This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The immediate safeguarding of funds could strain liquidity for smaller firms, requiring adjustments to workflows and potentially increasing reliance on credit facilities. Voices from the industry "The more voices that are heardsupporting the proposals or notthe more the FCA will likely take that feedback on board.

Keeping pace with agentic demands Financial infrastructure built for the self-hosted era cannot meet the demands of autonomous agents. The real edge lies in platforms with real-time, no-code configurability, dynamic rule engines that adjust instantly, and composable services that support emerging agentic use cases.

Additionally, an influx of CBDC usage across the globe could encourage central banks to adjust their foreign exchange reserves to include more CBDCs, influencing global capital flows and the traditional dynamics of reserve currency utilisation. Flexibility is also crucial when it comes to custody.

As new threats emerge, the shared knowledge pool helps all participants quickly adjust their models and their fraud prevention tools. This initiative builds on Swifts existing Payment Controls Service (PCS), and follows a successful pilot with financial institutions across Europe, North America, Asia and the Middle East.

Just by embedding analytics, application owners can charge 24% more for their product. How much value could you add? This framework explains how application enhancements can extend your product offerings. Brought to you by Logi Analytics.

The concern is regarding the period of adjustment and whether this leaves firms exposed to operational and compliance risks, particularly in the absence of established precedents. The impact of the UK Digital Assets Bill on PSPs, highlighting legal uncertainties, operational challenges, and strategic opportunities. Why is it important?

The Asian payments market is growing at an extremely fast rate due to a variety of factors, including an increase in smartphone penetration, rising financial inclusion, and the booming demand for digital services. Its latest milestone has included the launch of new local payment options across the region.

Consumers are shopping smarter, demanding convenience, security, and speed like never before. Consumers are embracing the convenience of online shopping, and businesses are rapidly expanding their digital presence to meet this demand. Global online sales are expected to hit $8.3 trillion, growing by more than 55% since 2021.

Furthermore, they adapt to business changes over time, whether its incorporating new data sources, adjusting to process updates, or adapting to changing regulatory requirements. Enhanced compliance : AI agents can be directed to scrape regulations to automatically detect changes and adjust accordingly.

Conversely, slowdowns in GDP can signal tighter consumer spending, lower business investment, and reduced demand for financial services. Business payment activity expanded, with 43% of firms increasing investment in digital payment tools—responding to stronger demand and economic stability. In 2020, U.S.

Consumers are demanding more. As these platforms integrate financial services, travel, retail, and daily lifestyle offerings into a single scalable ecosystem, automation becomes critical to delivering the frictionless, personalised experiences that users now demand.

They’ve validated demand, fine-tuned their offering, and now it’s time to take the next step: accepting payments and scaling the business. Of course, figuring out when and how to adjust 3DS flow adds another layer of complexity, with more logic, coding, and integration to manage. Here’s how those jobs break down: 1. Workflow Mapping.

Integration is far more extensive than simple order transmission—it creates one system whereby inventory levels, customer information, pricing, and financial information are continuously current on both systems. The best integrations manage bidirectional data flow, which means data flows effortlessly in both directions.

High-end merchants are in the perfect position to respond to this demand. These high-value customers demand more than just a premium product, they expect an exceptional experience, from sustainability and quality to seamless and secure payments.

This rising demand for LAMF reflects a valuable opportunity for lenders, driven by a streamlined and rapid application process that attracts a growing borrower base. That said, LAMF is a comprehensive financial solution that elegantly balances the demand for short-term liquidity with the goal of long-term investment growth.

No longer satisfied with being simply digital and inspired by interactions with Chat GPT, customers began demanding something deeper— experiences that understand them. For example, some banks use AI to automatically notify customers of unusual spending, predict upcoming bills or suggest budget adjustments—all tailored to the individual.

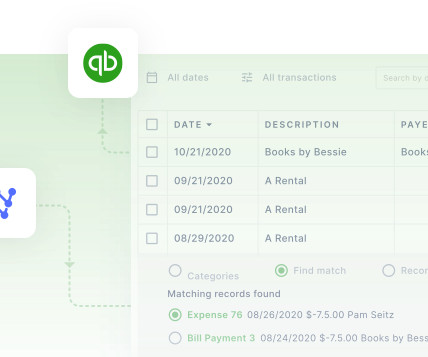

This transparency helps you make informed decisions about accepting or adjusting its recommendations. While Intuit Assist streamlines many financial workflows, complex enterprise requirements often demand additional capabilities. Businesses using QuickBooks ' AI-powered features get paid five days faster.

Luckily, enterprise merchant services step in to meet that demand. This valuable information is essential when adjusting to market demands and consumer preferences. As your transaction volume increases and your systems expand, so does the need for infrastructure that can handle the pressure without slowing you down.

Others rely on algorithms and supply adjustments, hoping that code and incentives alone can keep the price stable. They rely on mechanisms that increase or reduce supply based on market demand. Circle’s IPO earlier last month turned more than a few heads on Wall Street. So, What Is a Stablecoin? A stablecoin is a type of digital token.

Tony: And whats driving that changecost, compliance, or customer demand? If the rules of the game are going to changeand they likely willthen the question becomes: do you have the capabilities and flexibility to adjust? Thats not just a tech upgradeits an operating model shift. Regulators are definitely upping the ante. Thats unusual.

This data can identify customer preferences, allowing merchants to adjust their payment offerings accordingly. These payment insights can also help adjust strategies to prevent cash crunches. This enables more accurate budgeting and financial planning. Analytics can reveal feedback on transaction speed, security, and ease of use.

Addressing these vulnerabilities demands collaboration across financial institutions, digital platforms, and regulators. Unveiling digital fraud: Insights into scam trends and prevention in the UK payment sector January 3 2025 by Payments Intelligence LinkedIn Email X WhatsApp What is this article about? Why is it important?

A monthly vendor payment can afford to wait for batch processing if it saves costs, while a real estate closing demands immediate settlement. Tackling the True Challenge: Operational Readiness Real-time payments demand comprehensive operational transformation. Real-time fraud detection is also particularly complex.

UK payments firms are grappling with a critical question: What level of risk is acceptable in a market that demands both innovation and resilience? Key areas for regulatory adjustment Enhancing market competitiveness and innovation A well-regulated payments landscape supporting innovation is important for the UKs economic growth.

By monitoring market volatility, client flow, and inventory risks, they can autonomously adjust bid-ask spreads and quote levels. Advances in reinforcement learning and large language models (LLMs) have enabled agents to make decisions, learn from outcomes, and operate independently in complex domains. What is Agentic AI?

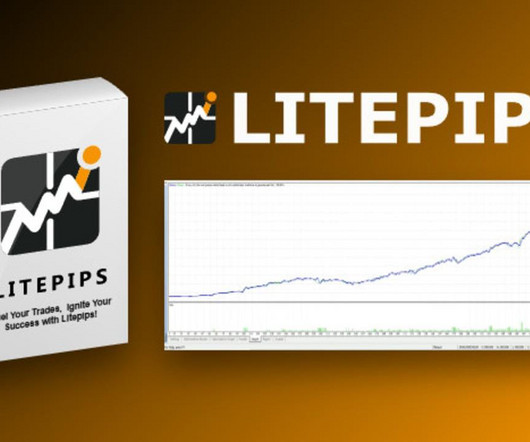

Unlike traditional trading bots that operate on pre-set conditions, Litepips dynamically adjusts to changing market structures, leveraging historical price action and pattern recognition to enhance decision-making. The demand for adaptive bots like Litepips continues to shape forex and gold markets.

For payments firms, integrating tailored insurance at checkout or as part of transaction flows presents a new value proposition and customer engagement lever, but also demands new risk management capabilities. Insurers now assess policyholders’ financial behaviouralongside payment patternsto adjust coverage dynamically.

Users can manage direct debits through banking apps, pausing, cancelling, or adjusting payments without calling the provider. Security, Visibility, and Peace of Mind Photo by Pixabay on Pexels.com To pay bills online with confidence, users demand strong security and total visibility. Usage-based billing is also common.

However, the rise of e-commerce and AI-driven analytics has reshaped the demand for tier three data. Unlike traditional receipt scanning apps or rewards programs, Smart Receipts dynamically adjusts offers after the transaction to suggest relevant products, cross-sell complementary items, and drive repeat purchases.

They collect data, monitor outcomes, and adjust operations in collaboration with the regulator. Startups can adjust based on genuine customer feedback and regulatory scrutiny. They are one of the most important tools regulators have introduced to support responsible financial innovation. What is a Regulatory Sandbox?

But this isn’t just about GPUs or cooling systems—it’s about how you build AI that earns trust, scales cost-effectively, and adapts to regulatory demands. Imagine a suite of AdviceRobo agents: One analyzing psychometric data, Another adjusting for behavioral shifts, A third scanning macroeconomic risks.

This is legal in all states but still demands clarity. Adjust your listed pricing to reflect built-in card processing costs. The surcharge is a percentage ( up to 4% ) of the transaction total. It’s applied only to credit card transactions, not debit or prepaid cards. Surcharges are legal in most—but not all—states.

Stablecoins have experienced substantial growth across the globe over the past year, reaching an adjusted transaction volume of $6 trillion, a 63% year-over-year increase. • The ability to scale with demand and transaction value. • A framework that meets current and evolving regulations.

Long Overdue for Innovation: Costs of Outdated Loan Servicing Featured image by abidakhatoon938 on Freepik Traditional loan servicing systems, often siloed and built on manual processes, were not designed to meet the demands of today’s modern banking.

In the 12 months to May 2025, adjusted on-chain stablecoin transaction volume reached $20.2 Earlier attempts—such as BGBP and GBPT—failed due to regulatory uncertainty, limited integration, and low market demand. They could enhance demand for sterling-denominated sovereign debt. The rest of the world is not waiting.

Strategic Business Benefits Competitive Market Positioning: Integrated E-commerce businesses are more attuned to market opportunities and customers’ demands. Universal platform connectors have emerged as the solution, enabling integration between NetSuite and any e-commerce platform. These operational inefficiencies compound over time.

Adjusting business operations to match the season can also prevent cash flow challenges. Optimize inventory: Since excess inventory can tie up cash that can otherwise be used for other high-priority expenditures, optimizing inventory by understanding customer demands will be helpful. Offer payment discounts for early payments.

For example, subscription-based billing, large invoice volumes, or international clients will demand more from your NetSuite payment gateway. Closely monitor payment activity during the initial weeks and adjust workflows or settings as needed. That’s where third-party NetSuite payment gateways come in.

As global demand for gift cards surges, Runa , the leading global infrastructure powering modern payouts, today unveiled Runa Shop, a white-label commerce solution that makes launching gift card marketplaces fast and simple. And we take on the expensive program risks like compliance, liability, and payment processing so they don’t have to.”

Were already seeing major crypto firms like Coinbase adjusting their operations to meet MiCAs requirements, while others are reassessing their market strategies some even shifting focus to countries with more relaxed crypto regulations. What makes the EU AI Act stand out is its risk-based approach.

led global trade disruption is turbulent in the near-term but represents a long-term tailwind for cross-border payments specialist Payoneer Global as companies adjust and find new trading partners, the company’s chief executive contended in an interview this month. Cheng Xin via Getty Images U.S.-led The bulk of the U.S.

Designed for traders who demand both speed and accuracy, Avexbot processes high-quality tick data, analyzes daily candlestick trends, and adjusts its execution strategy in real time, bridging the gap between algorithmic efficiency and strategic insight. This system isnt about chasing every price move, its about strategic positioning.

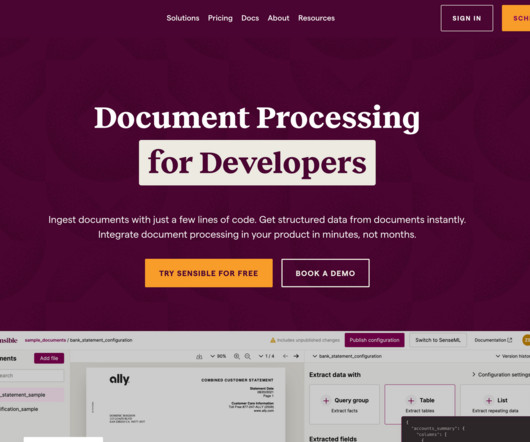

While Sensible offers robust document processing capabilities, it’s not always the best fit for every business. Here’s what you might want to consider before committing: Pricing challenges: Sensible’s pricing structure can feel steep, especially for businesses with irregular or low-volume document processing needs.

Adjusting payment terms, diversifying supply chains, and closely managing working capital are critical to maintaining financial stability in the face of international sales and tariff disruptions1. In May 2025, CreditSafe surveyed over 200 U.S. finance, procurement, and supply chain professionals to assess the impact of new U.S.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content