This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Changes Access Controls "Limit viewing of audit trails" to those with a need. Testing Procedures Broad testing, looking at system settings, monitored files, etc. Minor adjustments to testing scope. audit log security principles are mostly unchanged. Testing procedures align with updated access language. No changes.

Key Proposals in the RBI’s Draft Guidelines Standardized Gold Valuation Lenders must use a transparent and uniform method for valuing pledged gold, with valuation done by certified personnel and subject to periodic audits. Purity checks must be documented and auditable.

Audit Bank Reconciliation Guide Both internal and external accounting audits are essential parts of financial management as well as organizational risk management. A bank reconciliation audit is one such process that helps in identifying financial gaps or discrepancies. Looking out for a Reconciliation Software?

If not, it may be time to rework your current accounting policies to implement audit trails. Despite what many business owners believe, audit trails aren’t reserved only for companies that receive an audit. Audit trails can prevent fraud, aid in disaster recovery, and ensure compliance with regulatory agencies.

Internal audits play a crucial role in assessing a company's internal controls, corporate governance, and accounting processes. These audits are essential for ensuring compliance with laws and regulations, as well as maintaining accurate and timely financial reporting and data collection.

Over the years, the auditing landscape has undergone remarkable transformations, and among the most significant advancements has been the advent of audit automation software solutions. Computer-Assisted Audit Tools and Techniques (CAATTs) have been available to auditors since the early 1990s. The situation has changed now.

Financial controls are the procedures, policies, and means by which an organization monitors and manages its revenues, costs, budgets, cash flow, and other financial aspects. It requires careful planning, regular monitoring, and ongoing adjustments. What are financial controls, and why are they important?

Here are some quick tips to keep you focused on your priorities: Review Risk Assessments and adjust internal controls as needed. Conducting internal monitoring and auditing. Maintain a strong Tone at the Top (“Culture of Compliance”). Set clear and realistic priorities. Exercise caution in dealings with third parties.

The requirement is to comply with safeguarding requirements audited annually, with the audit submitted to the FCA. The FCA estimated £150.8m (present value adjusted) benefits and £106.2m (present value adjusted) costs from the proposals, leading to a net PV-adjusted benefit of £44.6m

This collaboration helps avoid discrepancies and audit risks. Stay Informed on Regulatory Changes: Monitor global regulatory trends and mandates, such as real-time reporting requirements and clearance models, to proactively adjust processes and technology. In Summary.

Firms must prepare for these changes by improving their internal processes, conducting audits, and adapting to new compliance requirements to ensure seamless implementation of the FCA’s reforms. What’s next?

Outdated risk assessments, limited awareness of emerging risks, and failure to adjust processes during operational changes, like customer migrations, left gaps that allowed high-risk transactions to bypass scrutiny. Our expertise ensures that your business remains compliant, resilient, and well-positioned for growth.

Remember that internal controls are procedures and processes management emplace to ensure accounting integrity and financial transparency. In this case, the referee (actual control measures and checks) uses the playbook (company procedures built on accepted accounting principles) to manage the game (financial reporting).

Policy and Procedure Updates : We can assist in revising your policies and procedures to align with the updated expectations, including the addition of PF risk assessments and stronger sanctions monitoring protocols. Assess your compliance : Consider conducting a gap analysis to identify areas needing adjustment.

The researchers examined executive pay as a risk factor because auditing standards include executive compensation in their risk assessment and prior research. As a result, executives could use their higher-order ability to hide misstatements or to avoid current-period adjustments when the external auditor finds misstatements.”

Make Adjustments: Record missing transactions and correct errors for accurate balances. Document Process: Maintain detailed records of steps, findings, and adjustments. Proper documentation provides a clear audit trail and facilitates transparency and accountability.

The vendor reconciliation process is the systematic procedure of verifying and aligning the financial records of a company with those of its vendors. Compliance and Audit Readiness: Vendor reconciliation plays a crucial role in ensuring compliance with regulatory requirements and audit standards.

Employee Training on Chargeback Procedures Train employees involved in customer service and order fulfillment on chargeback procedures. Regular Security Audits and Vulnerability Assessments Conducting regular security audits and vulnerability assessments is essential to identify and address potential weaknesses in the system.

Applicable to large organisations, the offence imposes criminal liability if firms do not have adequate fraud prevention procedures in place, even if senior leadership is unaware of the misconduct. Next steps/action required: Commission a digital accessibility audit of all consumer-facing platforms and payment interfaces.

This can impact the company’s stock price and ability to secure financing and increase external audit costs. This includes identifying key controls, establishing clear lines of authority and responsibility, and ensuring that policies and procedures are well-documented and communicated. Regular internal audits.

BlackLine also provides configurable dashboards and reports that offer insights into reconciliation status, performance metrics, and audit trails. Audit Trails and Compliance : BlackLine maintains detailed audit trails of all reconciliation activities, providing a comprehensive audit trail for compliance purposes.

Compliance policies and procedures: Develop comprehensive compliance policies and procedures that address key regulatory requirements, such as anti-money laundering (AML) and Know Your Customer (KYC) obligations (see below). Staff training: Provide regular training to your staff on AML obligations, red flags, and reporting procedures.

And, although smaller public companies may not always be mandated to conduct an integrated audit, they are still required to present their auditors with a framework of their controls. Companies must be prepared for an integrated audit as they grow and expand. Manual adjustments lead to higher error rates and version control issues.

You’ll have to find the reason and a proper expense category and adjust the balances properly. Check ending balance - Your general ledger balance ending balance should match your bank statement balance after all your adjustments. Check the entries that don’t match - Multiple entries will not match.

With more than 150,000 leasing contracts under management, AMAG Leasing AG has been able to automate large parts of the decision-making procedure involved in striking new leases so that the company will be able to handle 50 percent more applications with the same workforce, thanks to the power of FICO® Decision Modeler.

If the ending balances don't match, accountants investigate the cause of the discrepancies and make adjusting entries required to resolve differences resulting from errors or missing transactions. Once accounting reconciliation is complete, adjustments to the GL account balance may be made through an adjusting journal entry.

Businesses are encouraged to familiarize themselves with the procedural steps of cash reconciliation, adopt best practices to enhance accuracy, and consider the benefits of automating the process to mitigate risks associated with manual reconciliation. Recording the starting cash amount in the drawer, itemized by bill and coin types.

Are you focusing on workflows that allow for standardized steps and procedures to be followed? Monitoring and Optimization : Once implemented, continually monitoring and adjusting is crucial. Once everything is in place, review your workflows regularly and make adjustments to keep your team on the right track.

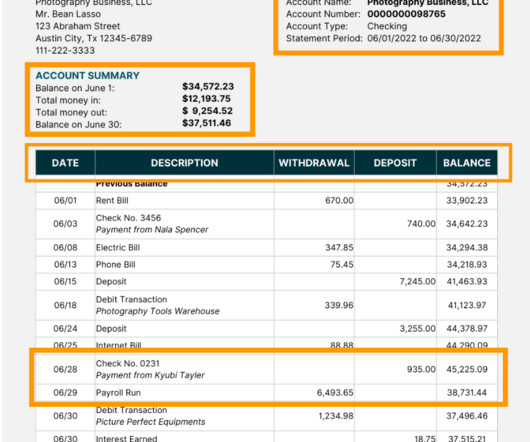

Bank statement processing is essential for accurate reconciliation , auditing, and financial reporting. Maintain an efficient audit trail for future retrieval. Adjustments Once the accounting team identifies and explains discrepancies, they make the necessary adjustments. 💡 Best practices: 1.

This policy outlines acceptable expenses, the procedures for submitting expenses for reimbursement, and the roles and responsibilities of staff and management in the expense reporting process. Enforcing explicit procedures for approval and reimbursement creates a standard for audits. What is an expense policy?

In a survey released earlier this year by the American Bankers Association (ABA), analysts found that banks are struggling with the regulations that impact their field — and are adjusting their risk management strategies accordingly. Sixty percent said that internal regulatory examinations include an assessment of risk management practices.

Automated Accounts Reconciliation software like Nanonets can cohesively consolidate all data sources on one platform, automate the matching logic across external data sources and general ledgers, effectively provide an audit trail, and keep the process transparent for the accounting team personnel involved.

This could involve making adjustments to the general ledger, correcting errors, or seeking clarification from external parties. Make the necessary adjustments and ensure that all transactions are accurately recorded in the appropriate accounts. Once the cause of the discrepancy is identified, take the necessary steps to resolve it.

This process includes verifying transactions against payroll registers and tax reports, ensuring that tax withholdings match figures reported to tax authorities, accounting for accruals and adjustments related to payroll expenses, and verifying the accurate calculation and recording of employee benefits and deductions.

Scalability: Outsourcing allows for scalability, enabling you to adjust the level of reconciliation services based on your business needs and fluctuations in transaction volumes. Quality Control: Businesses may struggle to ensure that external providers adhere to established standards and procedures.

This can be done through detailed audits, process mapping, and feedback from procurement staff and stakeholders. Ensure the pace of execution is manageable and allows for adjustments based on feedback and results. Implement tools that provide real-time market insights and automate price adjustments.

The external transactions go through the routine account reconciliation procedure, where the general ledger is matched with documents like bank statements. Its primary aim is to accurately account for all transactions and adjust accounts according to intercompany accounting rules. However, it is prone to errors due to its complexity.

It's a process that ensures every payment, adjustment, or write-off tied to an invoice is accounted for and settled. This might sound straightforward, but consider situations where there are adjustments such as discounts, returns, or errors. The invoice settlement process is a multi-step procedure.

Access to the Financial Ombudsman Service (FOS) BNPL customers can now escalate complaints to FOS, increasing the importance of auditable redress processes and timely resolution. Complaint handling will need to be FOS-ready This includes robust audit trails, clear redress pathways, MI reporting on themes, and training on FOS processes.

Automates stock audits, forecasts low-stock items, and deducts sold items from inventory. It should help your business save time by automating stock audits, forecasting products running low in your inventory, and deducting sold items from your inventory. The POS system should track stock levels across multiple locations in real time.

In addition to accelerating the reconciliation process, reconciliation software also enables an audit trail, significantly improving transparency and accountability. Once approved, the reconciled data is securely stored in a centralized database, ensuring an auditable trail.

In addition to aiding in financial transactions, invoices are an integral part of accounting internal controls and audits. Invoices play a crucial role in maintaining accurate accounting records, internal controls, and facilitating audits.

This includes encryption and tokenization of payment data, secure storage practices, and regular security audits. They should include detailed explanations of billing cycles, payment amounts, renewal policies, and cancellation procedures. Regularly reviewing and optimizing pricing models keeps the offerings competitive and appealing.

Updating and Evolving Policies: Bi-annual reviews to adjust limits and categories as per market rates and company growth. The management team, acknowledging the practical challenge, decides to adjust the policy. Record-Keeping : Finance stores the expense reports and receipts for auditing purposes.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content