms must prepare for these changes by improving their internal processes, conducting audits, and adapting to new compliance requirements to ensure seamless implementation of the FCA’s reforms. What’s next?

The company aims to eliminate the confusion related to cybersecurity audit and certification processes by assisting companies in scoping correctly-sized audits and dynamically adjusting controls. The new capital will help Strike Graph hire more engineering and cybersecurity positions.

Adjusting to MiCA The MiCA regulation aims to foster the use of innovative technologies by setting a regulatory framework that covers crypto-assets (including stablecoins ), crypto-assets issuers and crypto-asset service providers to protect the rights of holders in the EU.

Identifying and Assessing Risks Understanding the lay of the land is the first step in effective risk management. Conducting a thorough risk assessment tailored to the specific nature of the business is essential. This assessment serves as the groundwork for developing strategies to mitigate these identified risks.

Here are some quick tips to keep you focused on your priorities: Review Risk Assessments and adjust internal controls as needed. Conducting internal monitoring and auditing. Maintain a strong Tone at the Top (“Culture of Compliance”). Set clear and realistic priorities. Exercise caution in dealings with third parties.

It also applies to accounting firms, audit agencies, and any third party that a publicly traded company uses in its accounting management process. The act requires companies to develop, publish, audit, and actively use their ICFR. An assessment of how adequate internal controls were for the preceding period.

It also introduces new self-assessment questions and emphasises the importance of senior management accountability. Proliferation Financing (PF) In response to the 2022 changes in the Money Laundering Regulations (MLRs), the Guide now explicitly addresses the need for firms to conduct PF risk assessments.

In addition to assessing how many members of the C-Suite have accounting experience, the researchers looked at other data points, including executive pay, complexity of company finances, financial performance and more. Newton of Florida State University examined data from 3,252 public companies over a 10-year period.

Annual safeguarding audits conducted by an external auditor, with findings submitted to the FCA. Firms must prepare to: Upgrade systems and processes : Enhanced record-keeping and reconciliation will require operational adjustments. Firms will need to ensure they are audit-ready throughout the year.

Merchants should assess exposure, engage with providers, and begin implementation planning ahead of key deadlines. The FCA’s final guidance, issued in April 2025, outlines “reasonable procedures,” including fraud risk assessments, internal controls, staff training, and governance oversight. Why is it important?

This valuable information is essential when adjusting to market demands and consumer preferences. Before you even look at providers, take a moment to audit your current setup. Review the provider’s uptime record, understand their approach to incident response, and assess the quality of their customer support.

The key is to assess whether strong periods will generate enough cash to sustain the company through downturns. Flexible Cost Structure: Companies that can adjust costs in response to demand, such as by using temporary labor or scaling back overhead, are better positioned to maintain profitability during downturns.

This can impact the company’s stock price and ability to secure financing and increase external audit costs. Conduct regular risk assessments. Regularly assess the risk of material misstatement in financial reporting and adjust controls accordingly. Regular internal audits. Documentation and evidence.

Journal entries facilitate adjustments to the company's books to reflect transactions that have been recorded by the bank but not yet by the company, or vice versa. Clear and reconciled financial data enable management to assess the company's performance, manage cash flow effectively, and plan for the future.

It is crucial to conduct a thorough assessment of your financial position and ensure that you meet the minimum capital requirements. Risk management framework: Develop a robust risk management framework that identifies, assesses and mitigates key risks associated with your business operations.

Correct or adjust accounting records accordingly. Adjustment Recording : Adjustments in the accounting system are made to reconcile accounts, such as accounting for bank fees, interest earned, or rectifying errors. Audit Trails : Comprehensive audit trails to track changes and maintain a transparent reconciliation process.

Adjust Ledger Balances: Make necessary adjustments to the accounts receivable ledger to correct any errors or discrepancies. Document Reconciliation: Maintain detailed records of the reconciliation process, including any adjustments made and the reasons for those adjustments.

According to a new report by the National Audit Office (NAO), the number of telephone calls received by HM Revenue & Customs (HMRC) from customers was down from previous years. HMRC must allow more time for these services to bed in and understand the difference they make before adjusting staffing levels.”

The details contained in the FNOL for insurance claims assist the insurance provider in handling the claim, determining insurance coverage, assessing the extent of damage or loss, and settling the claim on the basis of the terms and conditions of the insurance policy. This accurate data is crucial for claims assessment and analytics.

Make Adjustments: Record missing transactions and correct errors for accurate balances. Document Process: Maintain detailed records of steps, findings, and adjustments. Proper documentation provides a clear audit trail and facilitates transparency and accountability.

Common in transportation and logistics, fuel surcharges adjust for fluctuations in fuel prices. Healthcare providers, for instance, may factor in compliance costs spent on cybersecurity measures, staff training, regular audits, and legal consultations to ensure adherence to health information privacy regulations. Fuel surcharge.

In a survey released earlier this year by the American Bankers Association (ABA), analysts found that banks are struggling with the regulations that impact their field — and are adjusting their risk management strategies accordingly. Sixty percent said that internal regulatory examinations include an assessment of risk management practices.

Decisions to extend trade credit are based on an assessment of a company’s financial stability, competitiveness, and desire and ability to pay to the seller’s terms. Critical Factors to Consider Be sure you are comparing companies with an analysis that is both current and audited.

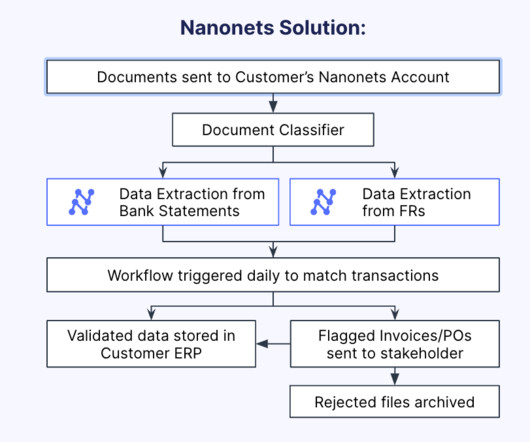

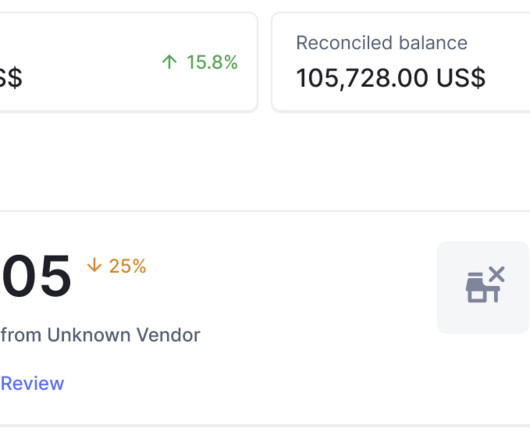

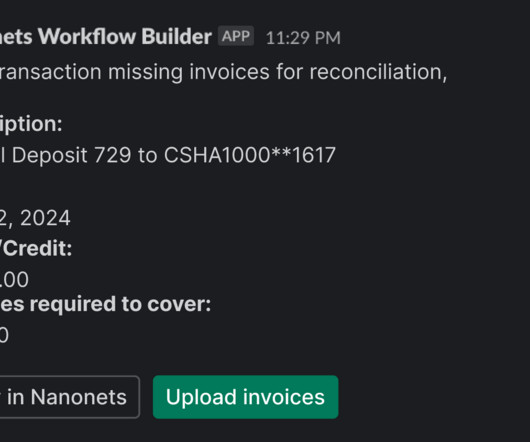

Bank statement processing is essential for accurate reconciliation , auditing, and financial reporting. Maintain an efficient audit trail for future retrieval. Adjustments Once the accounting team identifies and explains discrepancies, they make the necessary adjustments. 💡 Best practices: 1.

McKinsey’s research estimates that approximately 50% of work can be automated, leading to: Reduced errors Increased efficiency Enhanced compliance More time for accountants to focus on other high-level tasks Technology like FloQast can reduce the time to close by 30% , the reconciliation time by 38%, and the time for the audit to process by 23%.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content